If you have any questions about the software, please feel free to email us at info@aiaccount.com for inquiries.

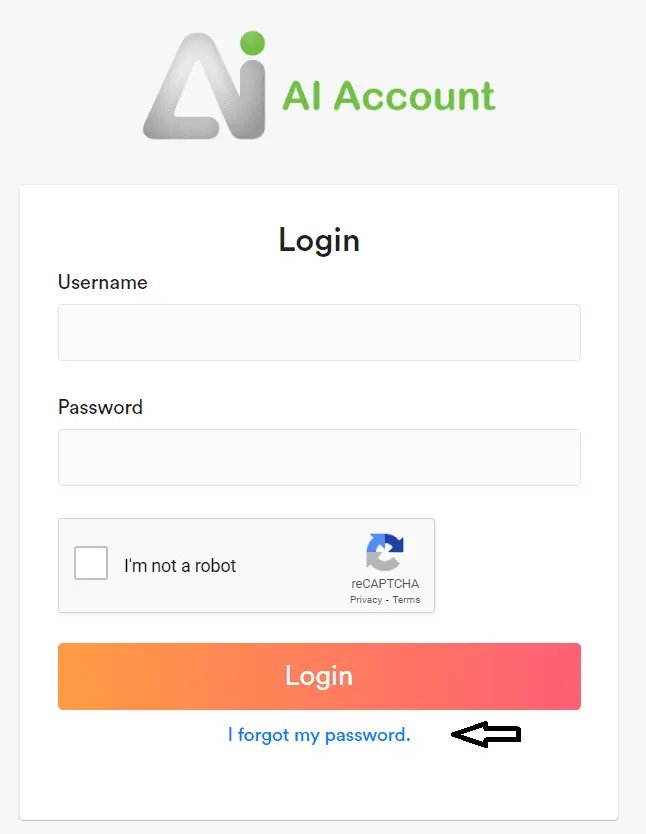

First Time Login

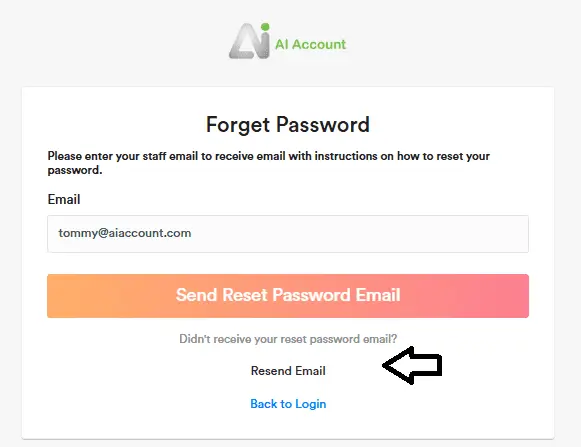

You can check your spam mail folder, as the reset password email and 2FA email may have been directed there.

For first-time users, please visit https://app.ai-account.com/ and follow the steps outlined below:

Click on “I forgot my password.”

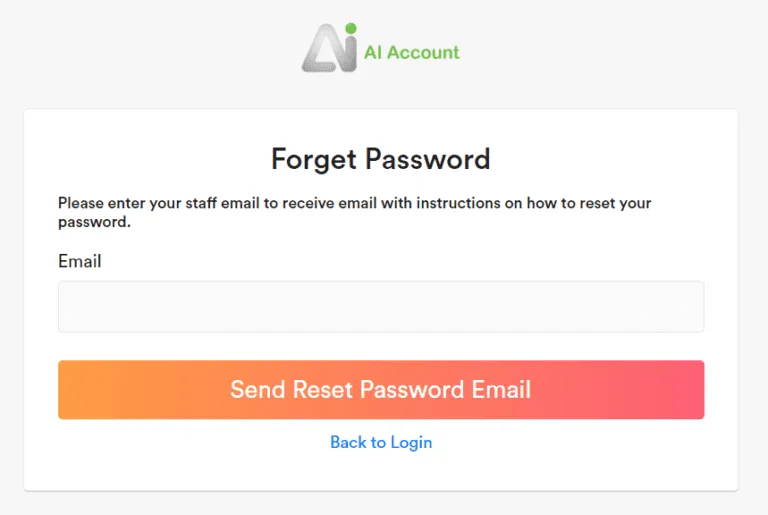

Enter your email address and click “Send Reset Password Email”. You will receive an email from our system, allowing you to set a new password and log in to your account.

Click Resend Email to send the reset password email again if you didn’t receive it the first time.

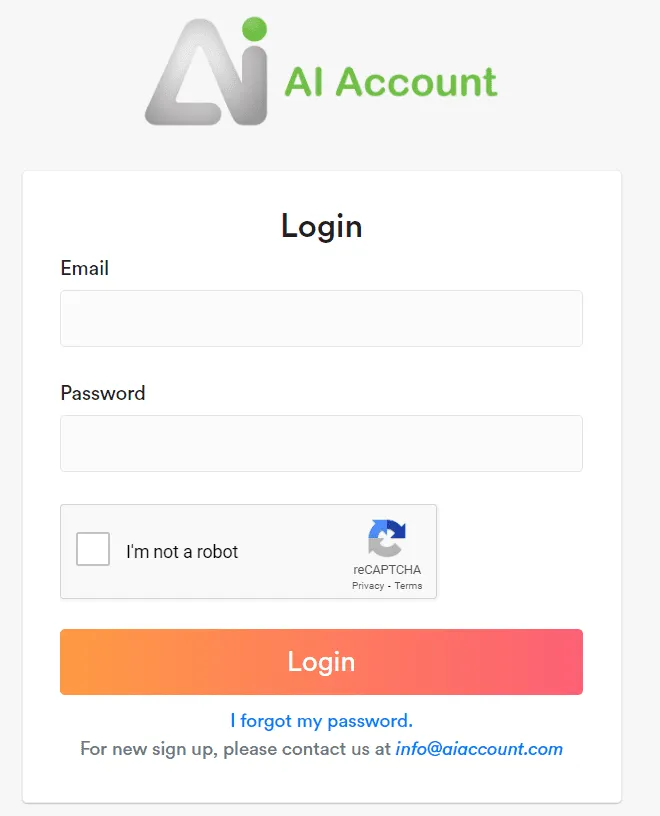

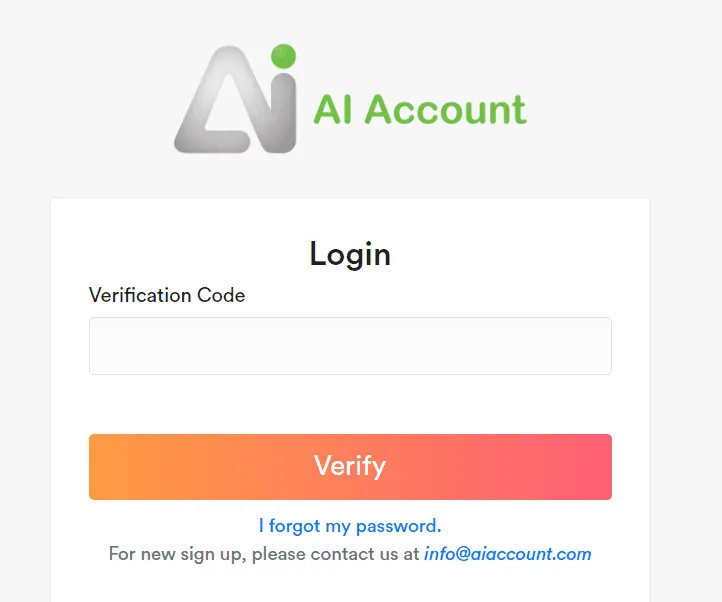

Enter your email and password to log in to your account.

Thereafter, enter the verification code sent to your email and click ‘Verify’.

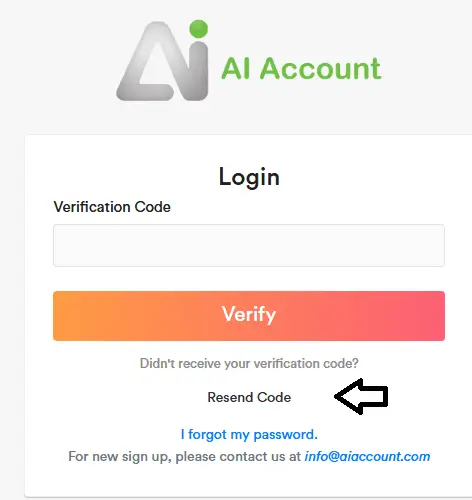

Click Resend Code to send the Verification Code again if you didn’t receive it the first time.

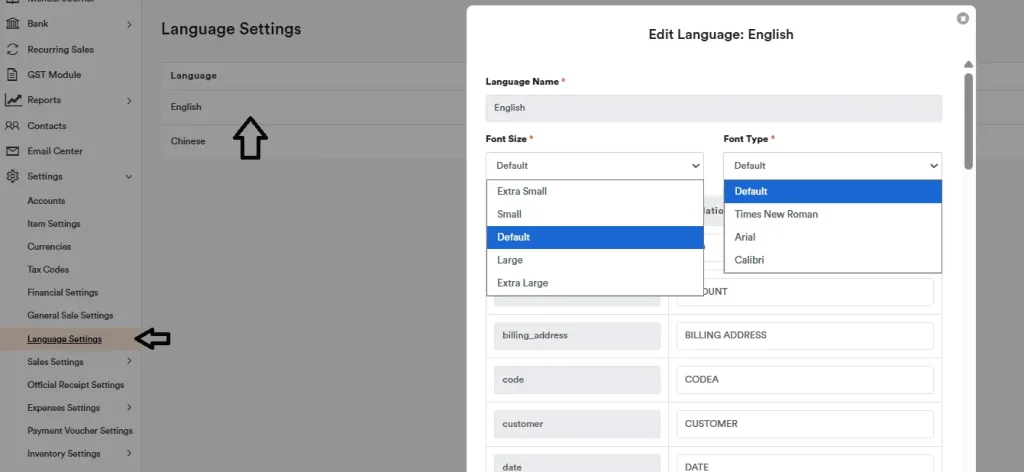

Customise Plan

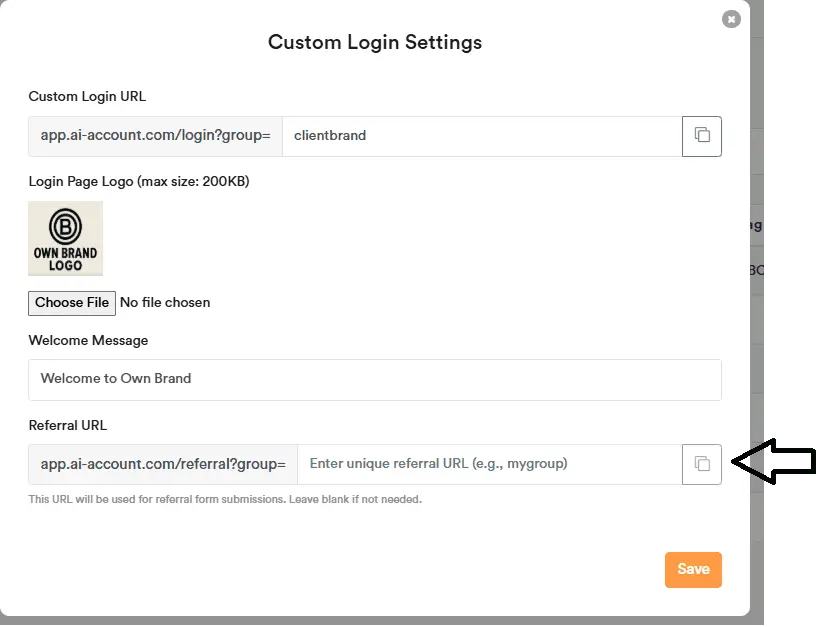

Customise Plan (Create Your Own Login Page)

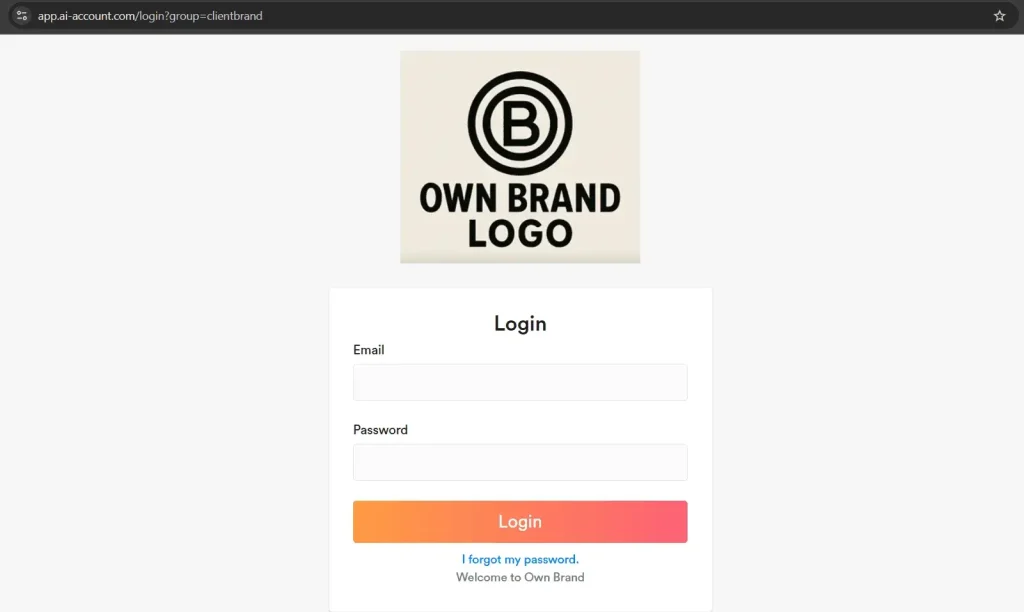

You can create a personalised login page with your own logo, allowing your customers to log in to AI Account and see your company branding. This lets you white-label the accounting software, making it easier to resell to your customers.

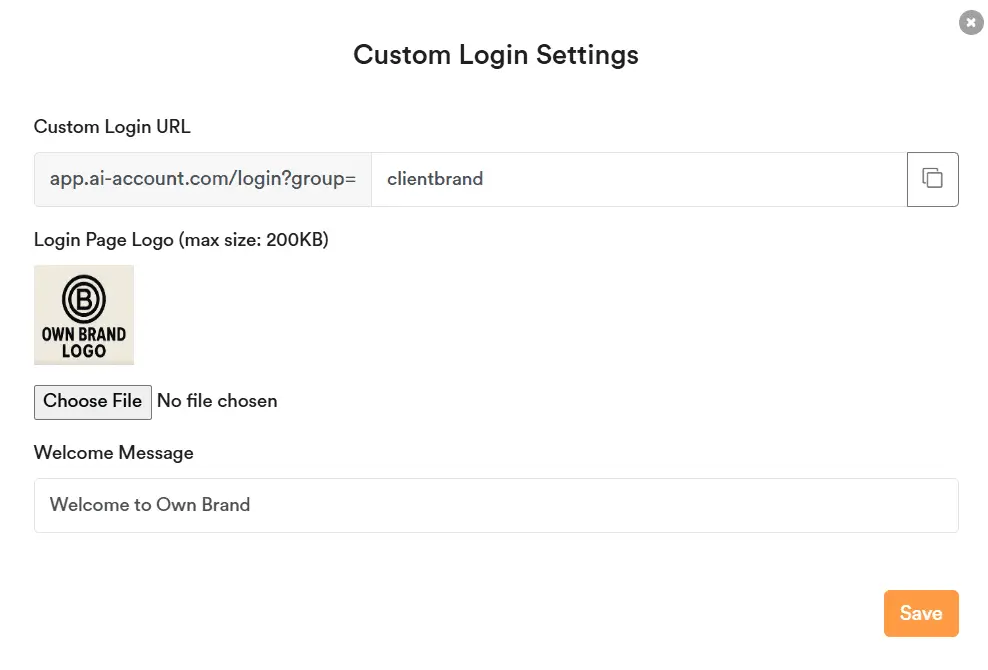

To set it up, click on Custom Login.

Next, fill in your desired URL name, upload your branding logo, and enter a welcome message for your customers. Click Save. Then, click the copy icon beside the URL to copy and share it with your customers.

Your customers can then use the custom URL to log in and see your branding on the login page, as shown below.

Customise Plan (Create Your Referral URL)

In Custom Login Settings, you’ll find the Referral URL. Enter your own preferred URL, save it, and share it with your friends. When a referral is successful, we’ll process your referral fee.

Your friend can submit their interest and we’ll then contact them to set up a free trial or a package that suits their needs.

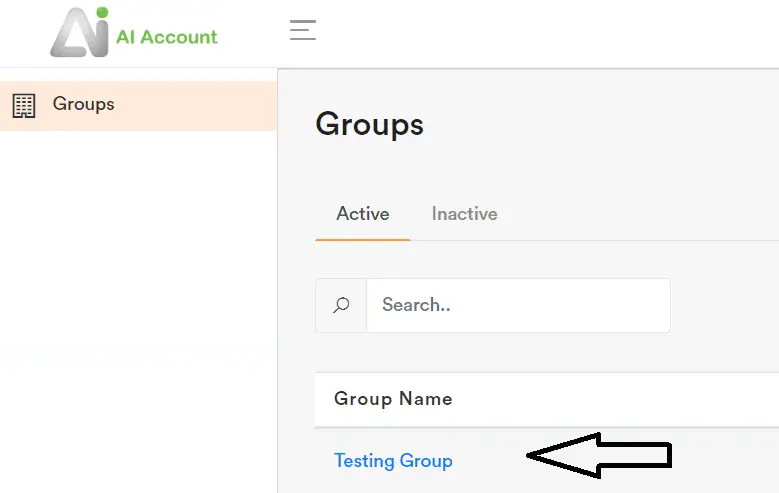

Customise Plan (Group Access with Unlimited Company Support)

When clients sign up for the Customised Plan, you will receive Group Access with support for an unlimited number of companies.

A group will be created under your brand.

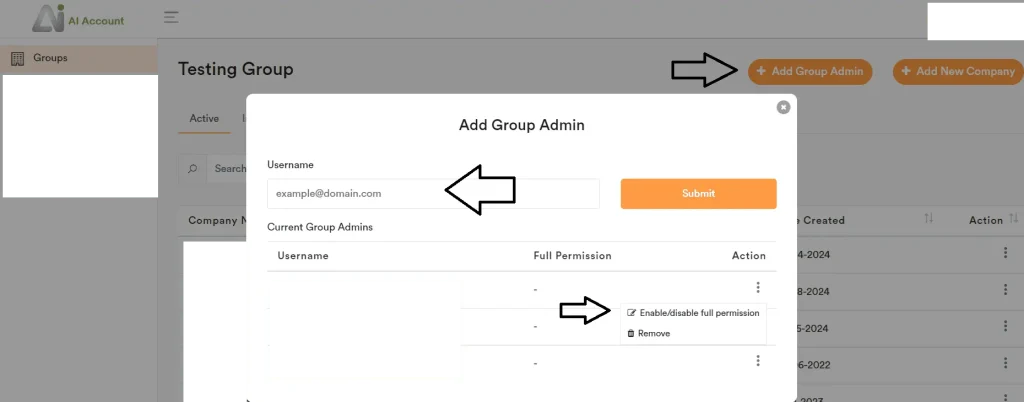

You can assign Group Admins (input the email at the Username box and click ‘Submit’) and grant them ‘full permission’ as needed. Group Admins with full permission can add or remove other Group Admins within the group.

Group Admins also have the ability to add new company within the group.

Customise Plan (How to Create a New Company)

After clicking into your group, click “Add New Company” to create a new company account.

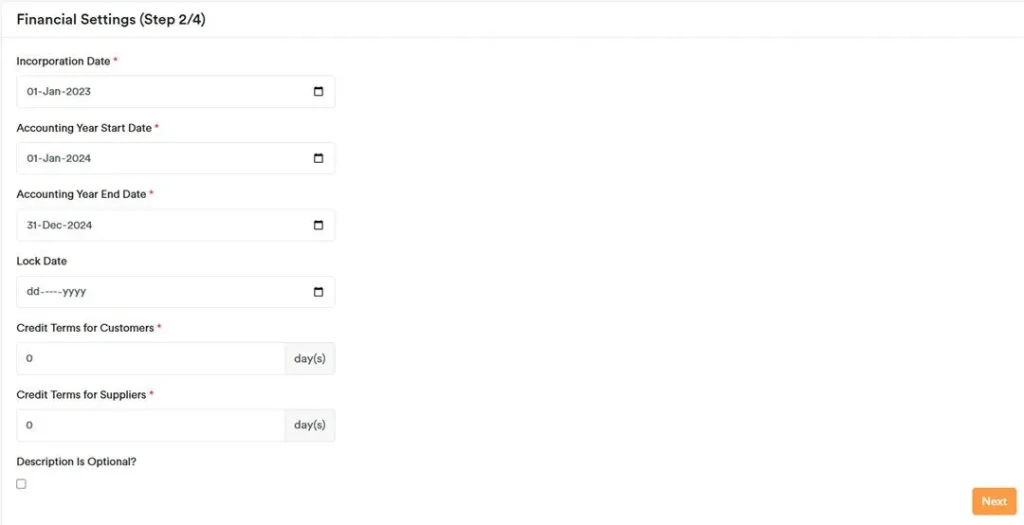

Fill in the required fields (at minimum, the company name and country), then click Next.

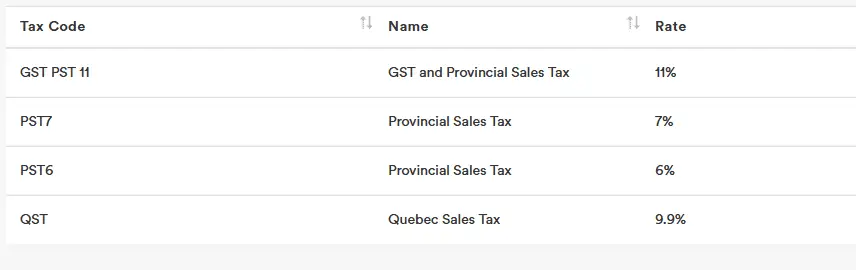

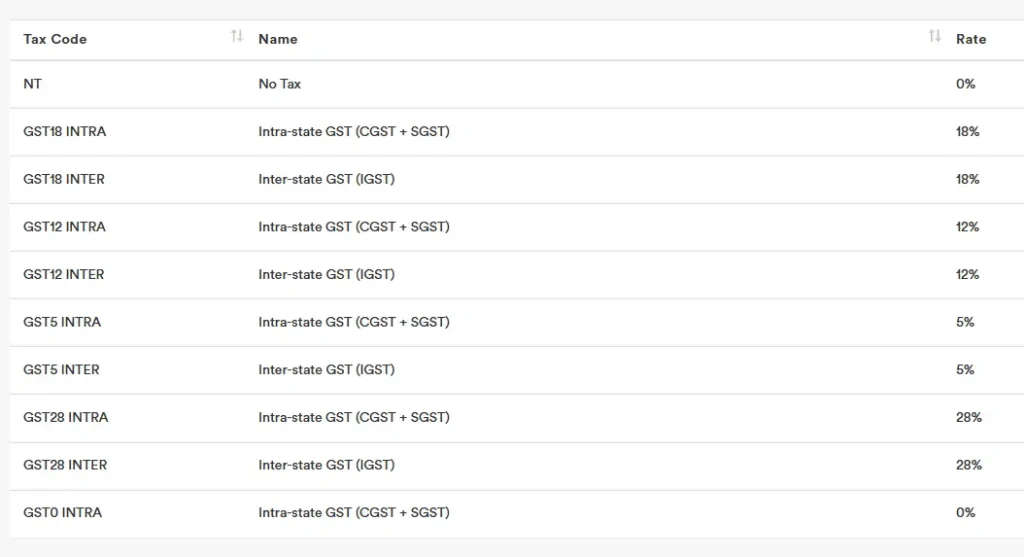

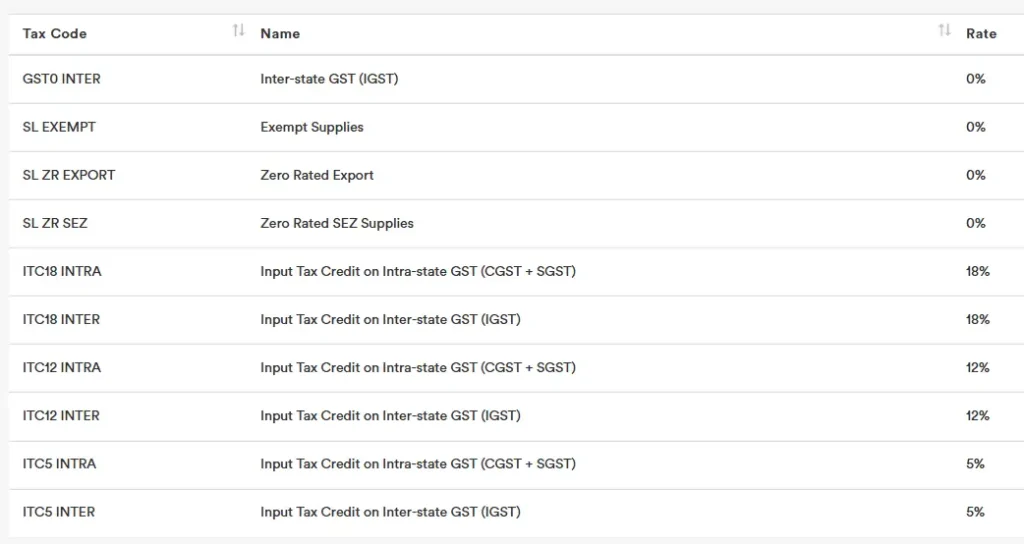

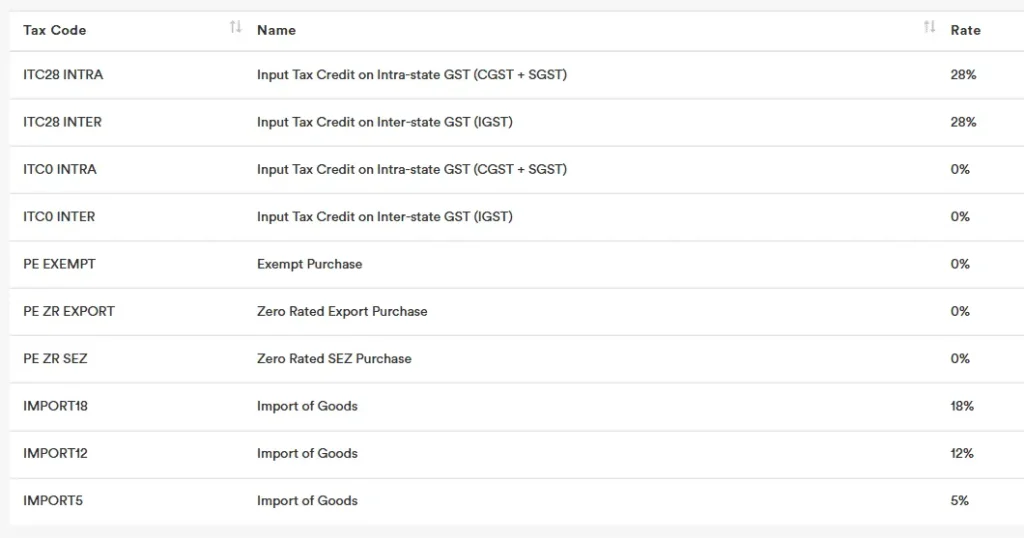

Note: The default tax codes for the selected country will be automatically set based on your country selection.

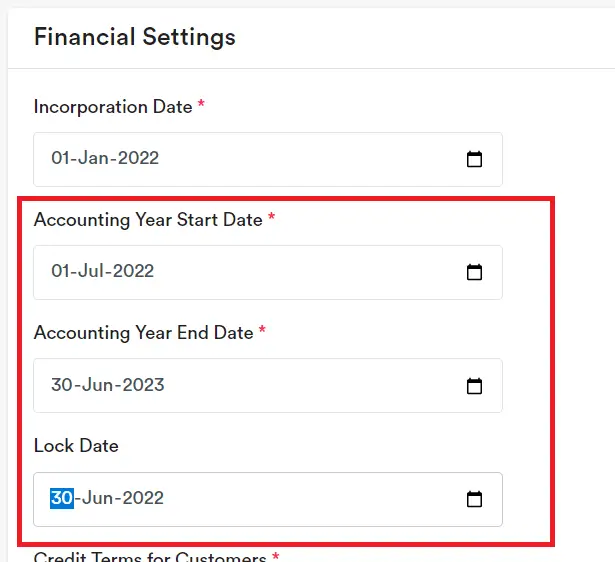

Enter the Incorporation Date (entries before this date are not allowed), Accounting Year Start Date, and Accounting Year End Date, then click Next.

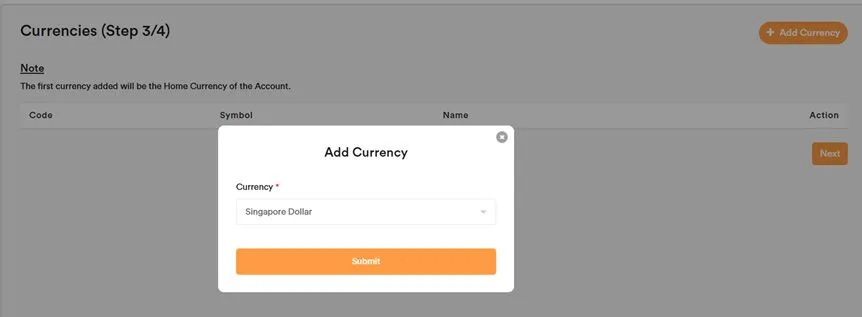

Click Add Currency to set the company’s Home Currency (also known as the functional currency).

Select the currency and click Submit, then click Next.

Note: The home currency cannot be changed after setup. If the company wants to change its home currency, a new company must be created.

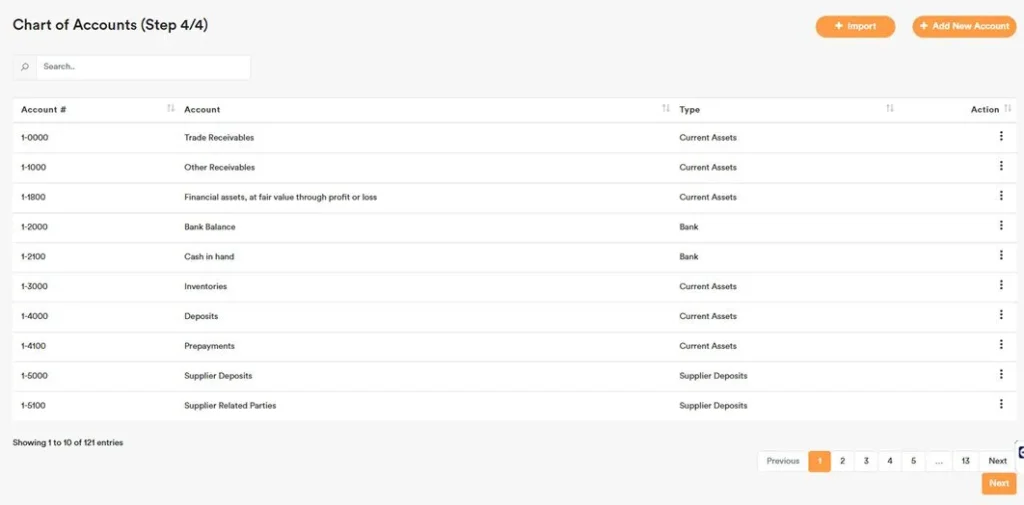

The Default Chart of Accounts will be automatically created. If no customisation is needed, simply click Next.

To add your staff or client as a user for the newly created company, go to the “Add New Users” section and follow the steps there if needed.

For Group Admins with full access, you can add or edit tags for each company. This feature allows you to group clients (e.g., those under the same group) by assigning specific tags. You can also use tags to differentiate between companies with the same name, such as tagging one as “HQ” and the other as “Branch”.

Customise Plan (Get your Certificate)

After logging in, open your Group and click the ‘Export Certificate’ button at the top right to download your Certified Partner certificate.

Supported Countries

AI Account currently supports the following countries. We’ve customised the chart of accounts and local tax codes for each:

- Australia

- Bermuda

- British Virgin Islands

- Brunei Darussalam

- Cambodia

- Canada

- Cayman Islands

- China

- Hong Kong

- India

- Indonesia

- Lao PDR

- Malaysia

- Maldives

- Myanmar

- New Zealand

- Pakistan

- Philippines

- Singapore

- Taiwan

- Thailand

- United Arab Emirates

- United Kingdom

- United States

- Vietnam

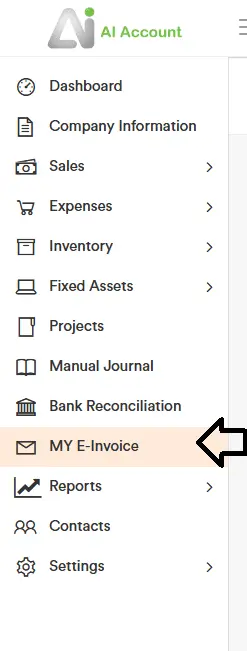

E-Invoicing Support

We currently support e-invoicing in:

- Malaysia

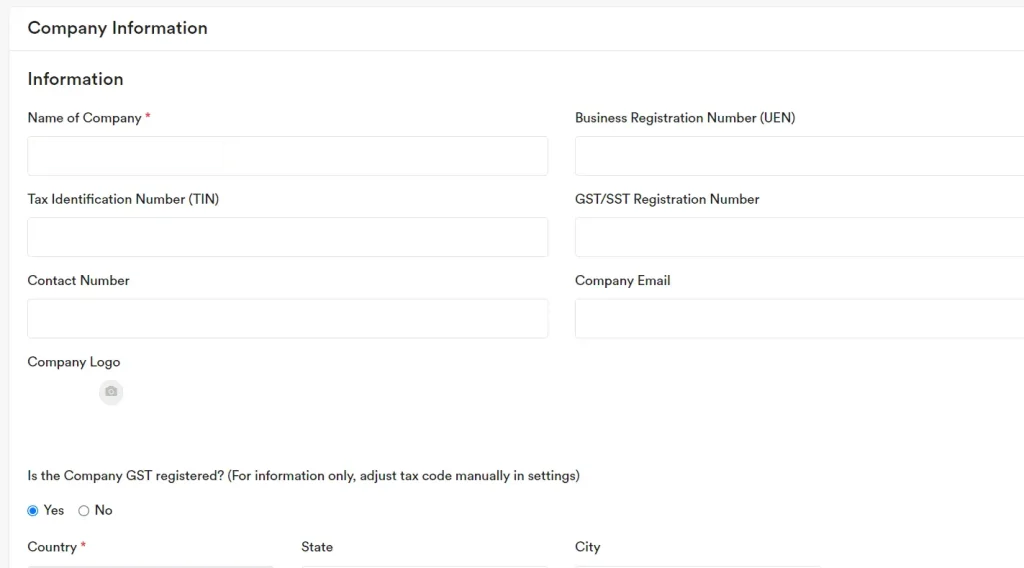

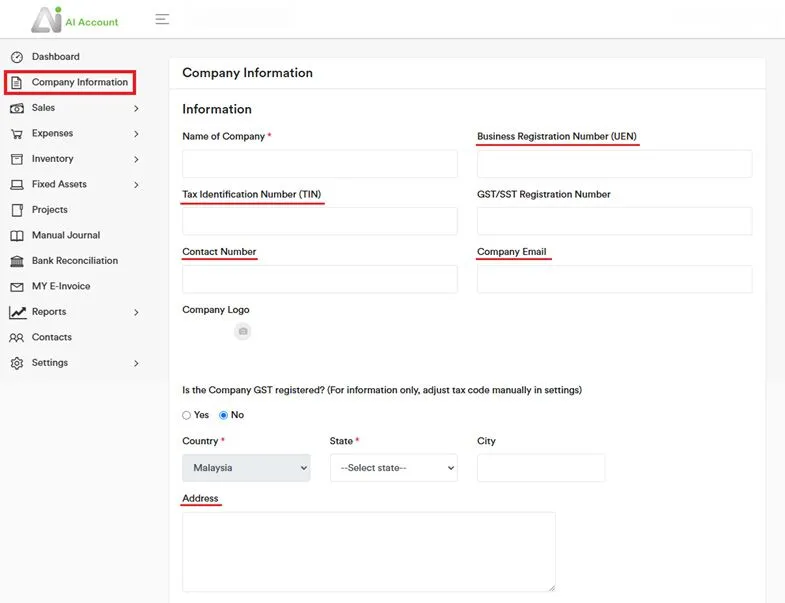

Company Information

Complete the relevant fields that apply to your company.

Security & Data Protection

AI Account is Singapore-headquartered (AI Account Pte. Ltd.), and our handling of personal data follows the Singapore Personal Data Protection Act (PDPA). Our Data Protection Policy explains what we collect, how we use and disclose data, the legal bases for doing so, and covers retention, access/correction rights, overseas transfers with PDPA-comparable protection, and governance under Singapore law.

ISO 27001-certified information security

AI Account’s Information Security Management System (ISMS) is certified to ISO/IEC 27001:2022 — a globally recognised standard for managing information security risks through formal governance, controls, and continual improvement.

The certification scope covers the governance, design, development, operation, maintenance, and support of the AI Account cloud-based accounting platform (including applications, data, and supporting services).

It also includes the supporting cloud infrastructure and managed services hosted across multiple environments.

This certification is issued following an independent assessment and is maintained through ongoing surveillance audits during the certificate period.

Layered security controls and resilience

We apply layered protection across:

- People: access restricted to authorised staff operating under clear security rules and procedures

- Providers: reputable cloud/hosting infrastructure with strong safeguards

- Technology: encryption and strong access controls to protect data

We also maintain daily backups of production data to support business continuity and recovery. While no method of transmission or storage is 100% secure, we continuously review and enhance our measures.

Secure connections and external safety checks

Connections to our app are protected using modern TLS. An independent SSL Labs test of app.ai-account.com shows an A rating with TLS 1.3 support (assessed 19 Aug 2025), indicating a strong HTTPS configuration.

You can also verify our domain’s current safety status anytime via Google Safe Browsing’s Site Status checker (results are dynamic and reflect the status at the time you view them).

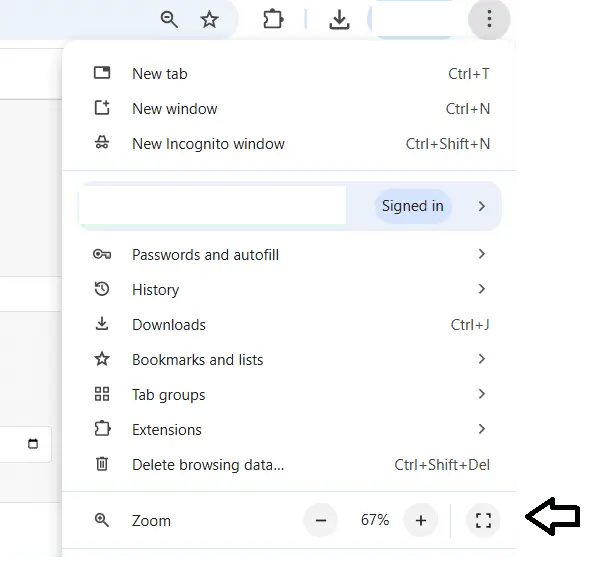

Systems Requirements

Recommended Browser

Latest Google Chrome

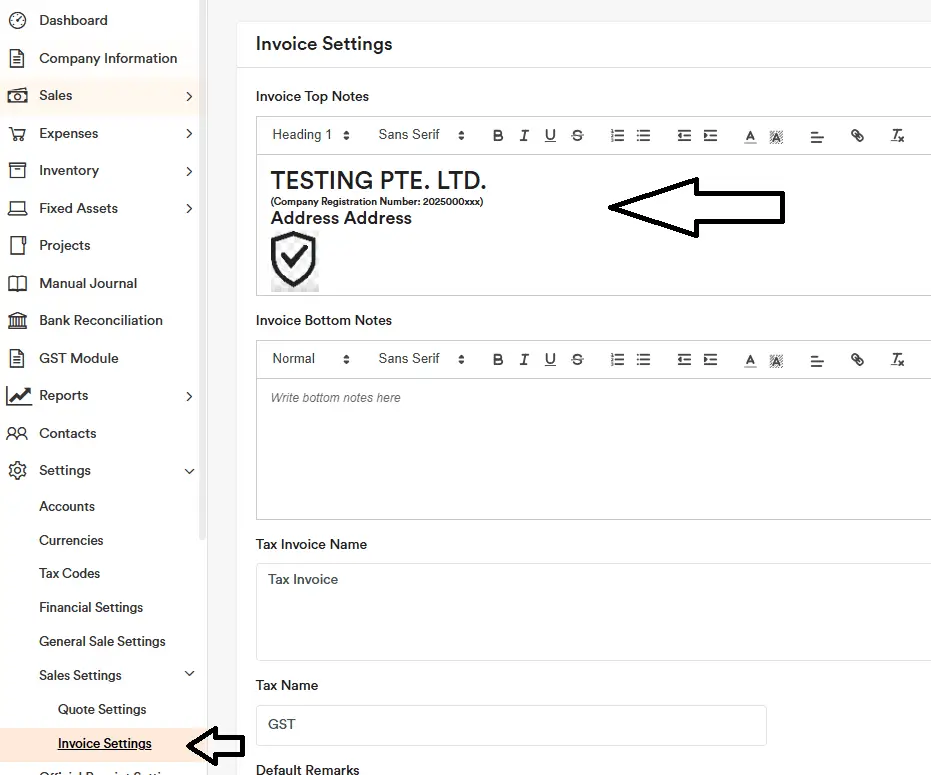

For the best viewing experience, set your zoom level to 67%. This zoom level makes it easier to adjust items such as the top notes and bottom notes, and it more accurately reflects the actual report.

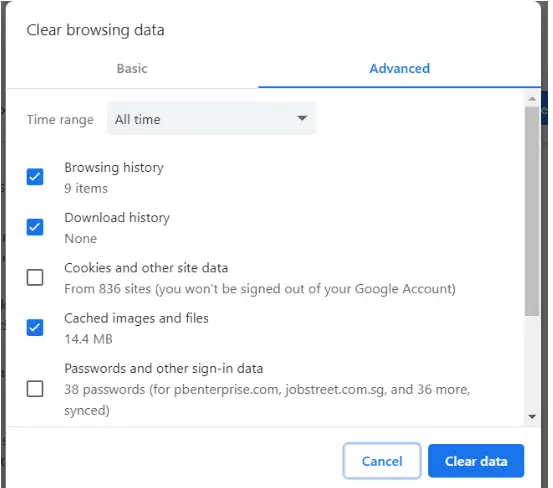

Clear Cache

Sometimes, you need to clear the browser cache to receive the latest software updates. Press Ctrl + Alt + Delete, and select the following items to clear:

Remember to choose the time range ‘All time’.

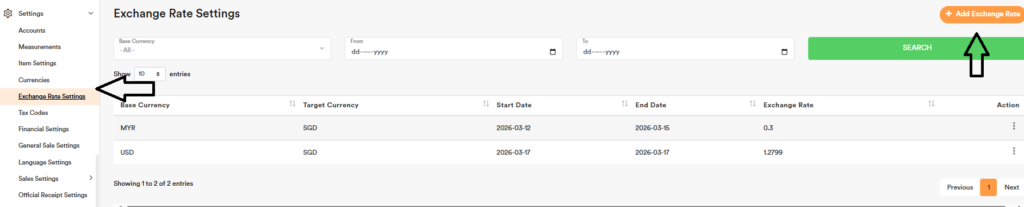

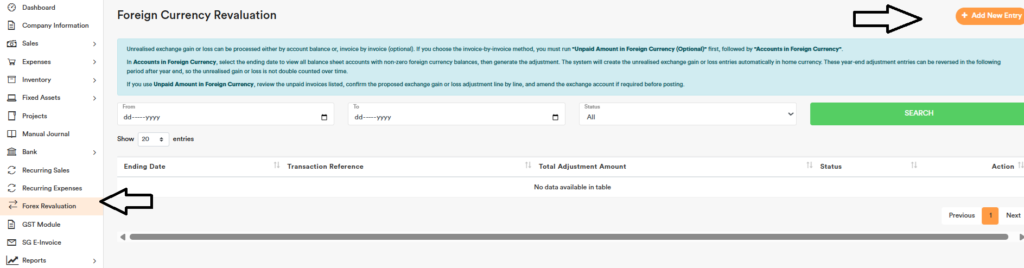

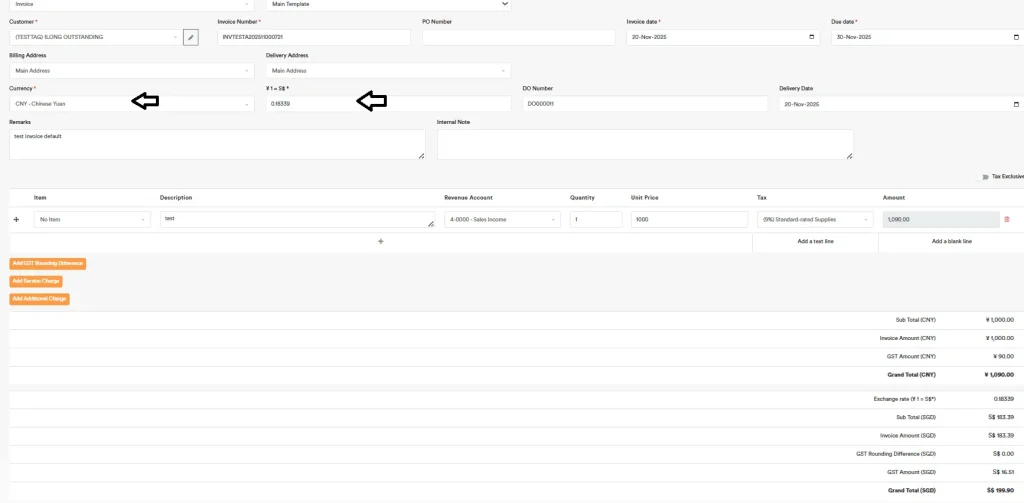

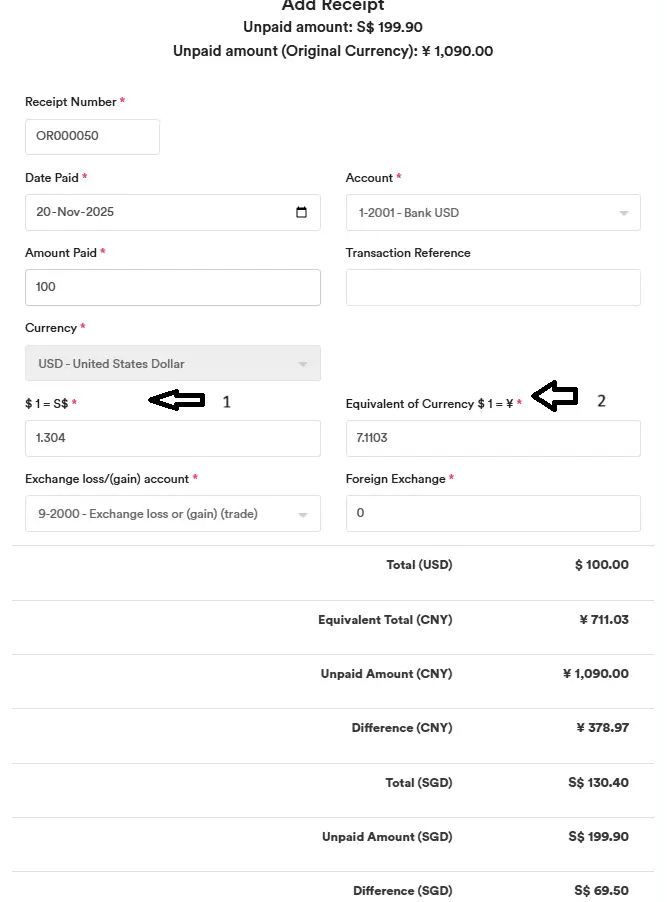

Exchange Rates

The exchange rates used in this software are retrieved automatically via API from Exchangerate-API ( https://www.exchangerate-api.com ). Their rates are compiled from central banks that publish daily reference rates and recognised financial market data providers, and are documented here: https://www.exchangerate-api.com/product/our-exchange-rate-data

IAS 21 The Effects of Changes in Foreign Exchange Rates does not prescribe any specific source of exchange rates; it requires the use of a reliable, observable market-based spot rate. Because Exchangerate-API’s rates are derived from multiple independent market sources and reflect indicative mid-market spot rates, they are appropriate for use under IAS 21 and equivalent local standards, and are generally acceptable to auditors and authorities such as MAS, ACRA, IRAS, IRB and similar bodies.

Our system uses live market rates, updated automatically from these sources. This is a stronger and more defensible approach than using a single fixed “monthly rate,” which some companies apply for convenience. A fixed monthly rate can deviate significantly from actual market conditions during the month, leading to less accurate translation of transactions and unrealised gains or losses, and weakening the link to the spot rates required by IAS 21.

Accordingly, it is advisable to use the exchange rates provided by our system rather than setting your own arbitrary monthly rate. Using live, transparent, market-based rates improves accuracy, aligns better with accounting standards, and provides a clearer, more supportable basis if your figures are reviewed by auditors or government authorities.

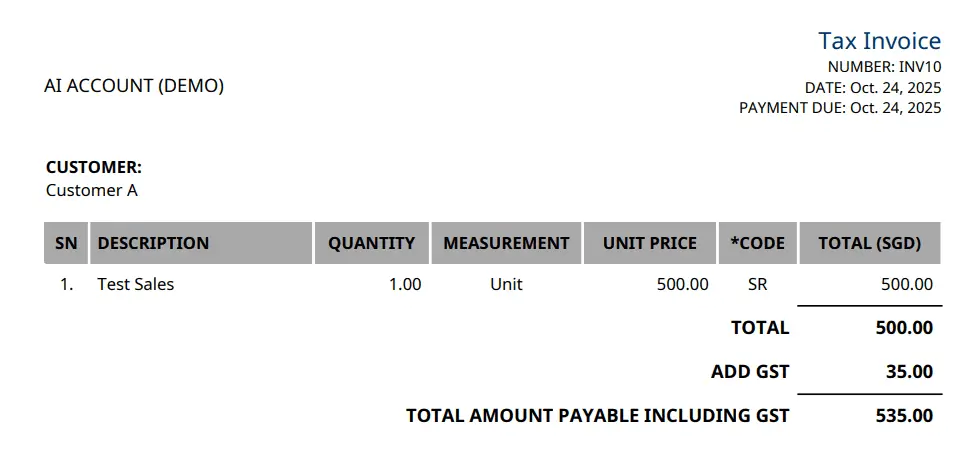

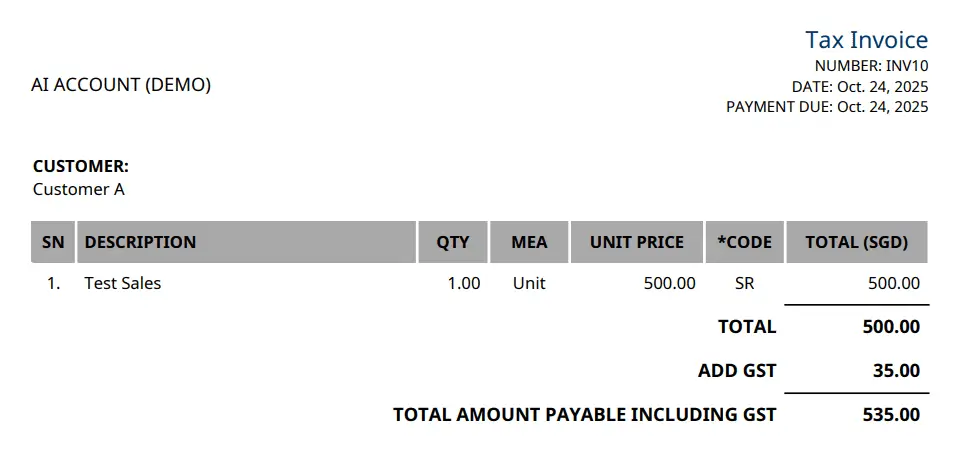

Unit Price

Unit Price supports up to 6 decimal places. If the calculated amount (Quantity × Unit Price) is less than 0.01, it will be rounded up and displayed as 0.01.

Accounting Automation

AI Account is working hard to stay at the forefront of AI automation. We currently offer the following automation features:

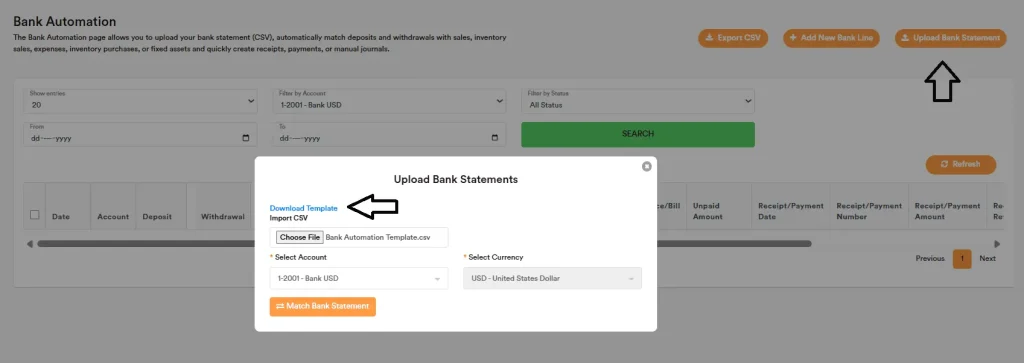

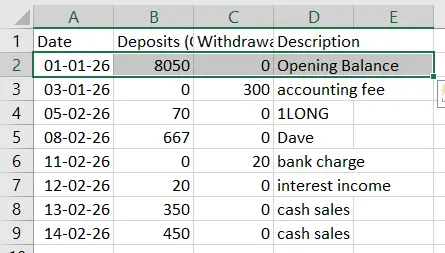

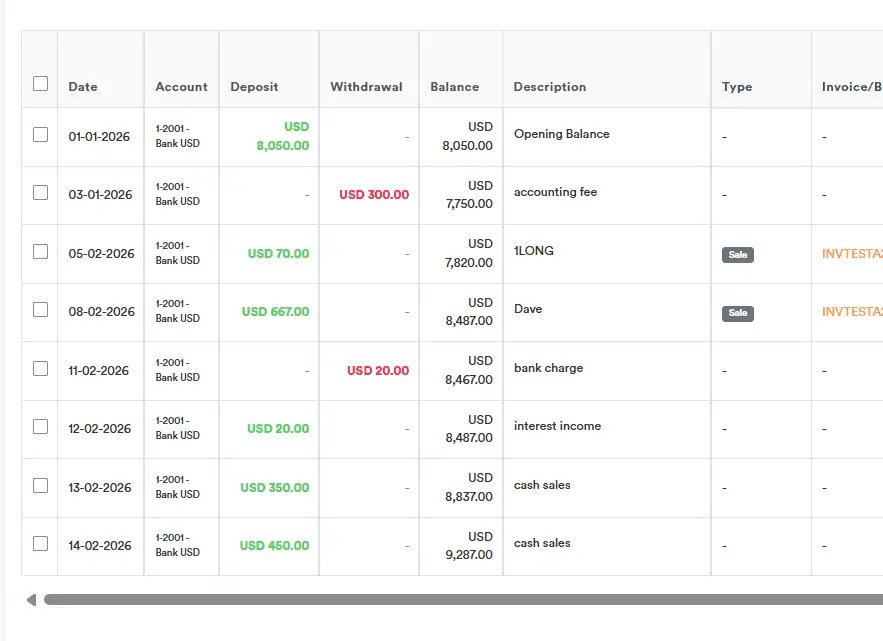

- Bank Reconciliation Automation – Easily upload your bank statements and let us automatically perform the reconciliation and matching for you.

- Bank Automation – Upload your bank statements and let the system automatically match each line to existing receipts, payments, and outstanding invoices or bills, while giving you the option to quickly create new receipts or journal entries where needed.

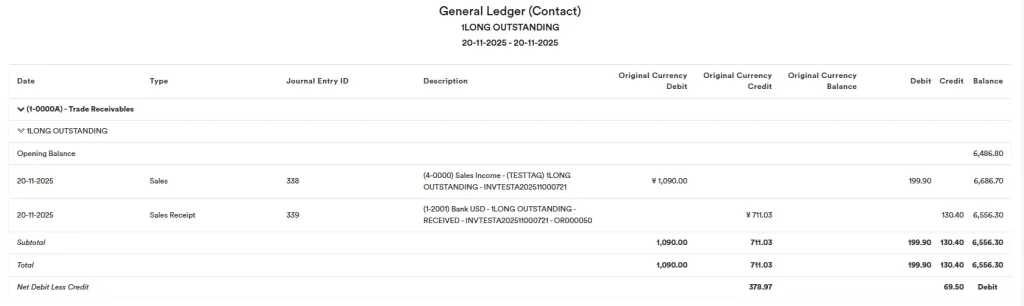

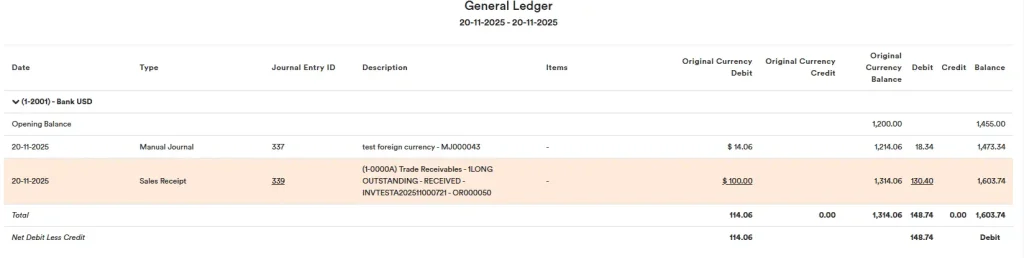

- Foreign Currency Exchange Gain/Loss – Exchange gains and losses are automatically calculated for you as you enter foreign currency transactions.

- Sales Recurring – Automatically generate invoices for your customers on a monthly, quarterly, half-yearly, or yearly basis, clearly showing the service period.

- Fixed Asset Automation – Automatically generate depreciation entries for your fixed assets and produce the fixed asset note to the accounts for you.

- Financial Performance Summary – combines key financial figures and ratios into a clear snapshot of profitability, cash flow, and efficiency, helping management and investors make faster, better-informed decisions without complex manual work.

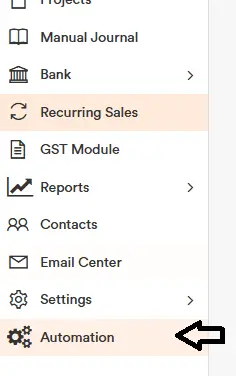

For more AI automation features and detailed walkthroughs, go to the Automation tab. There, you can find videos showing exactly how each process works, including how to:

- OCR to read expense and sales invoices, capture key details, and automatically prepare the double-entry postings.

- Matches unpaid invoices and bills to bank statement transactions and auto-generates the related receipt and payment entries.

- Imports bank statements, structures the data, and gets it ready for automated bank reconciliation.

- Imports opening balances and maps them to the correct ledger accounts for fast, accurate setup.

- Help you generate financial statements with minimal manual work.

Next-Gen AI Accountant

The AI Account Agent (BETA version) is a powerful intelligent agent that works like an autonomous accountant directly inside your software. Its true strength lies in its advanced reasoning capabilities, which allow it to go far beyond simple data processing.

Instead of just recording data, it analyzes context, cross-references information across documents, and applies sophisticated accounting logic to make complex decisions automatically. It can handle ambiguous transactions, infer missing details with high accuracy, instantly update your financial accounts, and dramatically streamline your entire accounting workflow.

Just like chat, you can chat with our agent, upload files, and it will automatically organize your data, complete your entries, detect and resolve issues, and post the entries into your accounting system — without you ever needing to open your accounting software. Everything is done in the chat, and your accounts are taken care of.

Contact our consultant to book a demo.

Key Functions

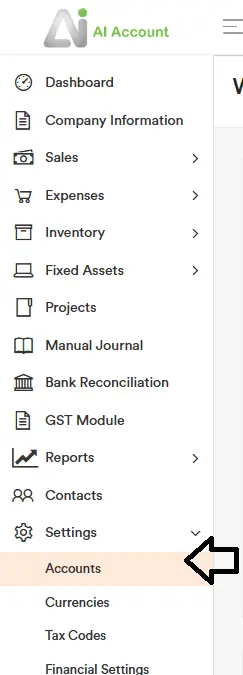

Chart of Accounts Setup

You can set up your Chart of Accounts at ‘Settings’ → ‘Accounts’

Chart of Accounts is created by default, suitable for most SMEs. You can add a new account or import one if needed.

The default chart of accounts is tailored to your country. For example, if the company is created as Malaysia, it will show EPF, SOCSO, and EIS accounts; if created as Singapore, it will show CPF accounts.

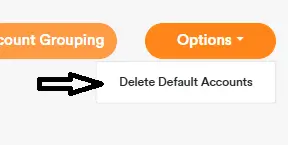

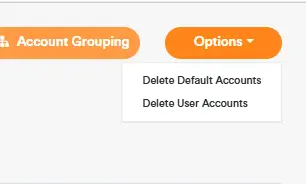

You can delete all default accounts and set up your own list using the top-right button, “Delete Default Accounts.”

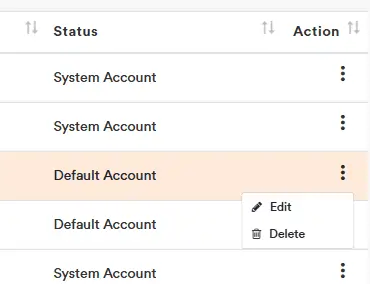

You can edit or delete individual default accounts from the Action menu.

Accounts that are in use by transactions cannot be deleted.

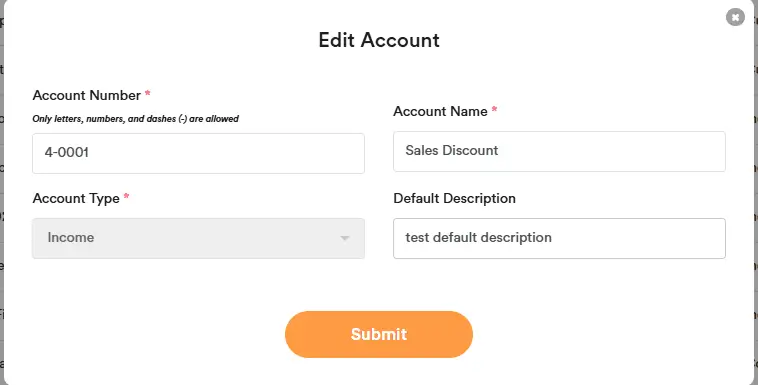

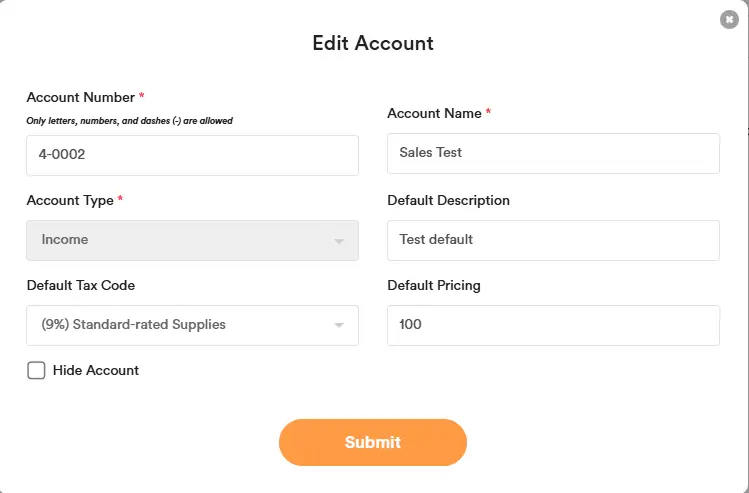

Chart of Accounts – Account Number and Name

Account Number (Account #)

Account numbers in the Chart of Accounts cannot be duplicated. The numbers 1-0000 and 10000 are treated as the same number and therefore cannot both exist at the same time, as this would be considered a duplicate.

Account Name

System account names cannot be duplicated. Other (non-system) account names can be duplicated.

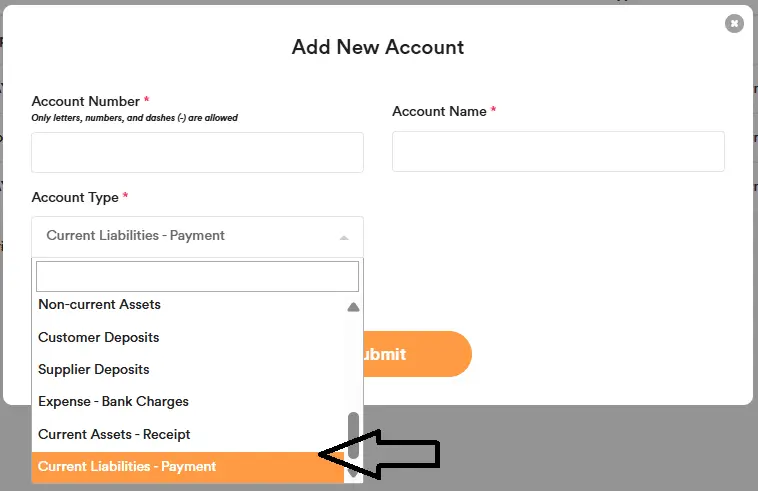

Chart of Accounts – Account Type

Use these account types when setting up your Chart of Accounts:

- Bank — For bank accounts and cash on hand. Selectable on payment and receipt transactions.

- Current Assets — For prepayments and deposits. Also used for trade receivables and inventory system accounts.

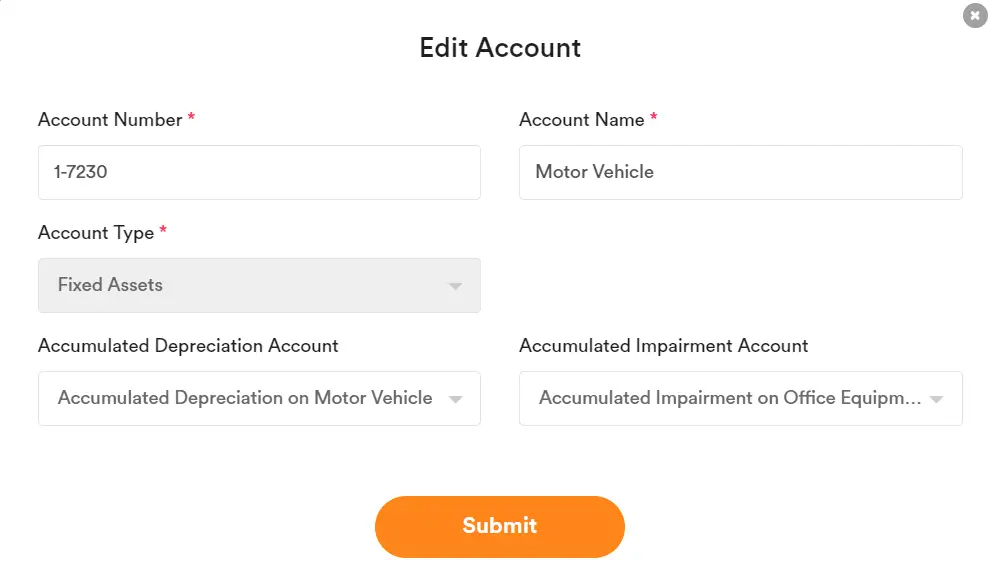

- Fixed Assets — For fixed assets. Selectable in the Fixed Assets and Expenses module.

- Income — For sales revenue. Selectable on sales transactions.

- Other Income — For non-operating income. Selectable in manual journals.

- Cost of Sales — For costs directly tied to sales. Selectable in the Expenses module.

- Expense — For operating expenses. Selectable in the Expenses module.

- Other Expense — For non-operating expenses (e.g., interest on borrowings, income tax, exchange gains/losses). Selectable in manual journals.

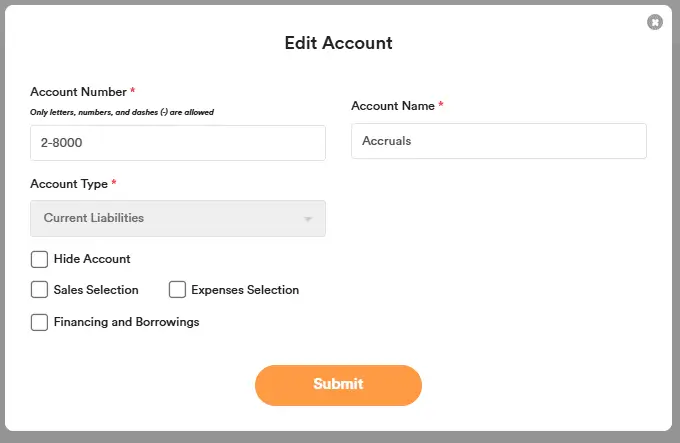

- Current Liabilities — For accruals, advance receipt, and short-term borrowings. Also used for trade payables and GST payables system accounts.

- Non-current Liabilities — For long-term borrowings.

- Equity — For share capital and similar equity accounts.

- Non-current Assets — For long-term investments.

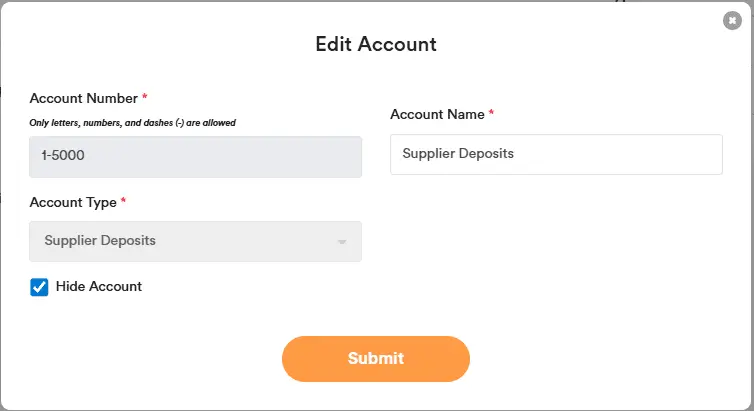

- Customer Deposits — For deposits received from customers. Selectable on sales and receipt transactions.

- Supplier Deposits — For deposits paid to suppliers. Selectable on expenses and payment transactions.

Inventory system accounts are fixed and managed by the system — no setup or mapping is required. The system automatically posts to Inventory (asset) for stock movements, Sales (revenue) for sales transactions, and Cost of Goods Sold (expense) when inventory is sold.

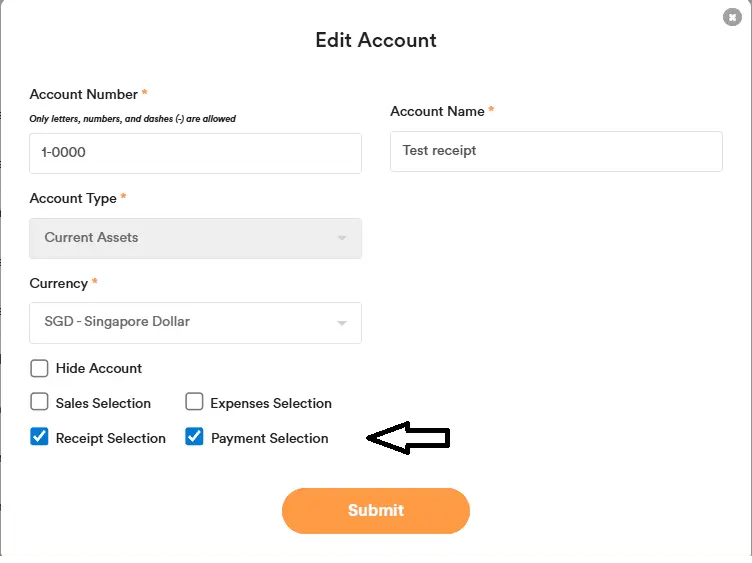

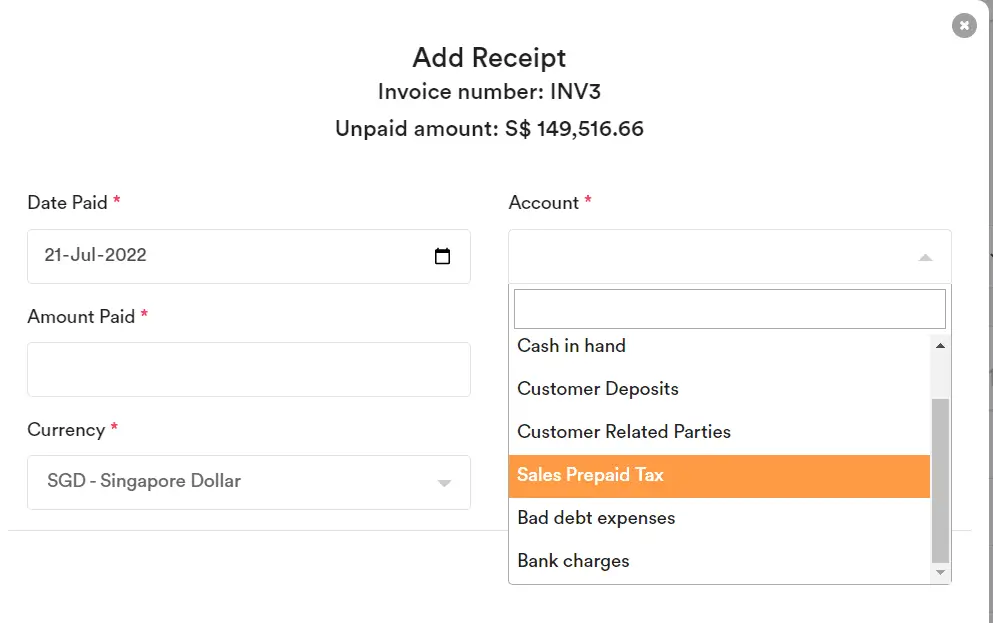

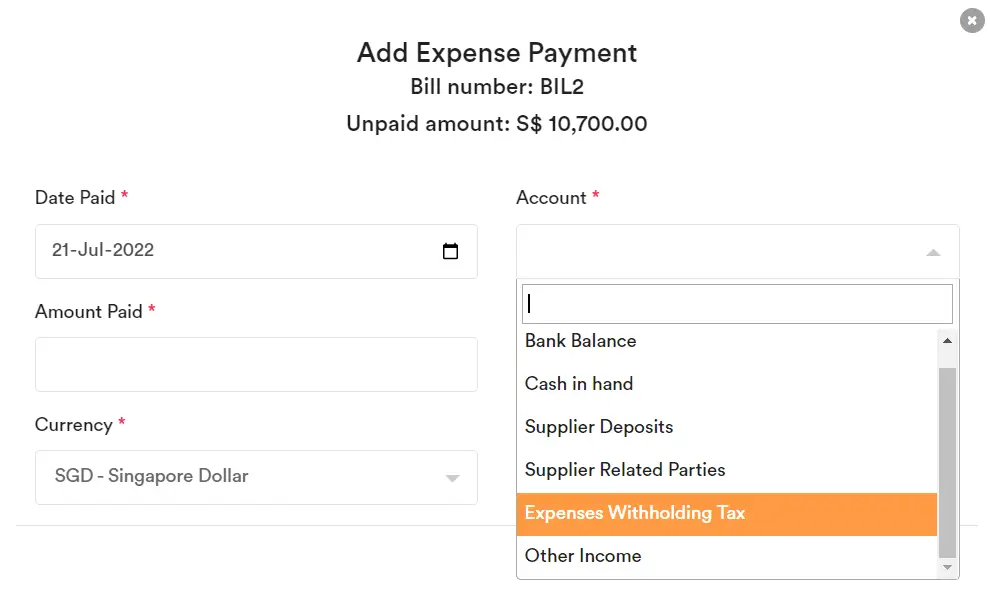

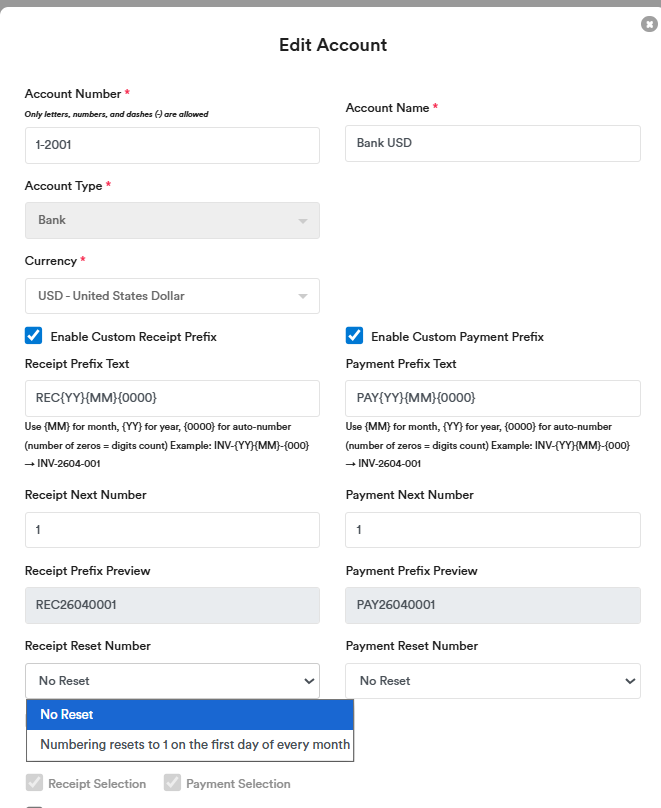

Chart of Accounts – Receipts and Payments

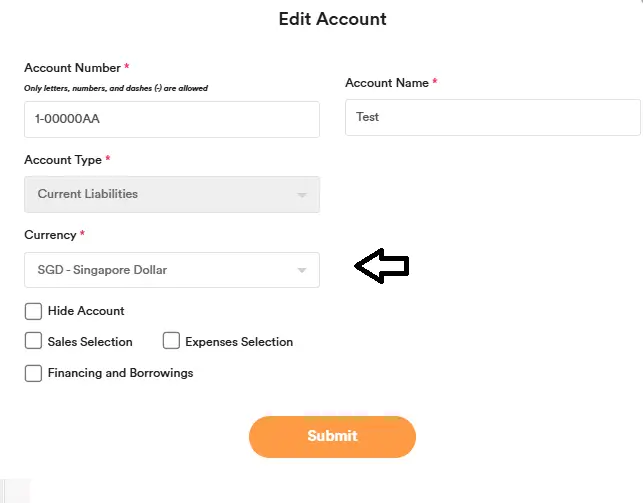

For any account that you want to be selectable when recording receipt or payment transactions, you can tick the relevant options in the Chart of Accounts as shown below.

If you tick “Receipt Selection”, the account can be selected when creating a receipt, e.g.:

1-8000 Sales Prepaid Tax

If you tick “Payment Selection”, the account can be selected when creating a payment, e.g.:

2-4100 Expenses Withholding Tax

Chart of Accounts – Sales and Expenses Selection

Some accounts cannot be selected under Sales or Expenses by default, such as accrual accounts. If you want to use an account in the Expenses section, go to the Chart of Accounts, select the account you want, and tick ‘Sales Selection’ if you want to allow that account to be selected in the Sales section, or ‘Expenses Selection’ if you want to allow it to be selected in the Expenses section. Then click Submit.

Important note: For each Chart of Accounts entry, do not tick both “Sales Selection” and “Expenses Selection”. Select only what the system recommends for that account type. We highly recommend using the system-suggested selection only and not ticking any extra options, to ensure transactions flow into the correct e-Invoice module and to avoid missing records.

Example: Do not tick “Sales Selection” for Expense, Cost of Sales, and Fixed Asset account types. If these expense transactions are recorded in the Sales module, they will not appear in the Self-Billed e-Invoice module, and you will need to issue a Manual Self-Billed e-Invoice for these special postings. Conversely, do not tick “Expenses Selection” for Income account types. If sales transactions are recorded in the Expenses module, they will not appear in the e-Invoice Sales section, and you will need to issue a Manual e-Invoice for those cases.

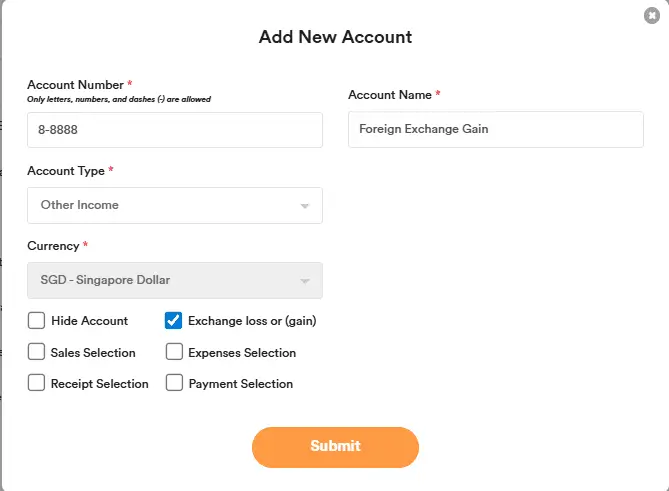

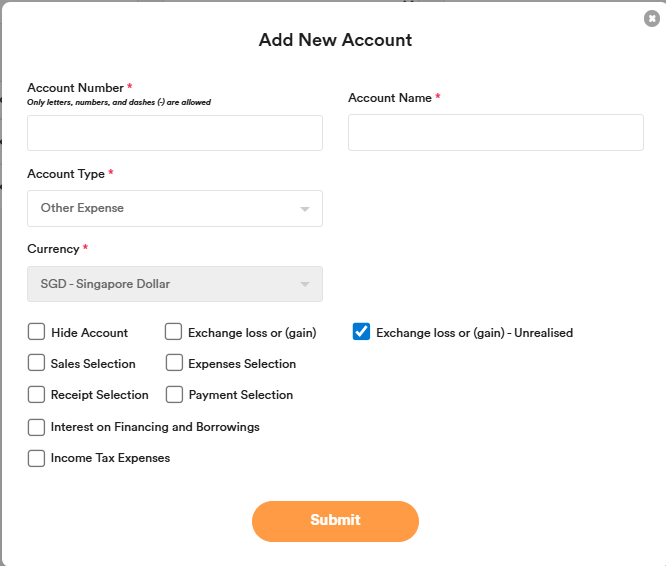

Chart of Accounts – Exchange Loss/Gain Selection

For the following five account types:

- Income

- Other Income

- Cost of Sales

- Expense

- Other Expense

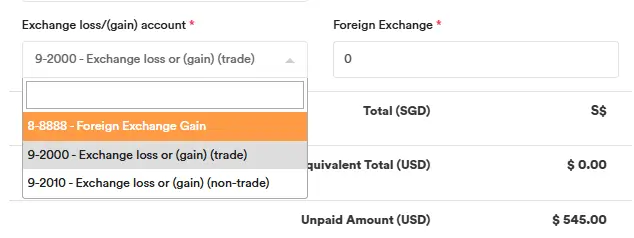

You can tick the optional checkbox: “Exchange loss or (gain)”. If this option is selected, the account will appear in the *“Exchange loss/(gain) account ” field for selection when recording a payment or receipt.

Example: Create a foreign exchange account and set its type to Other Income. It will appear under Other Income in the Profit and Loss report.

When creating a payment or receipt, the account will be available in the dropdown list.

For the existing system exchange gain/loss account, you can choose to hide it if you don’t want to use it.

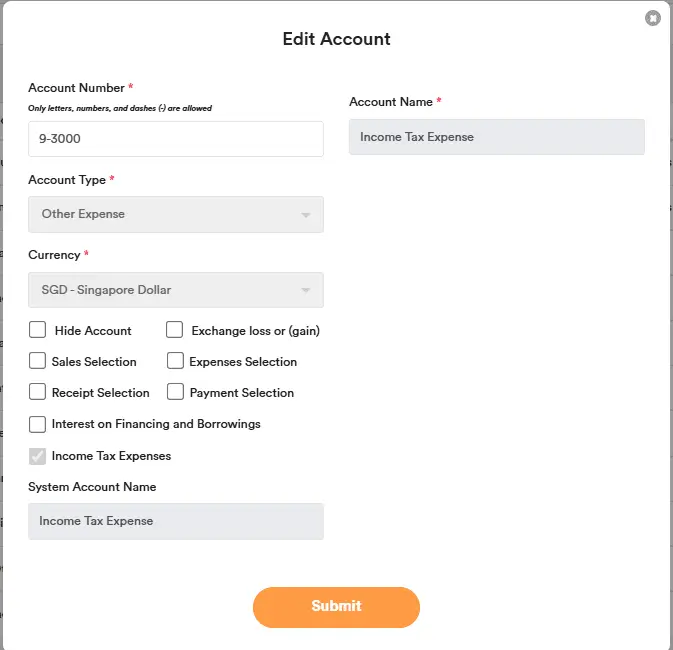

Chart of Accounts – Income Tax Expenses

You can use the system account – Income Tax Expense to record your corporate income tax expenses.

Alternatively, you can create your own income tax expense account by selecting Account Type = ‘Other Expense’ and ticking ‘Income Tax Expenses’.

In the Profit and Loss report, the income tax expense account will appear in a separate section, allowing you to calculate profit before tax and net profit after tax.

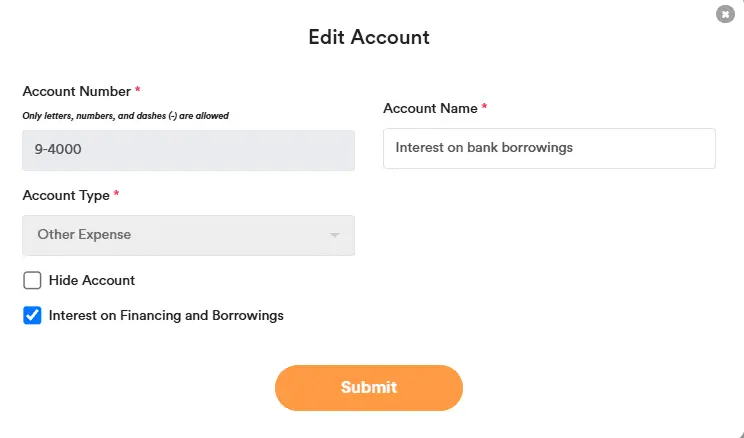

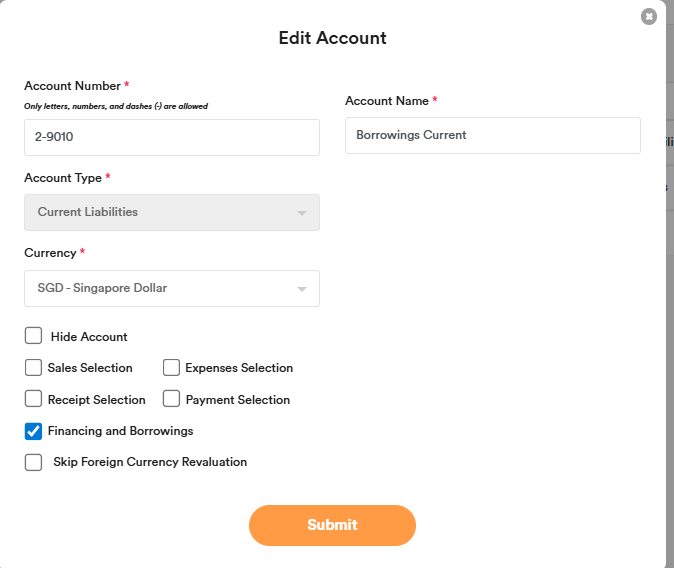

Chart of Accounts – Borrowings

Borrowings are interest-bearing debts (e.g., bank loans, credit lines).

Record short-term portions under ‘Current Liabilities’; longer terms under ‘Non-current Liabilities’.

Use an ‘Other Expense’ account type for interest charges.

If the account type is Current Liabilities or Non-current Liabilities, tick ‘Financing and Borrowings’.

If the account type is Other Expense, tick ‘Interest on Financing and Borrowings’.

After these settings are applied, the cash flow statement will report these accounts under Financing activities.

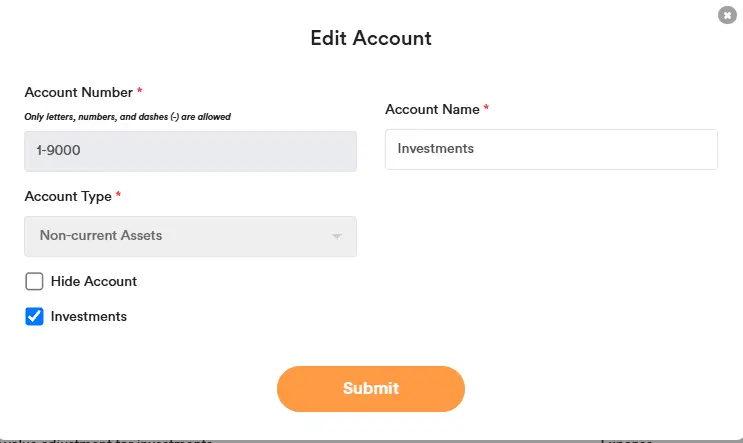

Chart of Accounts – Investments

Investments are long-term financial assets we hold (over 12 months).

Record them as Non-current Assets.

If the account type is Non-current Assets, tick ‘Investments’.

After these settings are applied, the cash flow statement will report these accounts under Investing activities.

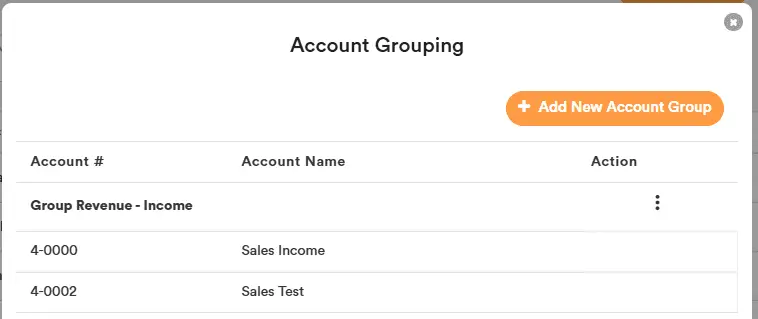

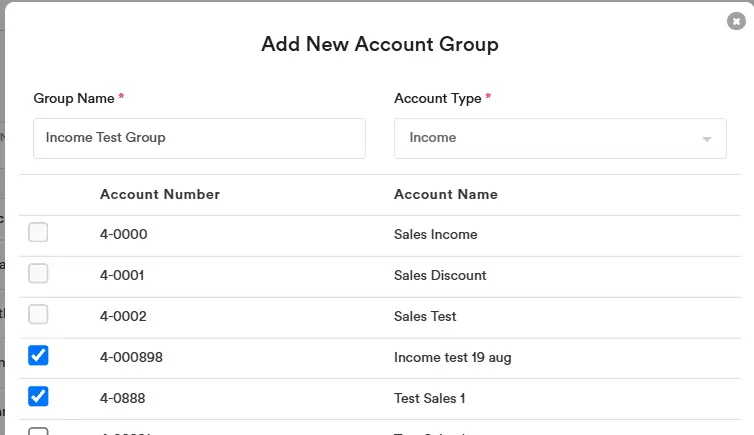

Chart of Accounts – Account Grouping

In the Accounts section, you can configure Account Grouping (via the top right button) and then generate the Balance Sheet (Group) and Profit and Loss (Group) reports, which will reflect the groupings you’ve defined.

Click Add New Account Group.

Select the Account Type you want to group, enter the Group Name, and choose the accounts to include for reporting. Thereafter, click on ‘Create Grouping’.

Note: You cannot post double-entry journals or transactions to the Account Group. It’s for header-level reporting/presentation only.

Chart of Accounts – System Account

You may rename, delete, or hide any default account (e.g. Sales, Expenses).

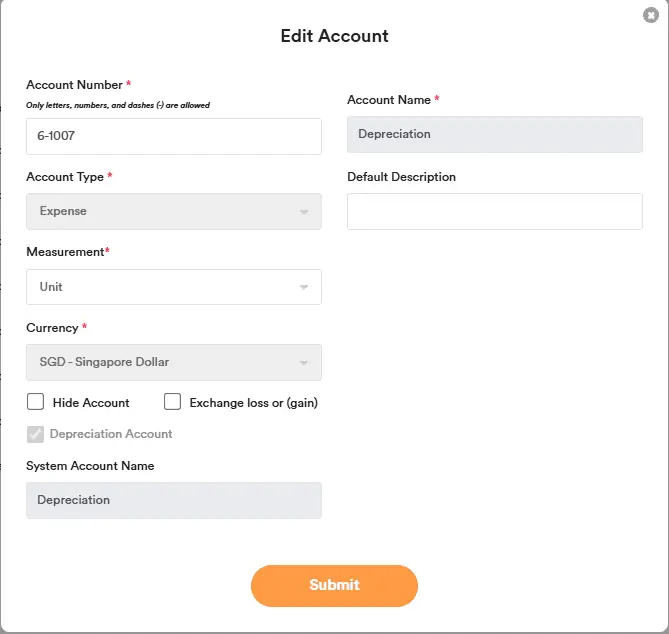

However, the following system accounts (Status = System Account) are locked for automation. You may change their account numbers if needed, but you cannot delete them:

- Trade Receivables

- Other Receivables

- Inventories

- Trade Payables

- Other Payables

- GST Payables

- Expenses Withholding Tax

- Retained Earnings

- Sales Inventories

- Service Charges

- Sales of Fixed Assets

- Cost of Goods Sold

- Depreciation

- Impairment Loss

- Loss or (Gain) on Disposal

- Exchange loss or (gain) (trade)

- Exchange loss or (gain) (non-trade)

- Rounding Differences

- Others

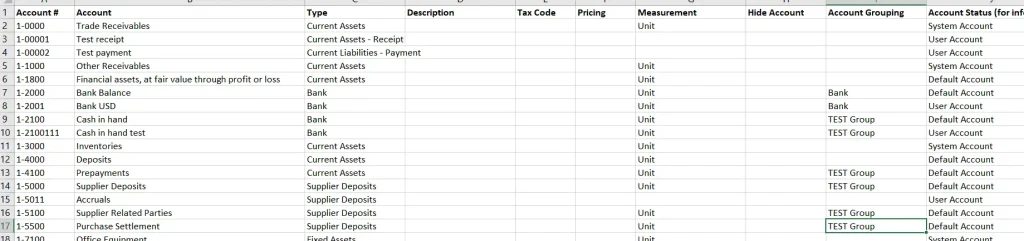

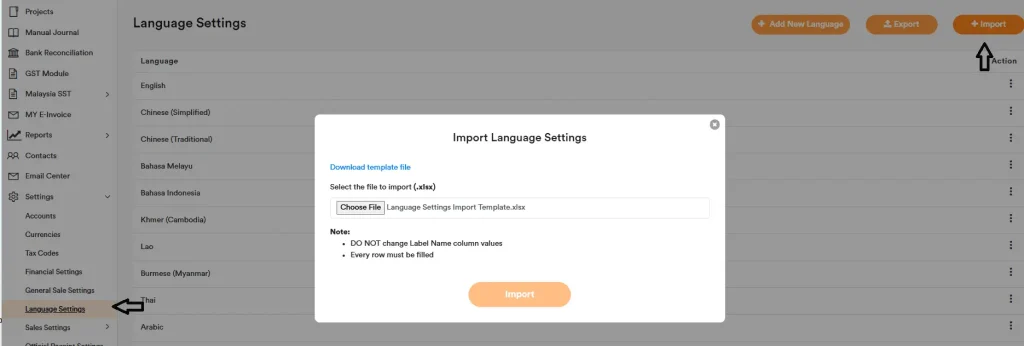

Chart of Accounts Export and Import

You can export the full chart of accounts to Excel using the ‘Export’ button, make your changes in Excel, and then import the file back into the system to update the chart of accounts. Note that some accounts—such as system accounts—cannot be modified; if you try, you’ll see a warning.

To hide unused accounts in bulk, import an Excel file where the ‘Hide Account’ column is set to “Yes” for the accounts you want to hide.

Fill in the Account Grouping in the Excel export.

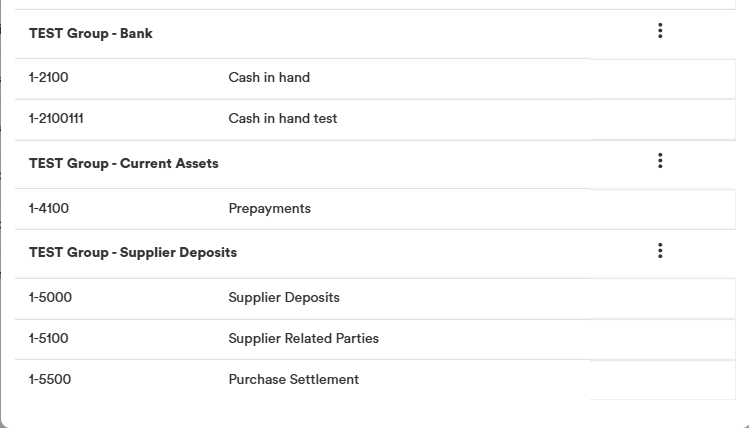

When you import the Chart of Accounts to update, the Account Grouping will be auto-created as shown below.

Chart of Accounts — Set Up Your Own

Some accountants prefer to use their own chart of accounts instead of the system default.

You can delete all default accounts and set up your own list using the top-right button, “Delete Default Accounts.”

After that, import the chart of accounts you previously exported from another company in AI Account. The new company will then have the same chart of accounts as the source company. For export/import instructions, see the previous Export/Import Chart of Accounts section.

You can delete all user accounts at any time if you’d like to start fresh.

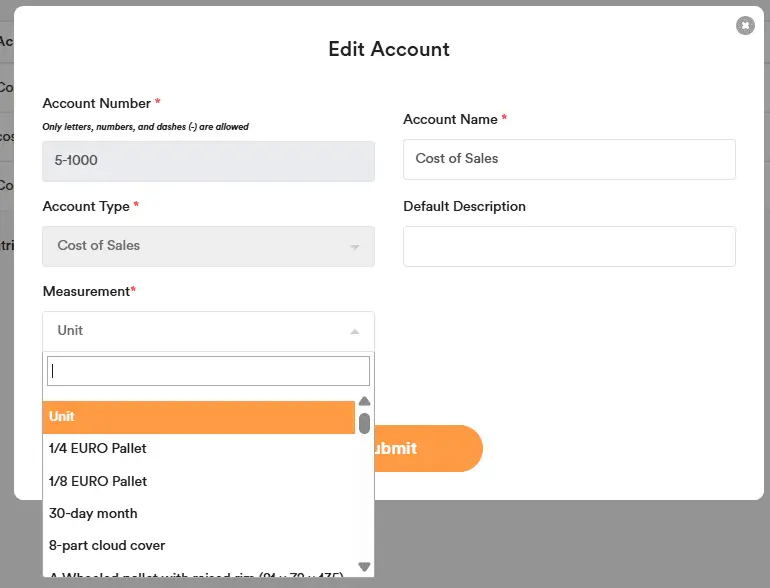

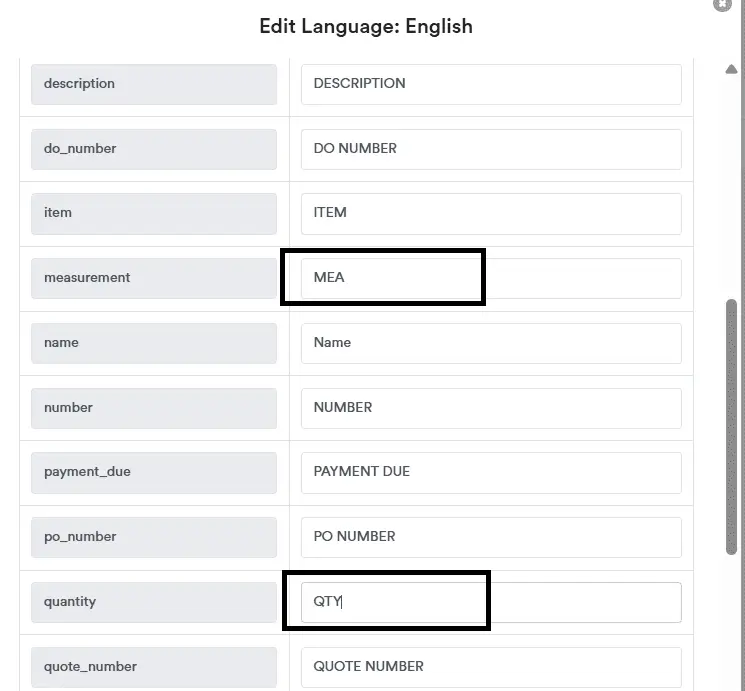

Chart of Accounts Measurement

For Account Type = Income, Expense, or Cost of Sales:

- You can set the Measurement (default: Unit).

- When you use these accounts in Sales or Expense transactions, the selected measurement appears next to the account name.

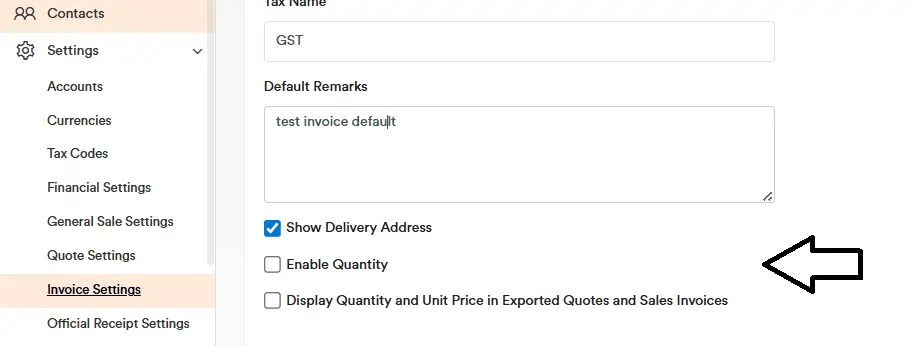

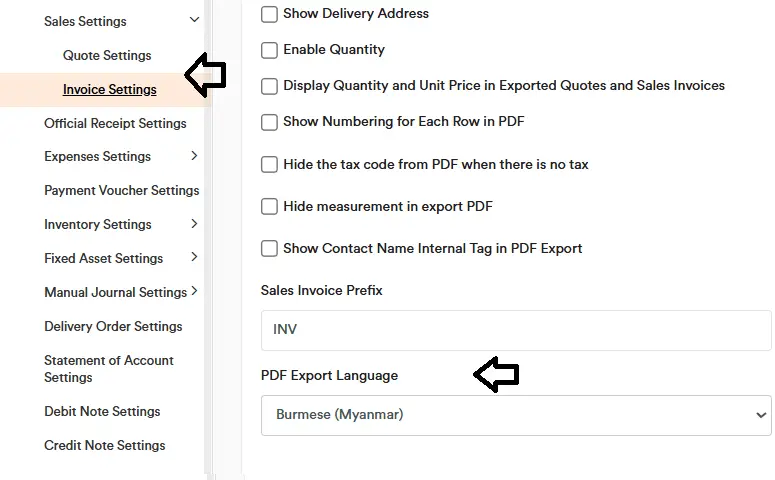

- To show the measurement on tax invoices, tick “Display Quantity and Unit Price in Exported Quotes and Sales Invoices” in Invoice Settings.

- This setup is suitable for recording inventory on a periodic basis.

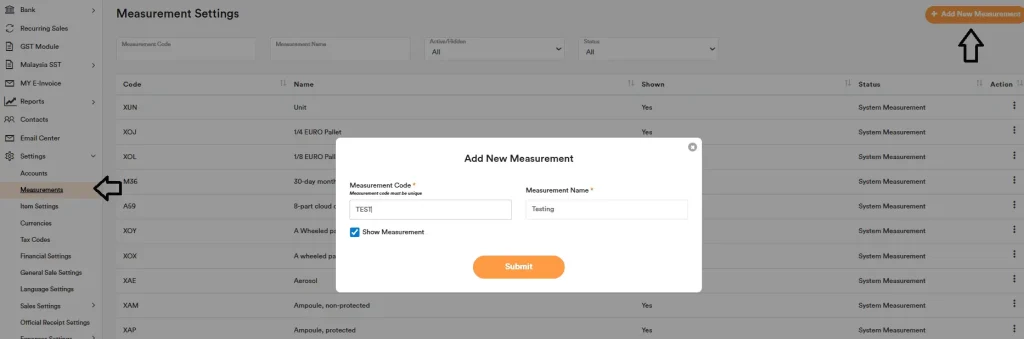

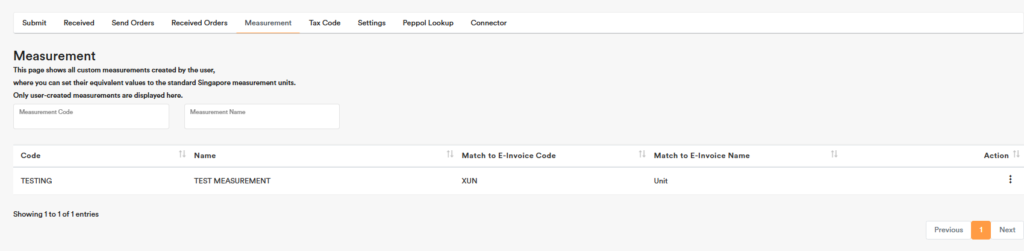

Measurement Setup

Go to Measurement, then click ‘Add New Measurement’ in the top-right corner to add your own measurement type.

Untick Show Measurement if you don’t want the measurement to be displayed.

“Unit” is the default measurement across all sections in general; it can’t be hidden.

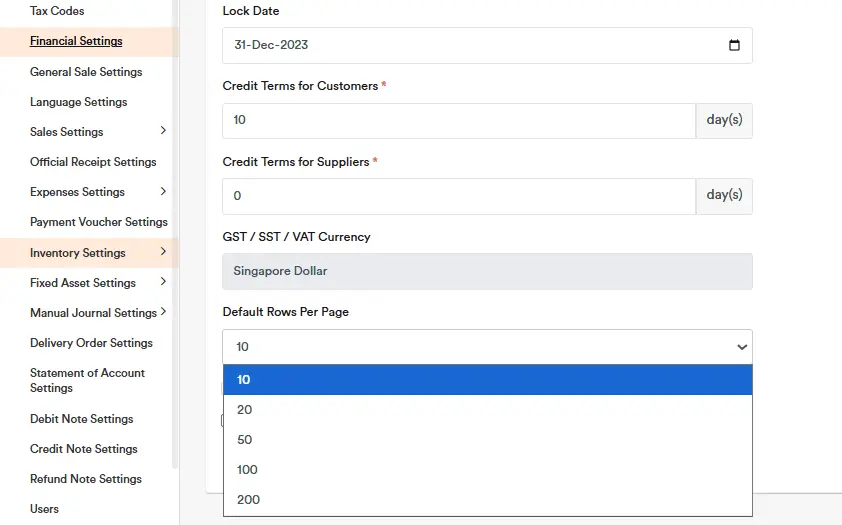

In the options at the top-right corner, you can choose either “Show all System Measurements” or “Hide all System Measurements except for ‘Unit’”, depending on your needs.

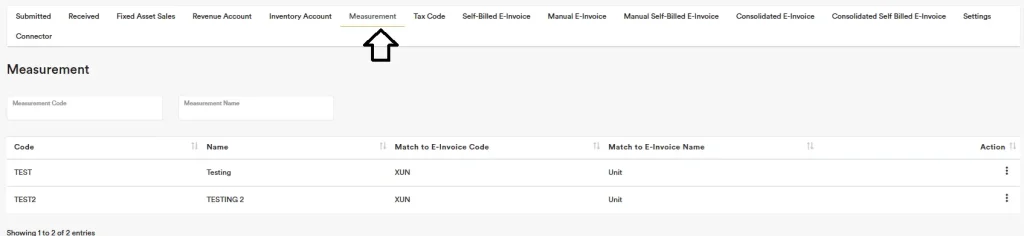

If you’re using the e-invoice feature, go to the E-Invoice → Measurement tab, and assign your custom measurement to the default government measurement you want submitted to the government.

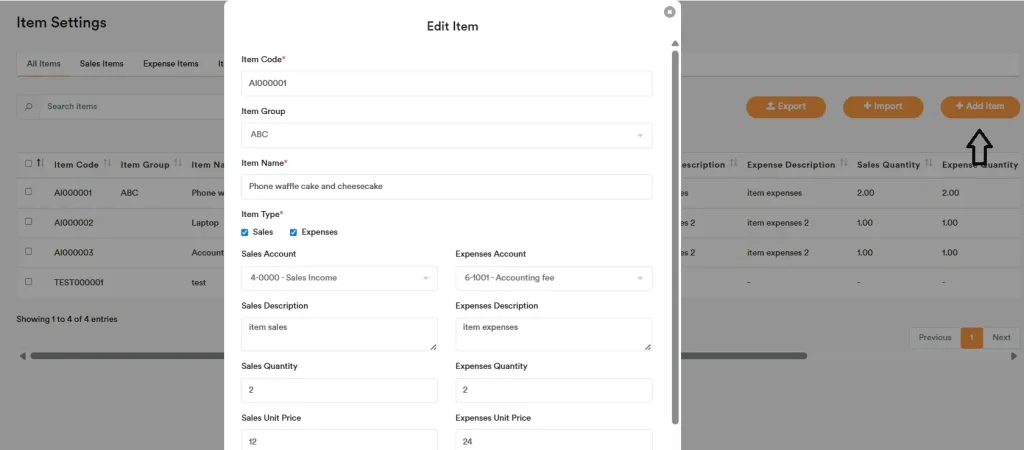

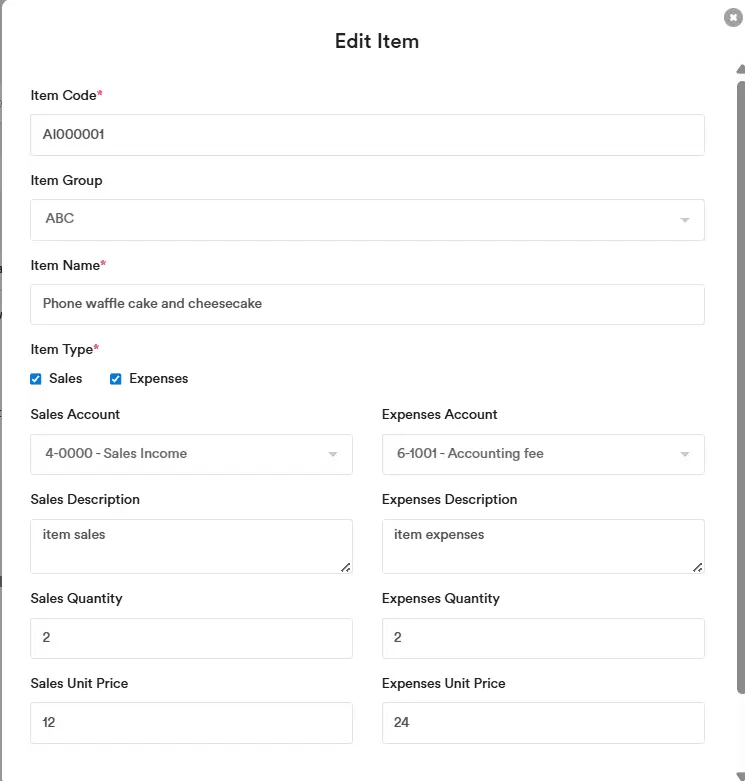

Items Setup

With AI Account, you can track the specific products and services used on each sales transaction line by using the Items feature.

This lets you manage multiple items — such as Consulting Services, Valuation Services, etc. — while posting them all to a single Chart of Account (e.g., Sales Income). You don’t need to create a separate account for each service. This is ideal when you have thousands of service types and it’s not practical to create individual accounts for each.

Items – Basic Setup

There are two item types: Sales items and Expense items.

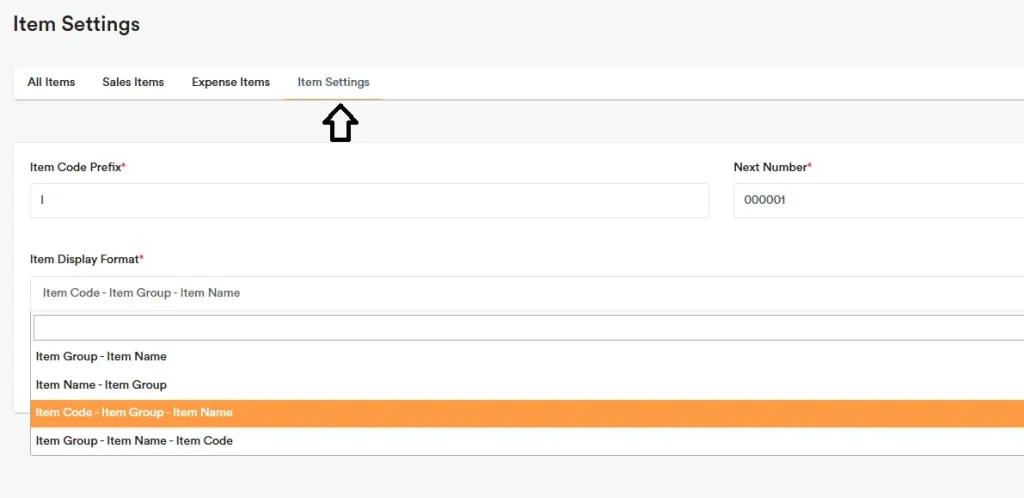

You can set a prefix number for the Item Code at ‘Item Settings’.

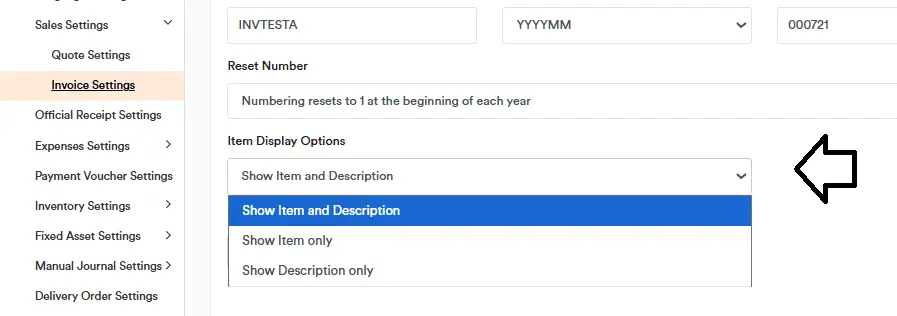

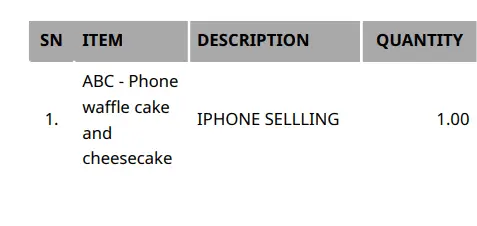

You can set your preferred Item Display Format in Item Settings, such as choosing not to show the Item Code.

To add an item, click ‘Add Item’ in the top-right corner.

The following fields are optional: Account, Description, Quantity, and Price.

- If you fill them in, these values will be used as defaults when the item is selected during sales or expense entry.

- For Sales Items, select an account that is used in sales transactions only (e.g., Sales Income).

- For Expense Items, select an account that is used in expense transactions only (e.g., Accounting Fees).

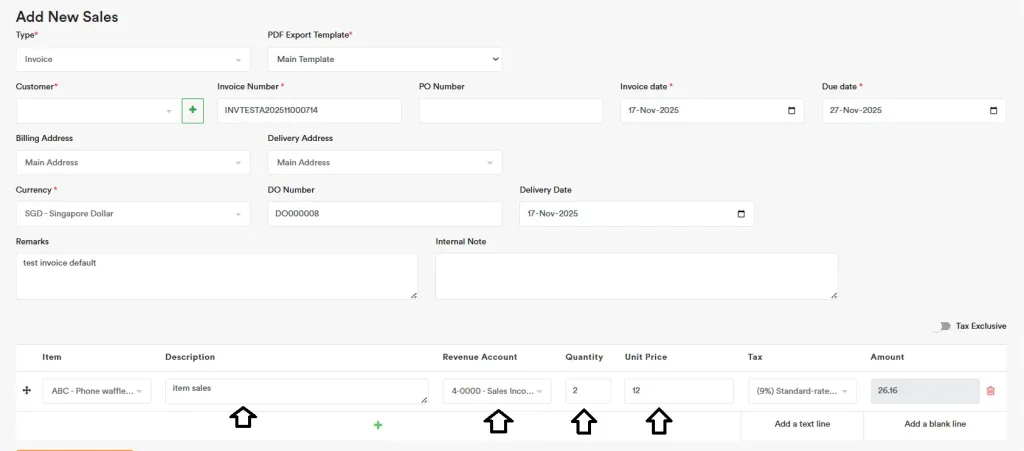

Example: If you create an item with all details completed, those details will automatically populate when you select the item on a sales record.

If you enable Default Tax, the tax will also be applied automatically — no manual selection required.

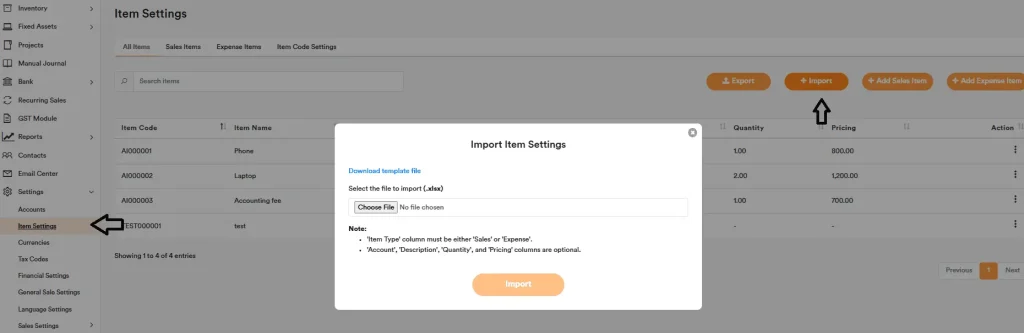

Items – Export and Import

Go to ‘Items Settings’ and click the Import button in the top-right.

Download the Template File, prepare the data, then upload and import it.

You can export the full Items to Excel using the ‘Export’ button, make your changes in Excel, and then import the file back into the system to update the Items list.

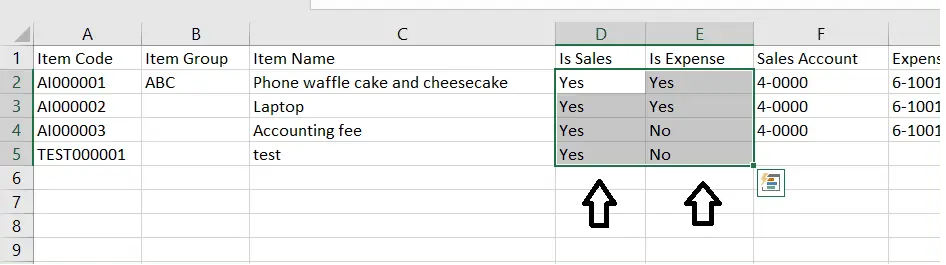

In Excel, if you set “Is Sales” to Yes, that item will appear in the Sales transaction selection. If you set “Is Expense” to Yes, that item will appear in the Expenses transaction selection.

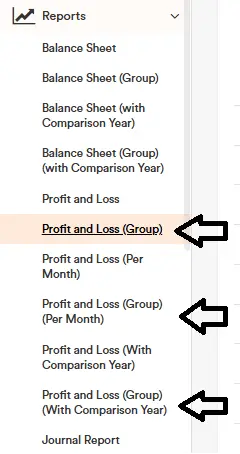

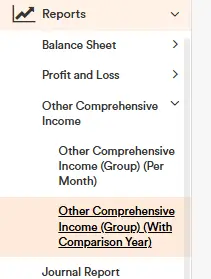

Items – Reports

You can see the item breakdown in the following report.

- Profit and Loss (Group)

- Profit and Loss (Group) (Per Month)

- Profit and Loss (Group) (With Comparison Year)

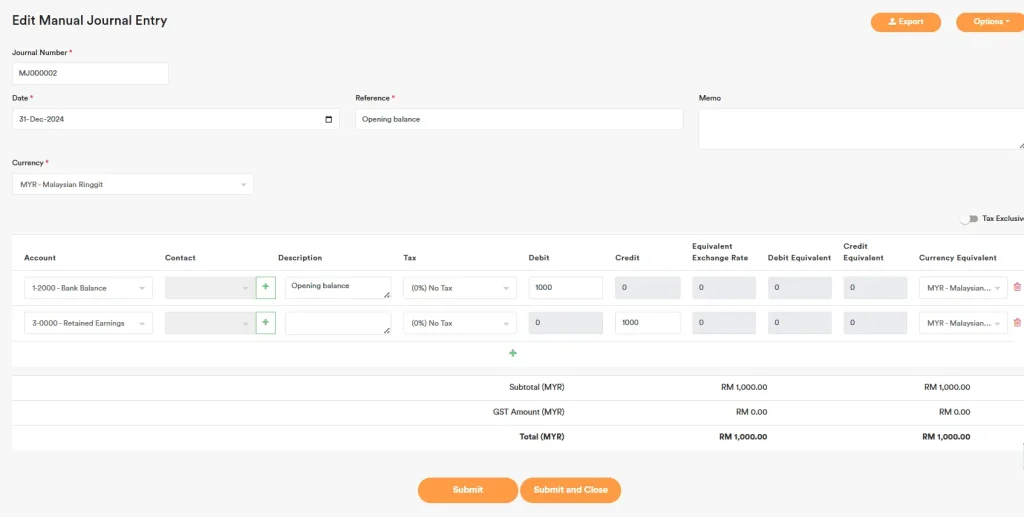

Opening Balance Recording

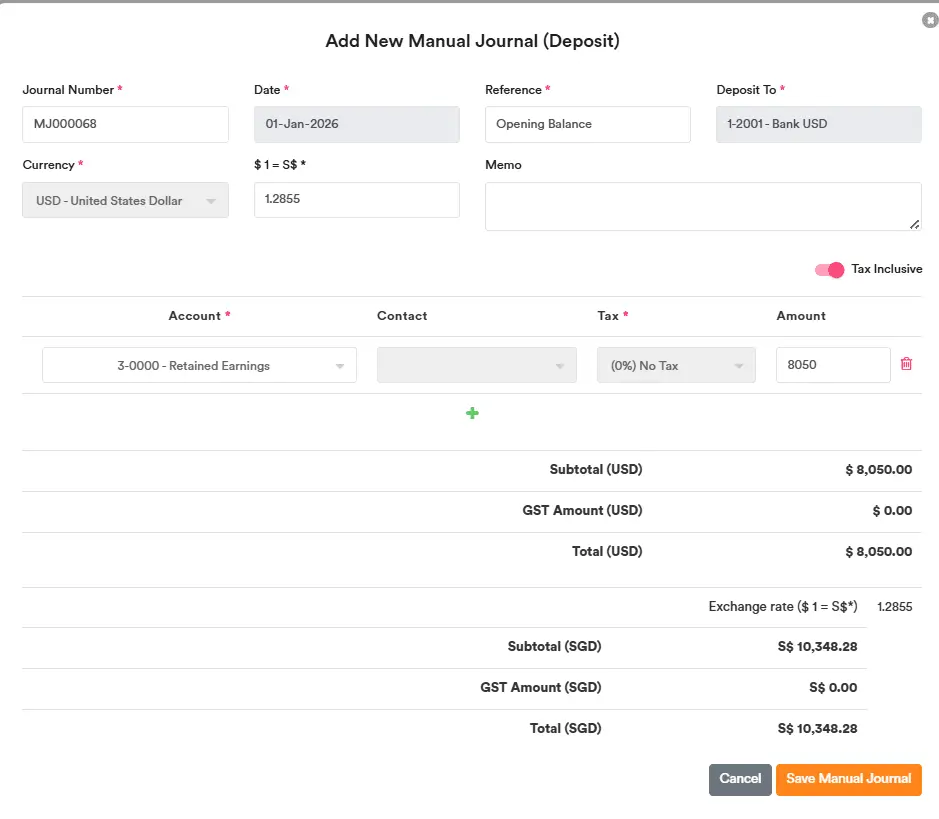

You can use Manual Journal entry to record opening balance. Example, the cut off is 1 Jan 2022, you are recommended to key in the opening balance on 31 Dec 2021. So when you generate the prior year balance sheet report on 31 Dec 2021, it can reflect the number accurately.

Watch the video below to learn how to enter your company’s opening balances using a manual journal.

Opening Balance Recording (Video)

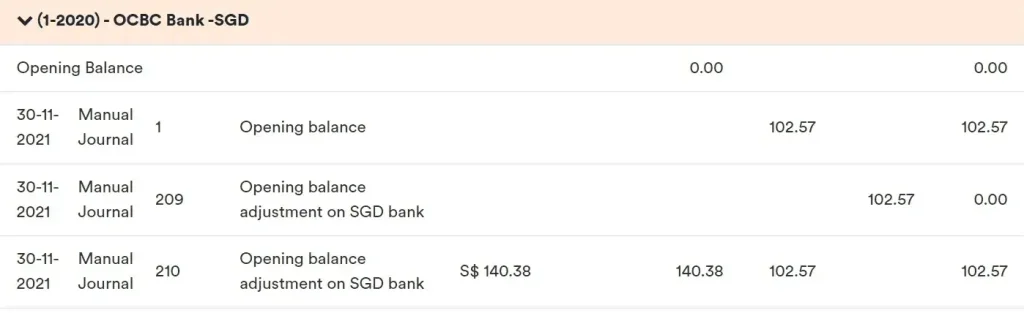

For foreign currency opening balances, you can record each in a separate manual journal, as each manual journal can record only one type of currency. Alternatively, you can record them in one manual journal and adjust it with another journal, as shown below.

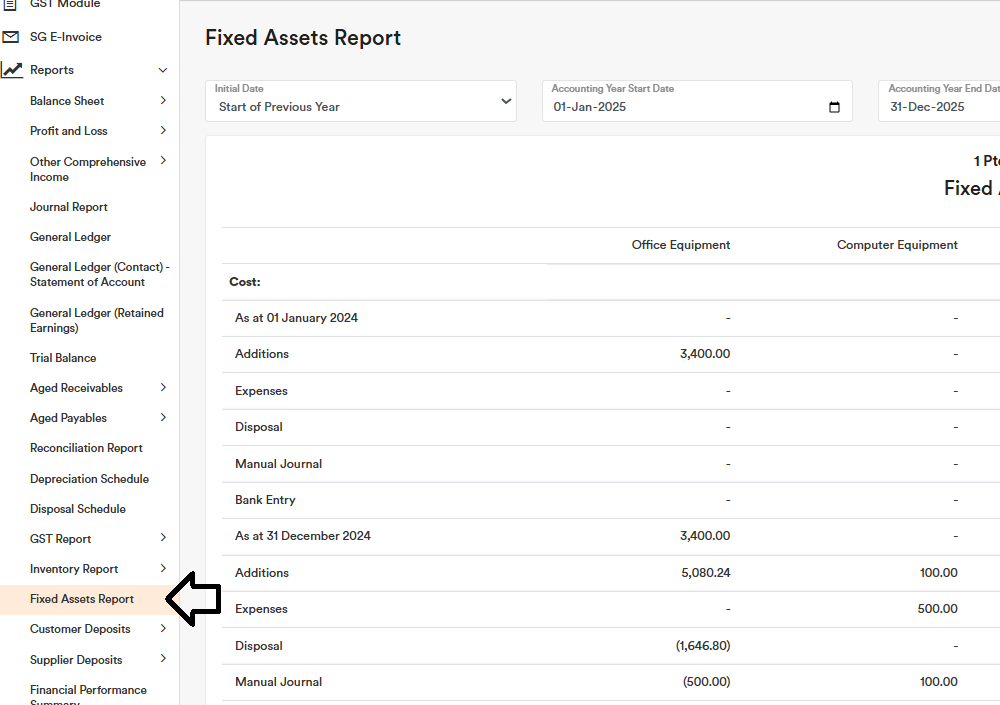

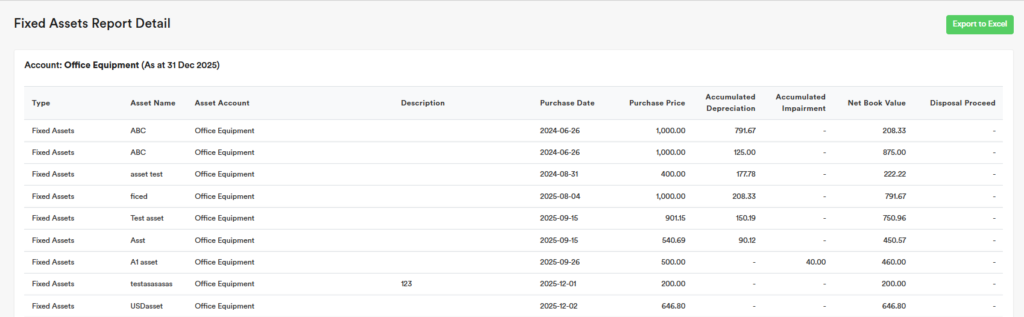

Opening Balance Recording (Fixed Assets Module)

Fixed Assets — how to bring in opening balances (simple example)

Some clients want to import fixed assets with full details. You can do this in the Fixed Assets module.

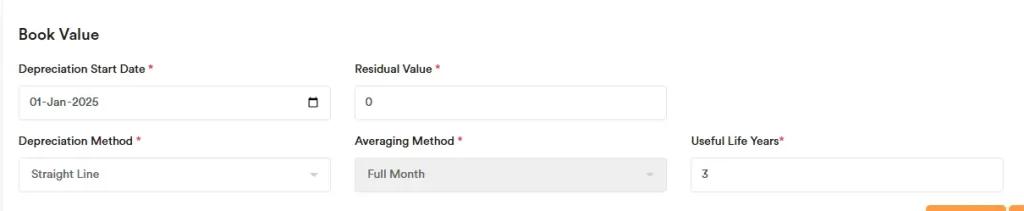

Example (numbers): Cost = $1,000, Accumulated Depreciation = $200. Opening balance date = 1 Jan 2025.

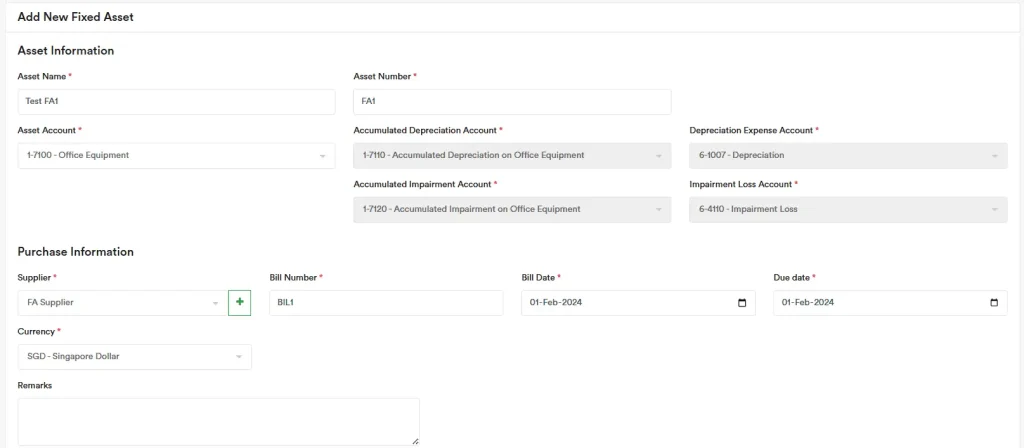

Step 1 — Add the asset

Enter the asset with its original purchase date and original cost ($1,000).

Step 2 — Set depreciation

Depreciation start date: use your opening balance date (e.g., 1 Jan 2025).

Remaining useful life: set the years left from the opening balance date (total life minus the years already used).

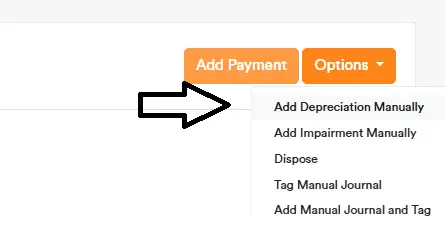

Step 3 — Bring in accumulated depreciation ($200)

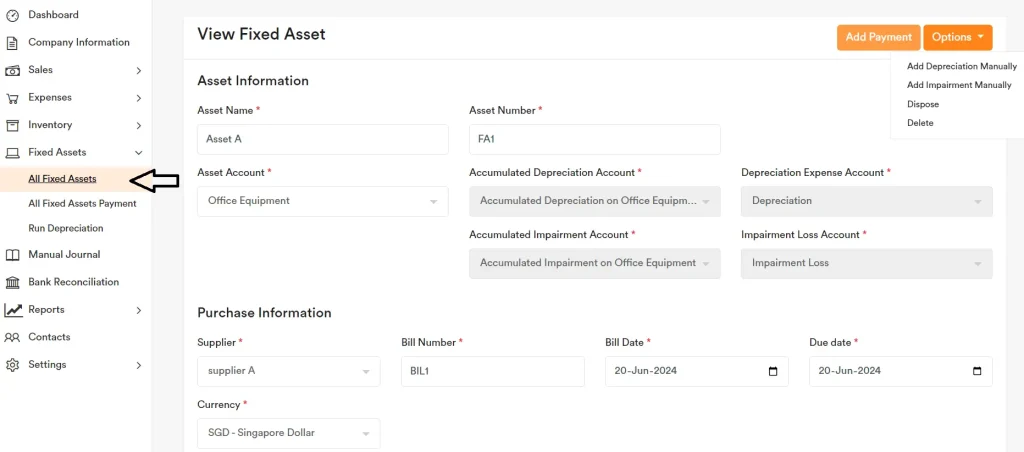

From the top-right menu, select ‘Add Depreciation Manually’ to record prior depreciation. Use a date before the opening balance (e.g., 31 Dec 2024), then post::

Dr Depreciation expenses $200

Cr Accumulated Depreciation $200

Step 4 — If the asset was already paid in a previous year

You may also record the payment (credit bank) using the appropriate past date.

Effect of Steps 1–4 (illustration):

Fixed Asset + $1,000

Accumulated Depreciation – $200

Bank Balance – $1,000

Depreciation Expense + $200

Compare to your assumed actual opening balances (example as at 1 Jan 2025):

Bank Balance + $2,000

Fixed Asset + $1,000

Accumulated Depreciation – $200

Retained Earnings – $2,800

Step 5 — Bring the bank to the true opening amount with one manual journal

To move bank from –$1,000 (after you re-entered the old payment) to the actual opening +$2,000, post manual journal entry on 31 December 2024:

Dr Bank + $3,000

Cr Retained Earnings – $3,000

This single entry aligns the books so the final opening balances tally on 1 Jan 2025.

Note: The $200 prior-year depreciation you posted (dated 31 Dec 2024) closes into Retained Earnings at year-end, which is why it’s not shown as an “Expense” line in the opening trial balance—its effect is already included in the –$2,800.

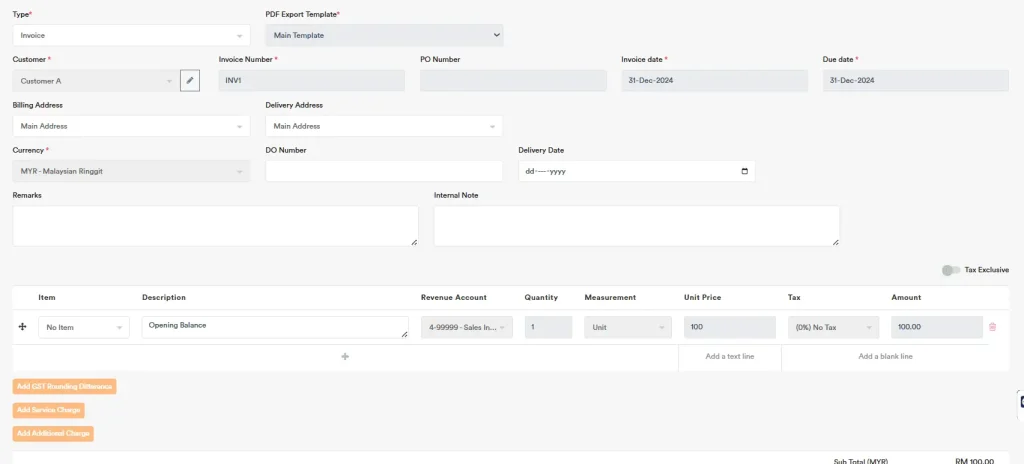

Opening Balance Recording (Account Receivables (Sales Module))

Sales (AR): bring in opening receivables with invoice details (unpaid)

Scenario / Dates

Opening balance date: 1 Jan 2025

Customer: ABC Pte Ltd

Invoice no.: INV-1001

Invoice date: 15 Dec 2024

Due date: 14 Jan 2025

Amount: $1,000 (no tax in this simple example)

Steps – Create the historical invoice (don’t mark as paid)

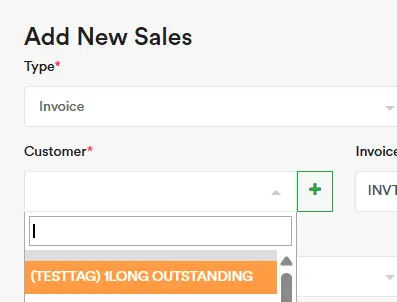

Go to ‘All Sales’ → ‘Add New Sale’

Enter the invoice with its original invoice date (15 Dec 2024), due date, invoice no., customer name, item/description, and amount $1,000. Click ‘Submit’

This preserves the correct ageing and keeps Account Receivables (AR) outstanding at opening.

What accounting entry this creates (on 15 Dec 2024)

Dr Trade Receivables $1,000

Cr Sales Revenue $1,000

Why this won’t inflate the new year’s revenue

Because the invoice is dated before your opening balance date (15 Dec 2024), the revenue sits in the prior year and gets closed into Retained Earnings at 31 Dec 2024.

On 1 Jan 2025, you start with the receivable outstanding, but no new revenue in the current year.

How your opening trial balance looks (as at 1 Jan 2025)

Trade Receivables +$1,000 (debit)

Retained Earnings –$1,000 (credit)

(That’s the balancing figure: Debits $1,000 = Credits $1,000.)

When the customer pays (in 2025)

Dr Bank $1,000

Cr Trade Receivables $1,000

That clears the outstanding receivable with no impact on prior-year revenue.

Opening Balance Recording (Account Payables (Expenses Module))

Expenses (AP): bring in opening payables with bill details (unpaid)

Scenario / Dates

Opening balance date: 1 Jan 2025

Supplier: XYZ Supplies Pte Ltd

Bill no.: BILL-2001

Bill date: 20 Dec 2024

Due date: 20 Jan 2025

Amount: $800 (no tax in this simple example)

Steps – Create the historical bill (don’t mark as paid)

Go to ‘All Expenses’ → ‘Add New Expense’

Enter the original bill date (20 Dec 2024), due date, bill no., supplier name, item/description, and amount $800. Click Submit

This preserves correct ageing and keeps AP outstanding at opening.

What accounting entry this creates (on 20 Dec 2024)

Dr Expense $800

Cr Trade Payables $800

Why this won’t inflate the new year’s expenses

The bill is dated before your opening balance date (20 Dec 2024).

That expense belongs to the prior year and is closed into Retained Earnings at 31 Dec 2024.

On 1 Jan 2025, you start with the payable outstanding, but no new expense in the current year from this bill.

Opening trial balance (as at 1 Jan 2025)

Trade Payables –$800 (credit)

Retained Earnings +$800 (debit)

(Debits = Credits: $800 = $800.)

When you pay the supplier (in 2025)

Dr Trade Payables $800

Cr Bank $800

That clears the payable; no impact on current-year expense from this historical bill.

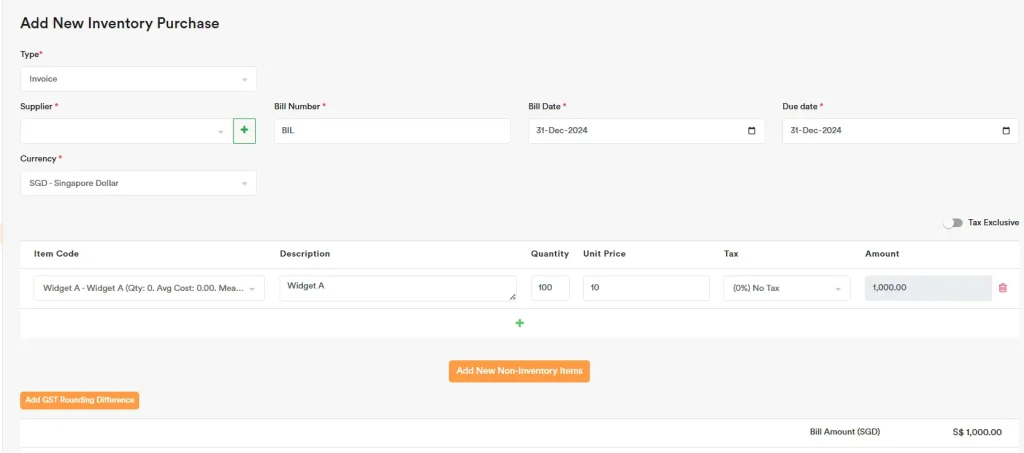

Opening Balance Recording (Inventory Module – perpetual method)

Inventory (Opening Stock): one clean way to bring it in

Goal: Show the remaining stock on hand at the start of your new year without messing up current-year P&L.

Key dates & names

Opening balance date: 1 Jan 2025

Transaction you’ll enter: a single purchase bill dated 31 Dec 2024

Supplier: “Opening Balance Supplier” (a dummy supplier you create for this purpose)

Example numbers

Item: Widget A

Quantity: 100 units

Unit cost: $10

Total cost: $1,000 (no tax in this base example)

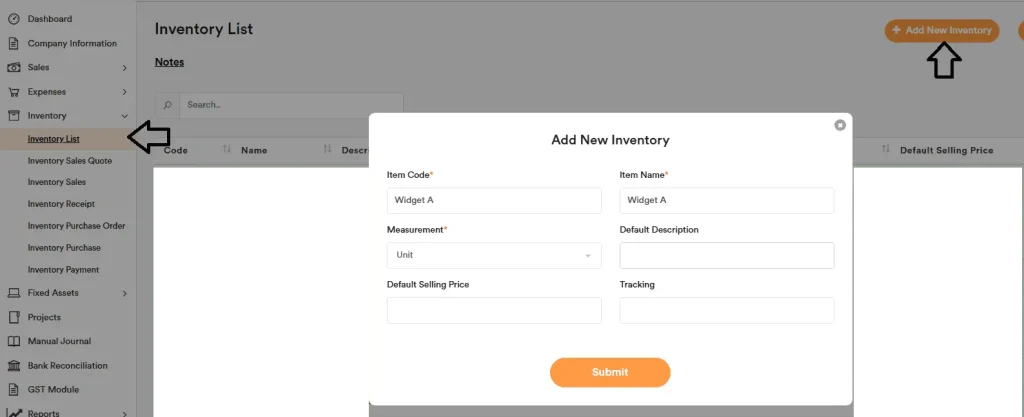

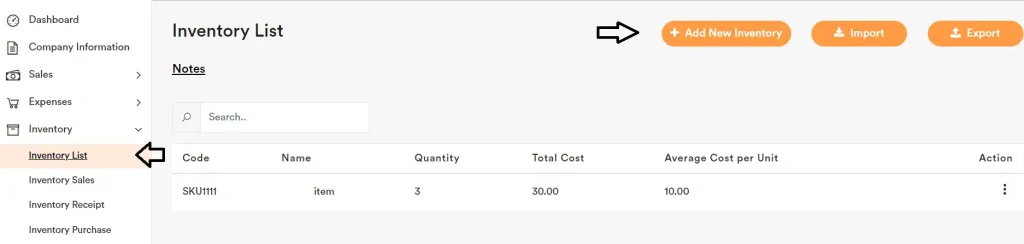

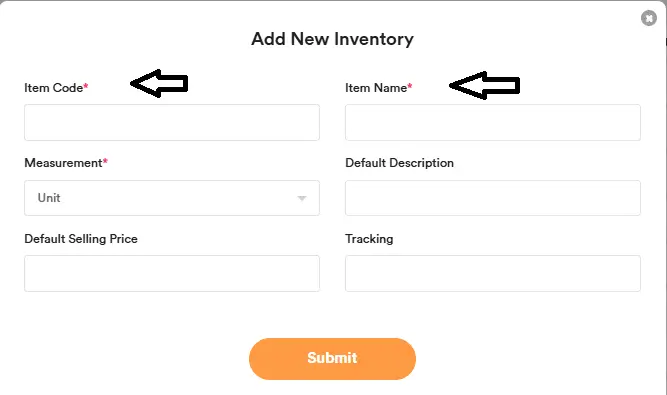

Step 1 – Go to ‘Inventory List’ → ‘Add New Inventory’

Add your items (or click Import to upload a list). The items you create here will be available to select when you enter inventory purchase later.

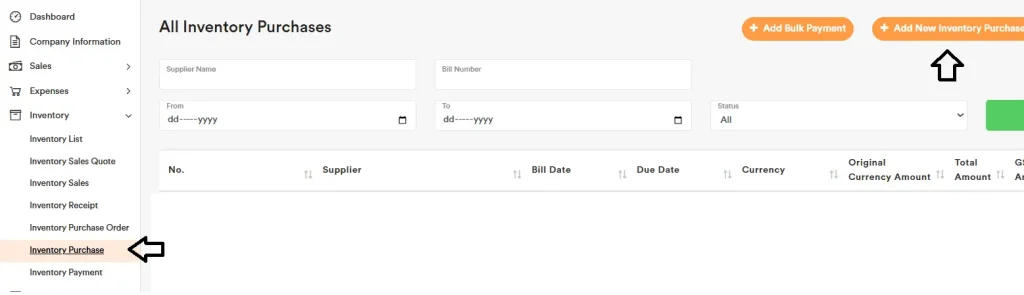

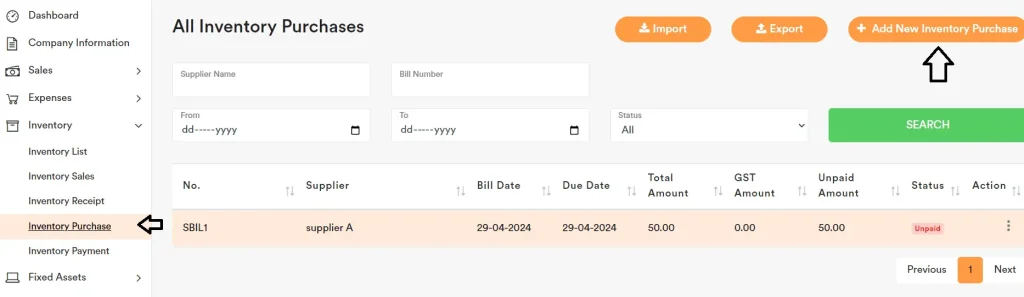

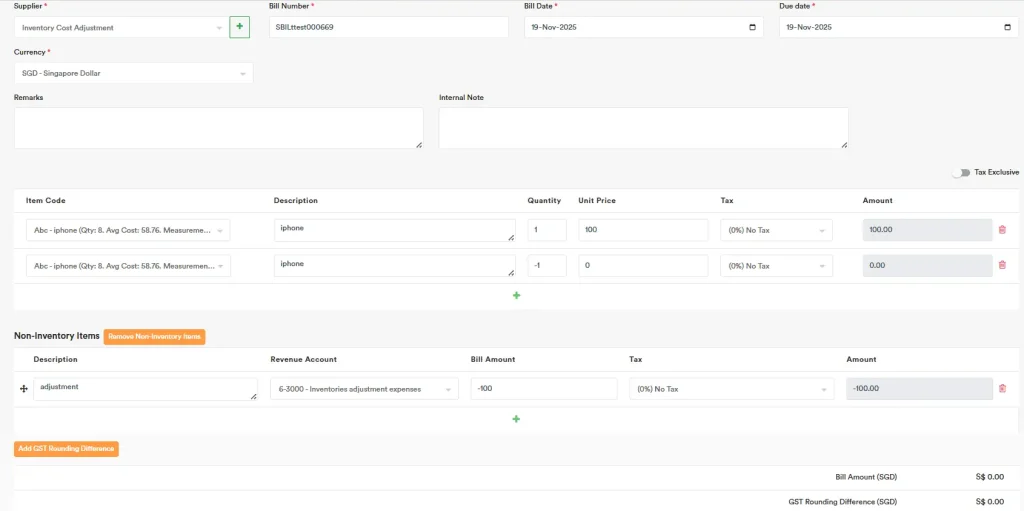

Step 2 – Enter one historical bill for the remaining stock (31 Dec 2024)

Go to Inventory Purchase → Add New Inventory Purchase

Supplier: Opening Balance Supplier

Bill date: 31 Dec 2024

Line: Widget A, Qty 100, Unit cost $10 → $1,000

What it posts (perpetual inventory):

Dr Inventory $1,000

Cr Trade Payables $1,000

Why 31 Dec 2024? This keeps the purchase in last year, so you start 1 Jan 2025 with stock on the balance sheet (no new expense in the current year).

Step 3 – Choose how to “pay” that bill (two options)

Option A — Pay from Bank on 31 Dec 2024 (your original flow)

Record a payment on 31 Dec 2024:

Dr Trade Payables $1,000

Cr Bank $1,000

Opening (1 Jan 2025):

Inventory +$1,000

Bank is $1,000 lower (because you just recorded that prior-year payment)

Final alignment (same day, 1 Jan 2025):

Compare your ledger’s Bank to the actual closing bank (per statement at 31 Dec 2024).

If your ledger Bank is short by $1,000 (example: ledger shows $1,000; statement says $2,000), post one opening journal to align:

Dr Bank $1,000

Cr Retained Earnings $1,000

Now your opening balance sheet tallies.

Option B — Use an Opening Balance Clearing (contra/suspense) account

To avoid touching Bank before you finalise, mark the bill Paid on 31 Dec 2024 to the Clearing account instead of Bank:

Dr Trade Payables $1,000

Cr Opening Balance Clearing $1,000 (Newly created bank type account)

Opening (1 Jan 2025):

Inventory +$1,000

Opening Balance Clearing –$1,000 (credit)

Bank unchanged (you’ll set Bank to the actual opening per statement)

Final alignment (1 Jan 2025):

Once you confirm all real opening balances, clear the suspense to equity with one entry:

Dr Opening Balance Clearing $1,000

Cr Retained Earnings $1,000

The result is the same clean opening as Option A, but you never touched the Bank during setup.

Step 4 – How this affects opening Retained Earnings

On opening day (1 Jan 2025), P&L accounts are zeroed (they closed into Retained Earnings at 31 Dec 2024). Your Retained Earnings (opening) is simply the balancing figure so that:

Retained Earnings = Total Assets – Total Liabilities – Share Capital – Other Reserves

In Option A, you may need a Bank ↔ Retained Earnings top-up entry so Bank matches your statement.

In Option B, you’ll clear Opening Balance Clearing ↔ Retained Earnings to finish the balancing.

Final Tips

If you have many SKUs, put all opening quantities on one bill (multiple lines), dated 31 Dec 2024, to “seed” on-hand stock.

Keep supporting docs (stock count sheets, valuation method notes like FIFO/Weighted Avg) for your audit trail.

Opening Balance Recording (Inventory Module – periodic method)

If you use periodic inventory, bring in opening stock with one manual journal—no need to enter items one by one or create a supplier bill. Date it 31 Dec 2024:

Dr Inventory (Opening Stock) $X

Cr Opening Balance Equity / Retained Earnings $X

Fuller tip (Periodic inventory)

Using periodic inventory? Record the total opening stock with a single manual journal (no purchase bills per SKU required). First total up your closing stock value as at 31 Dec 2024 (qty × cost, per your count/valuation). Then post:

Dr Inventory (Opening Stock) $X

Cr Opening Balance Equity / Retained Earnings $X

If you prefer, credit an Opening Balance Clearing account and later clear it to Retained Earnings when you finalise all opening balances.

For step-by-step workflows on inventory recording, refer to Inventory Recording.

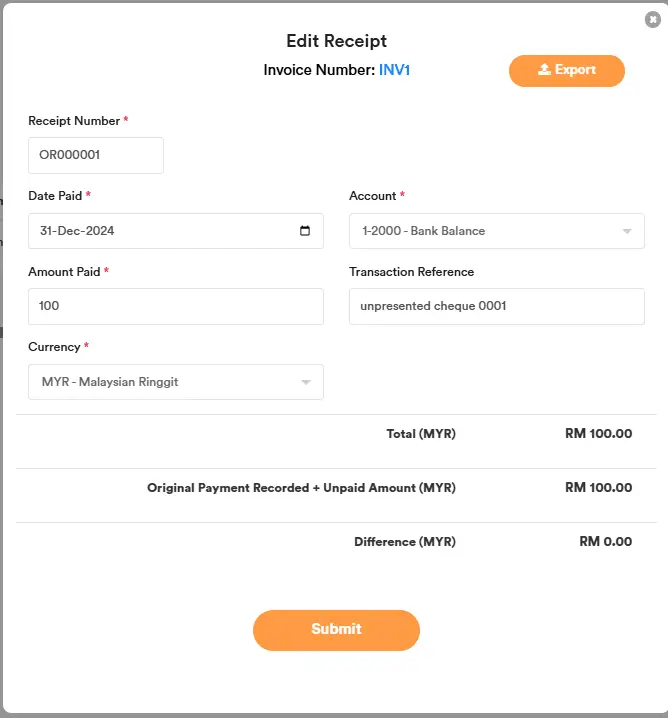

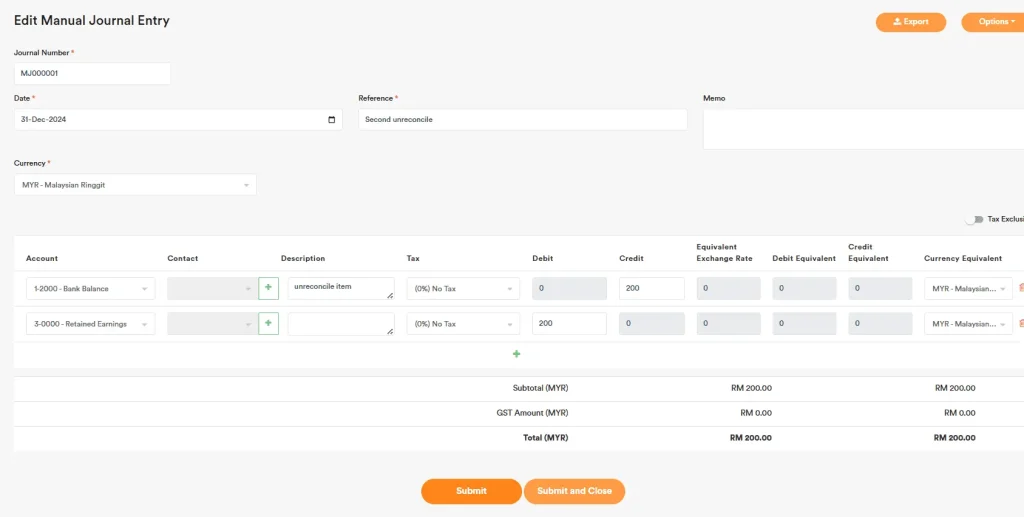

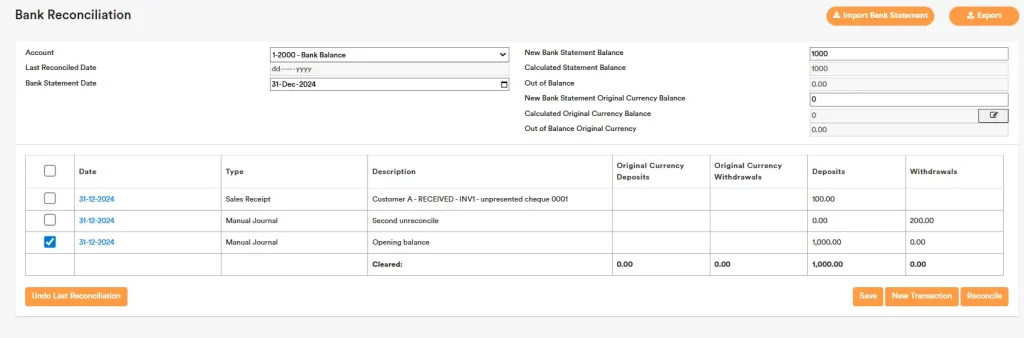

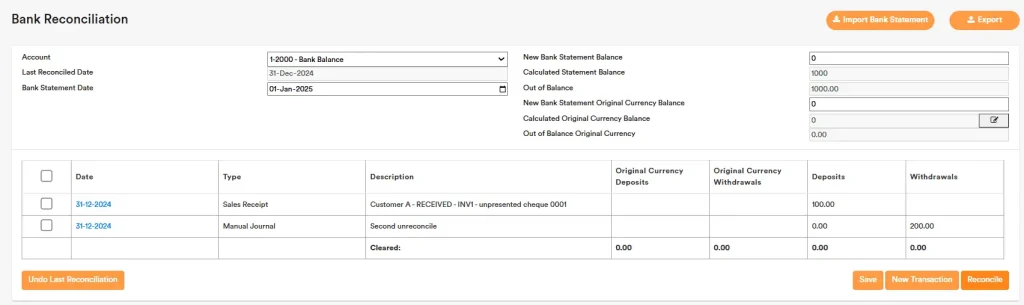

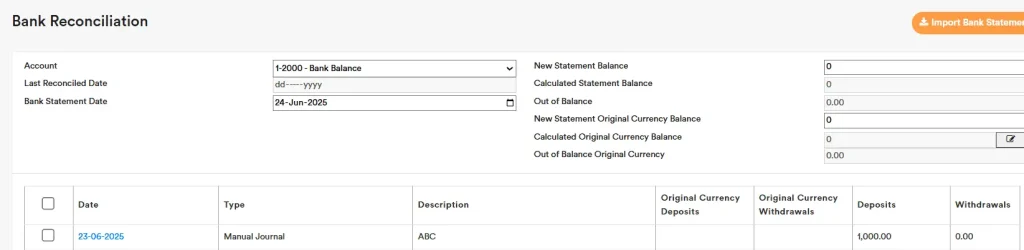

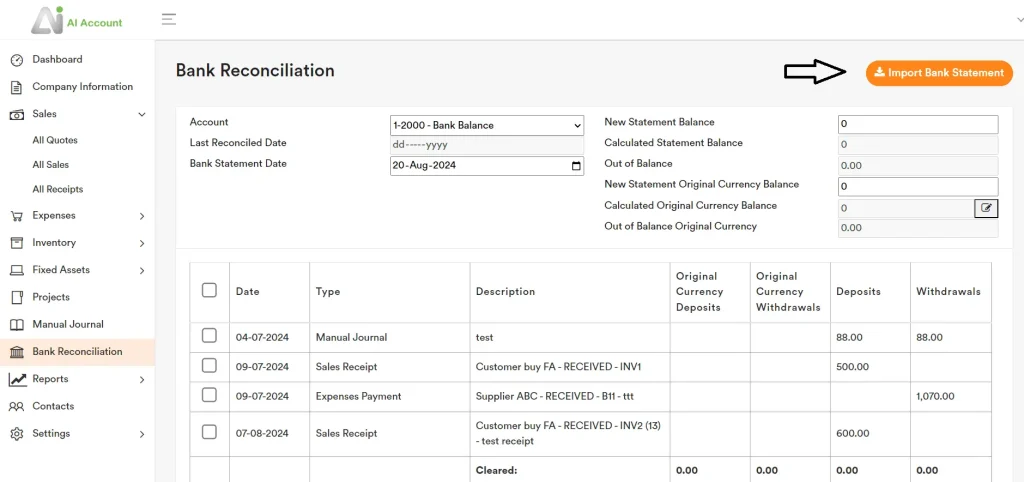

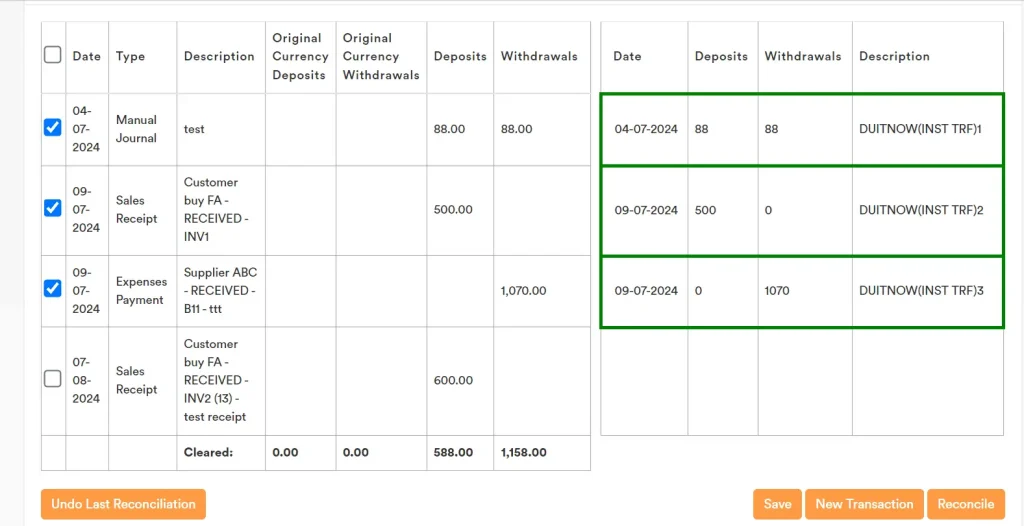

Opening Balance Recording (Bank Reconciliation)

You may have unreconciled items carried forward from the previous month’s bank reconciliation. You can record them as usual sales and receipts transactions, or via manual journal entries.

For example, I record the sales and receipt entries for the unreconciled item (an unpresented cheque).

Next sample, post another manual journal entry for the second unreconciled item.

Then, post a manual journal entry for the opening balance (excluding the unreconciled items).

After that, go to Bank Reconciliation and perform the reconciliation as at 31 December 2024. Assuming the two unreconciled items remain outstanding, the bank statement balance should be 1,000.

Once you click Reconcile, leave the unreconciled items to be carried forward and cleared in the subsequent period.

Opening Balance Recording (Retained Earnings)

Final step: set the true opening Retained Earnings so the balance sheet balances

After you’ve re-created all historical items (e.g., unpaid invoices/bills, prior-year payments/receipts, manual depreciation dated before the opening date), you must net everything off and bring Retained Earnings to the correct opening figure. This is normal and ensures the balance sheet balances on 1 Jan 2025.

What to do:

Step 1 – Confirm your true opening balances from your prior-year trial balance and statements (as at 31 Dec 2024):

Bank closing balance

Trade Receivables (outstanding invoices)

Trade Payables (outstanding bills)

Fixed assets and accumulated depreciation

Any other assets/liabilities (tax, loans, etc.)

Share capital (if any)

Step 2 – Compare vs what’s now in your ledger after you re-entered the history.

If Bank (or any other balance) doesn’t match the true opening, plan a single opening-date journal to fix it.

Step 3 – Post one balancing journal on 31 December 2024 to set Retained Earnings to the required amount.

If you need to increase Bank to the true opening:

Dr Bank / Cr Retained Earnings (for the difference)

If you need to reduce Bank to the true opening:

Dr Retained Earnings / Cr Bank (for the difference)

Retained Earnings is the balancing figure after all prior-year revenue/expense effects have closed out. In short:

Retained Earnings (opening) = Total Assets – Total Liabilities – Share Capital – Other Reserves (credits shown as negative if you use that sign style).

Migration Tool

Access the tool: https://convert.aiaccount.com/migration/

What it does

Converts accounting data from another system into AI Account import files — chart of accounts, contacts, opening balances, and historical transactions. The tool walks you through the process and tells you what to do at each step.

Privacy: The tool runs entirely in your browser. Your data is never uploaded to any server.

Two migration modes

Full Migration — Brings the complete transactional history into AI Account. Use when the client needs searchable historical records.

Opening Balance Only — Brings only closing balances and outstanding AR/AP into AI Account as the starting position. Faster, simpler, and sufficient for most fresh-year migrations.

You choose the mode in Step 1. Discuss with your client what level of history they need.

Before you start

You need three things:

- A modern web browser (Chrome)

- Exports from the source accounting system — the tool tells you exactly which files after you pick the software in Step 1

- AI Account’s Chart of Accounts template

How the wizard works

The tool has 8 steps. You can move forward and back at any time. Your work auto-saves in the browser so you can save and resume sessions.

- Step 1 — Setup: pick source software, migration mode, and company country

- Step 2 — Files: upload the files the tool lists for your selection

- Step 3 — Columns: confirm the auto-detected column mapping

- Step 4 — Accounts: match source accounts to AI Account chart

- Step 5 — Transactions: confirm how source transaction types map to AI Account templates

- Step 6 — Review: resolve any warnings before downloading

- Step 7 — Download: get the Excel files ready for import

- Step 8 — Validate: After the import, generate the report from AI Account to validate that the import is in good order.

The tool explains each step on-screen as you reach it.

How account matching works (Step 4)

The tool tries to auto-match source accounts to AI Account using four tiers, in order:

- Exact name match

- Software-specific aliases (terminology unique to your source system)

- Generic accounting aliases (e.g. “Sales” / “Revenue” / “Turnover” all map to the same target account)

- Fuzzy name similarity (handles typos and word-order differences)

You can always override any suggestion. For unmatched accounts, either pick one from the dropdown, click “Create new” for a single account, or use “Auto-create new for unmapped” to bulk-propose new accounts.

How Opening Balance mode works

Instead of replaying transactions, the tool generates:

- A balanced Opening Manual Journal setting account opening positions from the source Balance Sheet

- Opening Sales Invoices for outstanding customer balances from the Aged Receivables Detail

- Opening Bills for outstanding supplier balances from the Aged Payables Detail

The opening invoices and bills appear in AI Account’s standard AR/AP aging reports as normal documents, so collection and payment workflows work immediately.

For Full Migration, the tool check that:

- Trial Balance in AI Account matches the Trial Balance in the source system at migration date

- Total AR in AI Account matches total AR in the source system

- Total AP in AI Account matches total AP in the source system

- Bank balances in AI Account match bank balances in the source system

- Transaction counts per account match expectations

For Opening Balance Only, check that:

- Each account’s opening balance in AI Account matches the closing balance in the source Balance Sheet

- Total opening AR in AI Account matches total outstanding in the source Aged Receivables

- Total opening AP in AI Account matches total outstanding in the source Aged Payables

- Contact list is complete

If anything doesn’t tally, check Step 6 in the tool for warnings you may have skipped, re-export the source files without filters, or contact us with the specific reconciliation difference.

Important notes

- Data privacy: Files never leave your computer. Keep your own backups — nothing is stored on our end.

- Session persistence: Your progress can be saved and resumed after.

- Shared computers: Click “Reset” before leaving the device.

- One client at a time: Complete one migration end to end before starting another.

Need help?

Contact: info@aiaccount.com

For requests to add new source accounting software, tell us which system and we will work on it.

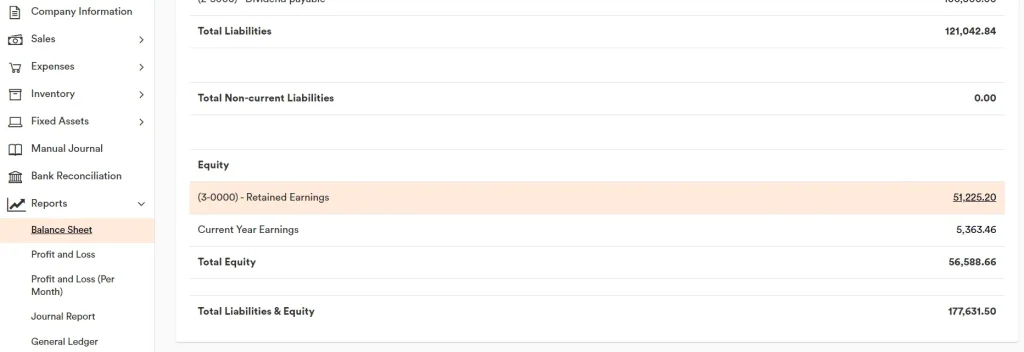

Retained Earnings

(3-0000) Retained Earnings are generated based on the period you select in Financial Settings (Incorporation Date), Balance Sheet Start Date and End Date by default.

You can select the period you want to generate a prior year balance sheet or previous month balance sheet. Example, if your company year end is 31 Dec 2022, you can generate the previous year balance sheet by indicating the start date as 1 Jan 2021 and End date is 31 Dec 2021.

Example, if you select Balance Sheet Start Date and End Date, start from 1 Jan 2022 to 31 Aug 2022, then the Balance Sheet “Current Year Earnings” will be for the period from (Start Date) 1 Jan 2022 to (End Date) 31 Aug 2022, “(3-0000) Retained Earnings” in Balance Sheet will be cover the period “Incorporation Date” to Balance Sheet one day before the “Start Date”.

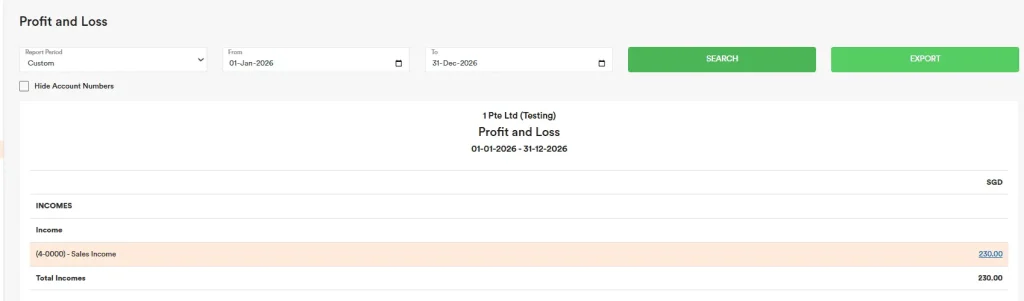

When you click on the “Current Year Earnings”, it will show the relevant profit and loss period that can match the number.

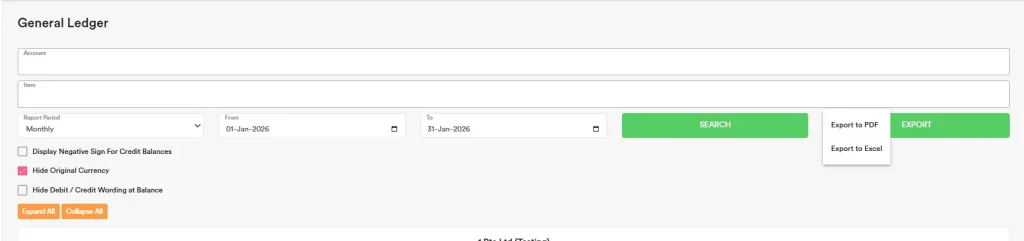

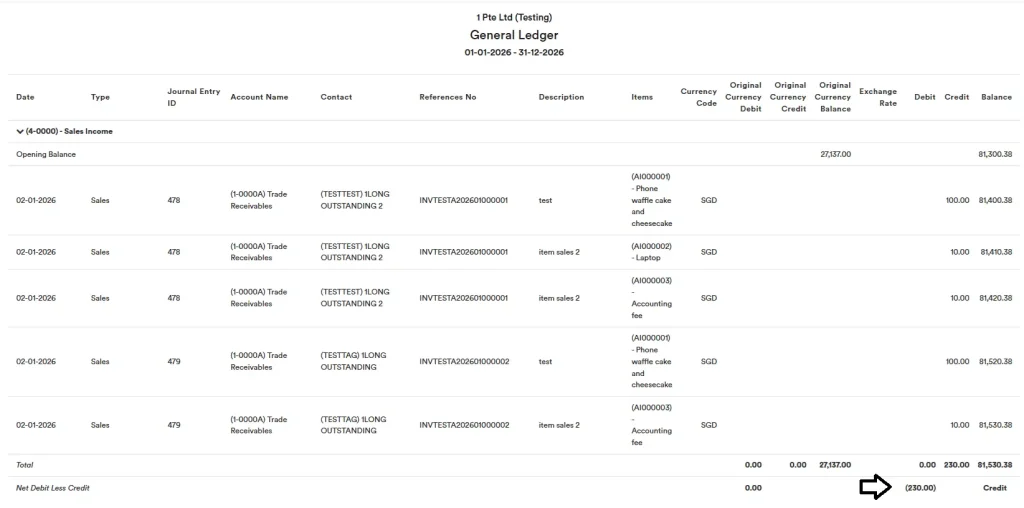

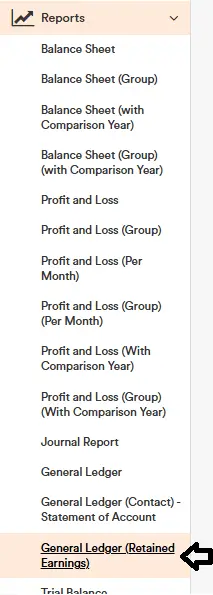

When you click on the “(3-0000) Retained Earnings”, it will show the “General Ledgers (Retained Earnings)” report that can match the number.

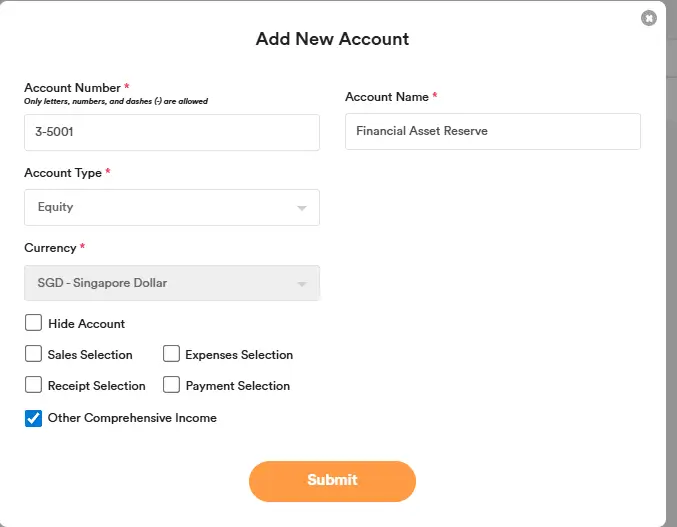

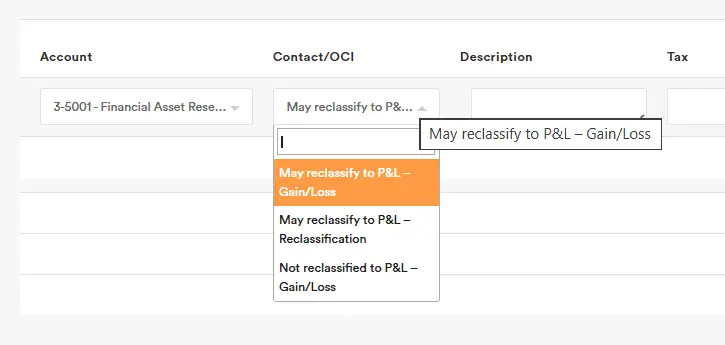

Other Comprehensive Income

You can now mark certain Equity accounts as ‘Other Comprehensive Income’ (OCI), so they can be used correctly in Manual Journals only and shown in a dedicated OCI report.

Important rules

- You can only tick OCI when creating a new account.

- Once ticked and saved, the OCI checkbox becomes locked.

- You cannot change the OCI tick later.

When you select an OCI account in Manual Journal, the Contact / OCI column will show a dropdown with these options:

- May reclassify to P&L – Gain/Loss

- May reclassify to P&L – Reclassification

- Not reclassified to P&L – Gain/Loss

OCI entries will appear in the General Ledger, and a summary will be shown in the Other Comprehensive Income Report.

Import of Data

Our software supports data import for the following items using import templates:

- Contacts Import Template

- Sales Invoice Import Template

- Sales Receipt Import Template

- Expenses Bill Import Template

- Expenses Payment Import Template

- Inventory List Template

- Inventory Sales Invoice Import Template

- Inventory Receipt Import Template

- Inventory Purchase Bill Import Template

- Inventory Payment Import Template

- Fixed Assets Import Template

- Manual Journal Import Template

You can use these templates to import historical data from your previous accounting software, ERP system, or POS system. They are also suitable for importing the latest data or for day-to-day data entry — saving you time and eliminating the need to key in data manually one by one.

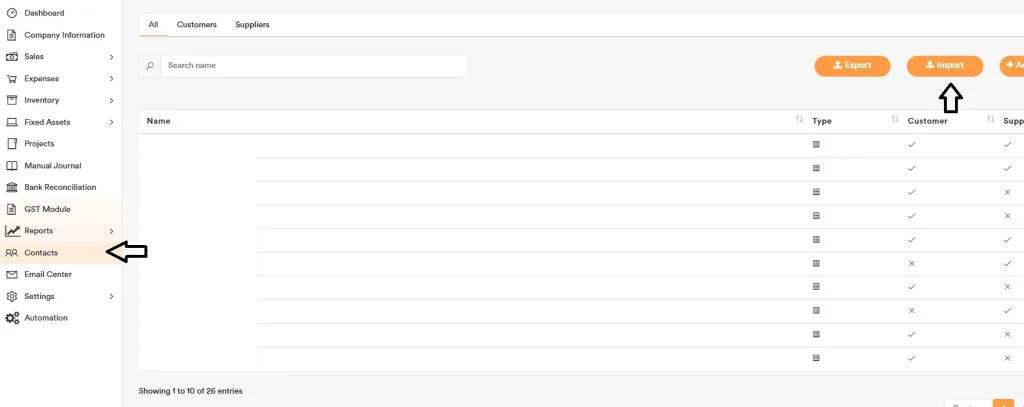

Import of Contacts

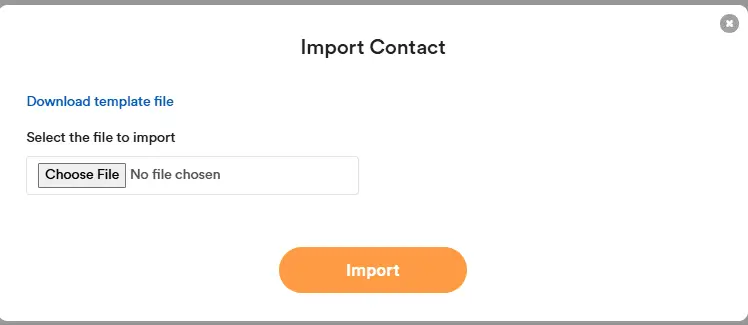

Go to Contacts and click the Import button in the top-right corner.

Download the Template File, prepare the data, then upload and import it.

To update existing contacts, click the Export button to download the contacts in Excel format.

Fill in or update the necessary details in the Excel file.

Use the Import button again to upload the updated Excel file. The changes will be reflected in the AI Account software.

Import of Sales and Expenses transactions

When importing sales and expenses transactions, if the customer or supplier contact is not available, it will be automatically created based on the name input from your Excel import into the system.

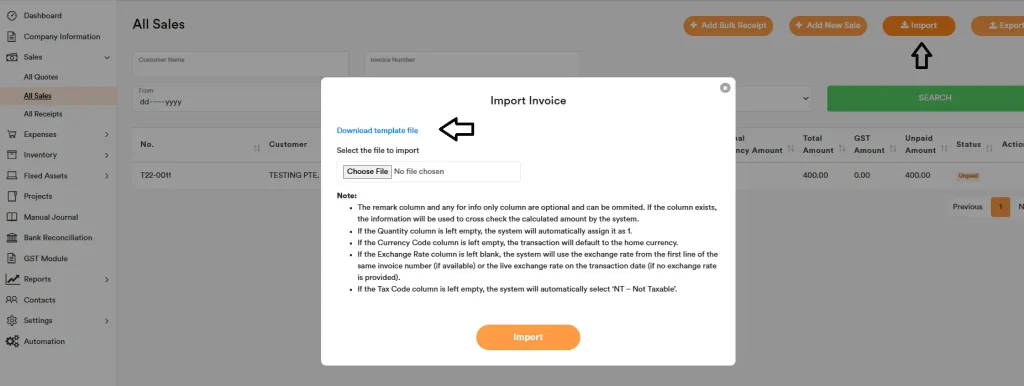

For sales, you may optionally import the Remark column. In each import of sales or inventory sales transaction, the remark can only be entered on the first line of the invoice. Multiple remarks across different lines are not allowed, as each invoice supports only one remark field.

In the import template, any column labeled “For info only” is optional and can be omitted. If such a column is included, the information will be used to cross-check the system’s calculated amount during import.

Example: Importing Sales.

Go to ‘All Sales’, click ‘Import’, then click ‘Download template file’ to get the CSV template. Open the CSV and fill in the required details, then save it. Back in the software, click ‘Choose File’ to select your completed CSV and click ‘Import’. All valid sales will be imported. If any required fields are missing or invalid, a warning box will list what to fix. If you’re unsure, email us at info@aiaccount.com for assistance.

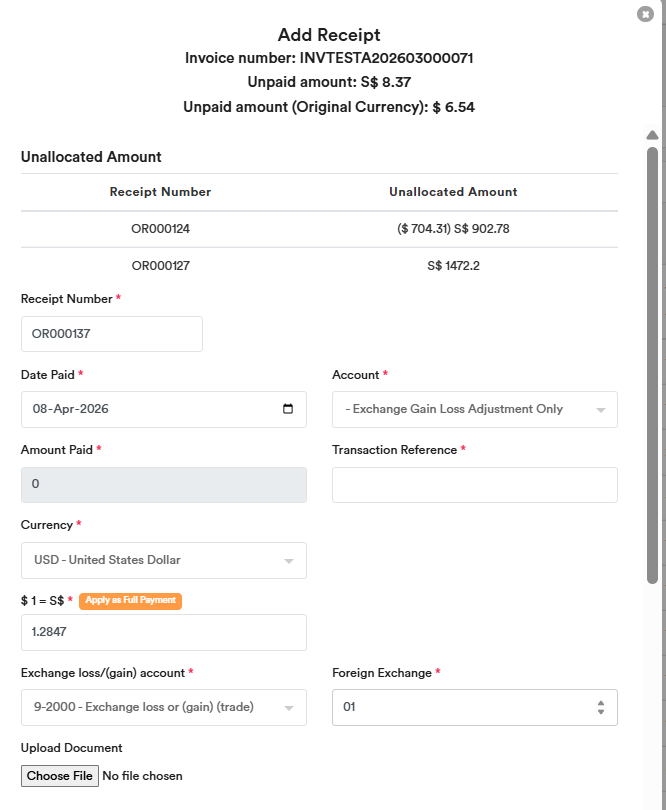

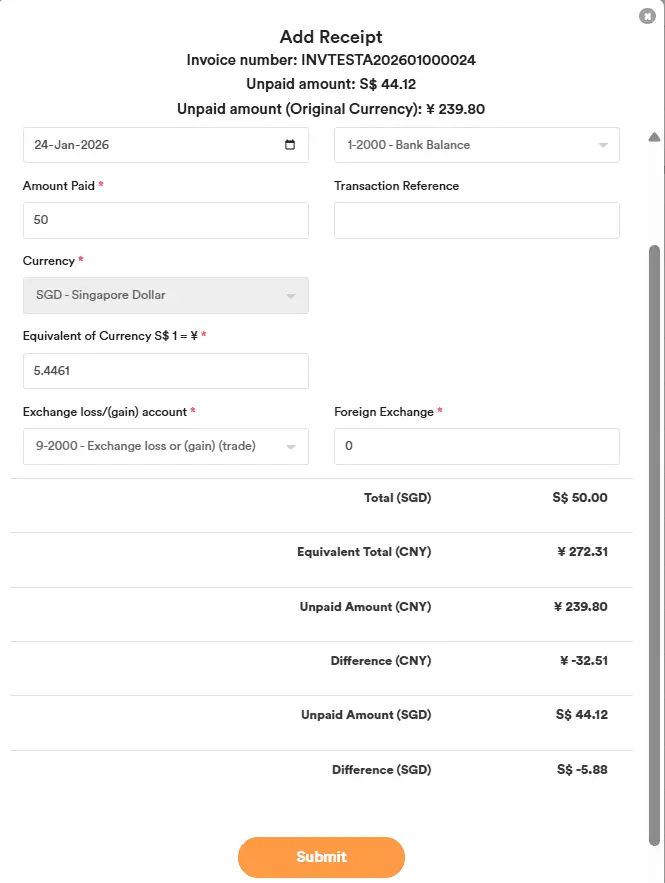

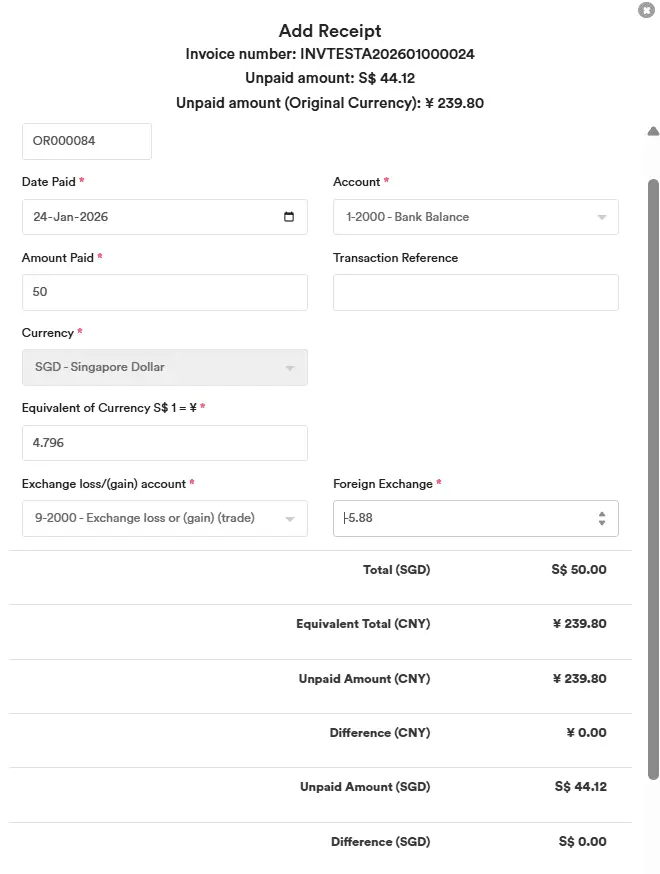

Import of Transactions in Foreign Currency

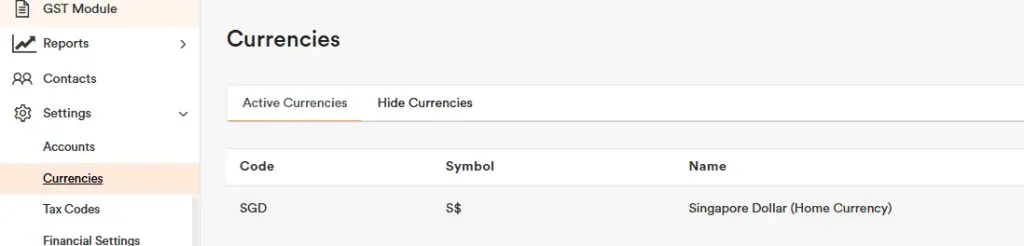

You can enter the Currency Code in the import template if you wish to import transactions in a foreign currency.

To find the correct Currency Code, please refer to the “Currencies” section at Settings.

If the Currency Code column is left blank, the transaction will default to the home currency. If you select the home currency as the Currency Code, the exchange rate will automatically be set to 1 in the system.

If the Exchange Rate column is left blank, the system will use the exchange rate from the first line of the same invoice number (if available) or the live exchange rate on the transaction date (if no exchange rate is provided).

When invoicing and recording payment in the same foreign currency, the system will automatically calculate the exchange gain or loss. Any difference between the exchange rate at the time of invoicing and at the time of payment will be posted as a foreign exchange gain or loss.

If you make a local currency payment and the amount exceeds the foreign currency invoice (after conversion), the difference will be posted as an exchange gain or loss. If the payment is less than the converted invoice amount, it will be recorded as a partial payment of the invoice.

Import of Inventory

When importing inventory items with different purchase costs, it is important to use separate item codes for each cost level. This is because the import process handles inventory by batch, and the system does not automatically adjust the cost of sales that occur between purchases.

For example, if you import Item A at $10 and later import the same Item A at $15 under the same item code, but sales take place in between those two imports, the system may not correctly calculate the average cost. The sales would have already reduced the earlier stock at $10, and adding new stock at $15 later will distort the average cost calculation. This leads to inaccurate cost of goods sold (COGS) and profit margins.

To avoid this issue, it is best to assign separate item codes for each different cost.

Alternatively, if you want to use the same item code, you must enter the transactions manually into the system in chronological order—ensuring that purchase and sales entries reflect the actual timeline. This approach helps maintain accurate inventory valuation and average cost calculation.

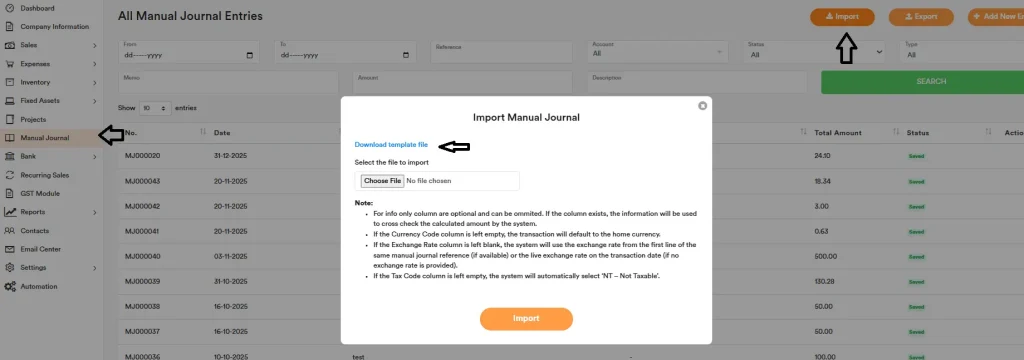

Import of Manual Journal

Click Import (top right).

Download the template file as shown in the screenshot.

Fill in the template using the guidelines below, then import it.

Column Guide

Account #

- Enter the chart of account number.

- You can use it with or without dashes (e.g. 10000 and 1-0000 are treated as the same account).

Contact

- Required only for accounts that need a contact, such as:

- Trade receivables / trade payables

- Other receivables / other payables

- Supplier deposits / customer deposits

- Enter the customer or supplier name. The system will match an existing contact or create a new one.

Manual Journal Date

- The date of the manual journal entry.

- For one journal, all related lines must have the same date so the system knows they belong to the same entry.

References

- A reference for the journal (e.g. “accounting 1”).

- For one journal, every line must have the same Reference.

- Unique references are required for each manual journal during import.

- You can use the same reference and differentiate each manual journal by assigning a unique Journal Number. Please remember that every line within the same manual journal entry must use the same Journal Number.

Memo

- Optional. Leave blank if you don’t need it.

- If you use a memo, every line belonging to the same journal must have the same Memo.

Currency Code

- Currency of the journal (e.g. SGD, USD).

- All lines for the same journal must have the same Currency Code.

Exchange Rate

- Exchange rate for the selected currency. You can leave this blank and the system will automatically use the exchange rate based on the transaction date.

- All lines for the same journal must use the same Exchange Rate.

Debit Amount (Original Currency)

- Debit amount before GST in the original currency.

Credit Amount (Original Currency)

- Credit amount before GST in the original currency.

Tax Code

- Select the tax code (e.g. NT).

- When a tax code is selected, the system uses it to calculate/check GST and totals.

GST Amount (for info only)

- GST amount based on the tax code.

- Used by the system to cross-check your tax selection and amounts.

Inc-Tax Amount (for info only)

- Amount including tax (original amount + GST).

- Also used for system validation.

Description (Optional)

- You can enter a different description for each line.

Journal Number (Optional)

- You can enter a Journal Number if you want. If you leave it blank, the system will automatically assign one based on the prefix number settings. Please remember that every line within the same manual journal entry must fill up with the same Journal Number.

Important: Debits and Credits Must Balance

Each manual journal entry must balance:

Total Debit = Total Credit (including tax).

Example:

Line 1: Debit 1,000 with tax code 7% → GST 70 → Inc-Tax 1,070

Line 2: Credit 1,070 with tax code NT (no tax)

This way, the journal balances: Total Debit = 1,000 + 70 (GST) = 1,070 Total Credit = 1,070

Automation for Data Importation

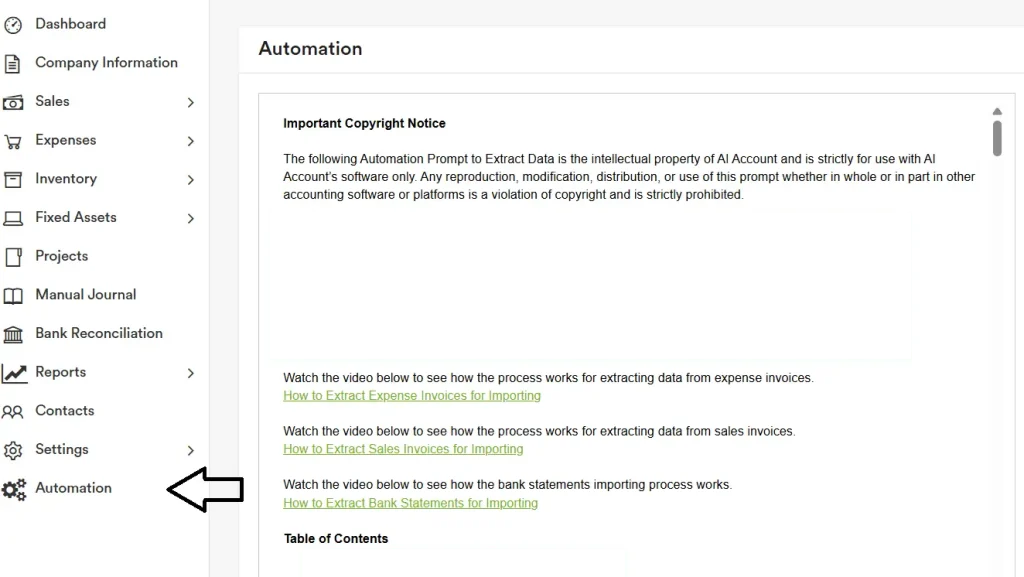

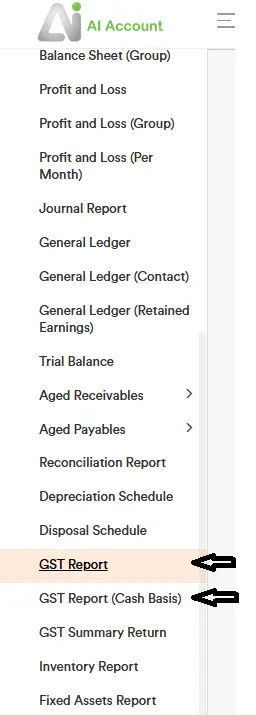

You can access the “Automation” section for step-by-step guides on how to automate key tasks, including scanning bank statements for automatic bank reconciliation, importing opening balances, and extracting sales and expense invoices from PDFs for seamless data import into our software.

Instructional videos are also available to demonstrate how the OCR and data import automation processes work.

Transaction Processing

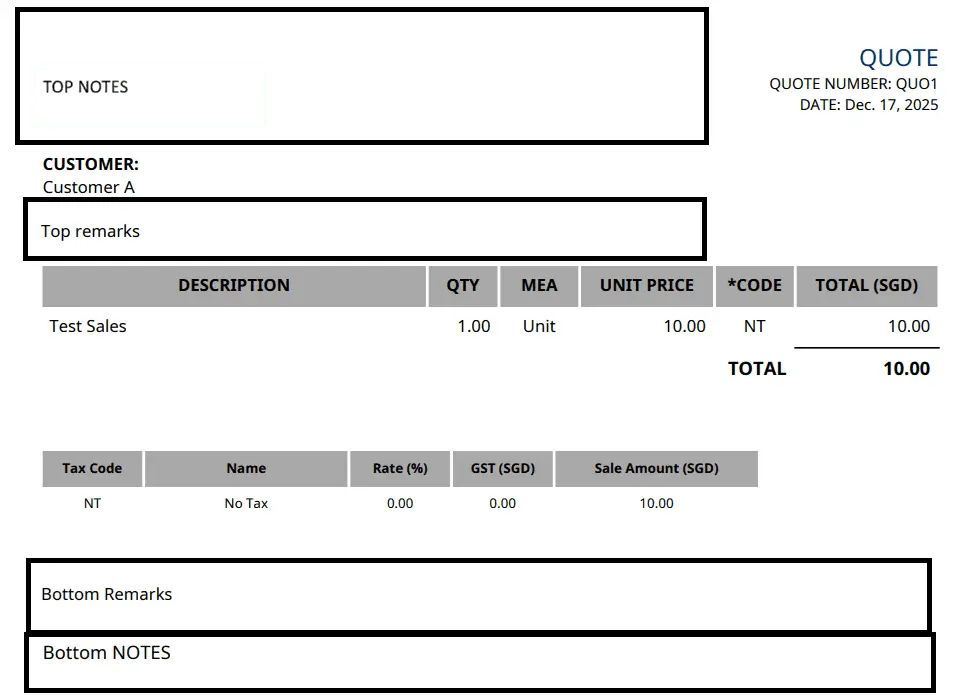

Sales Quotes

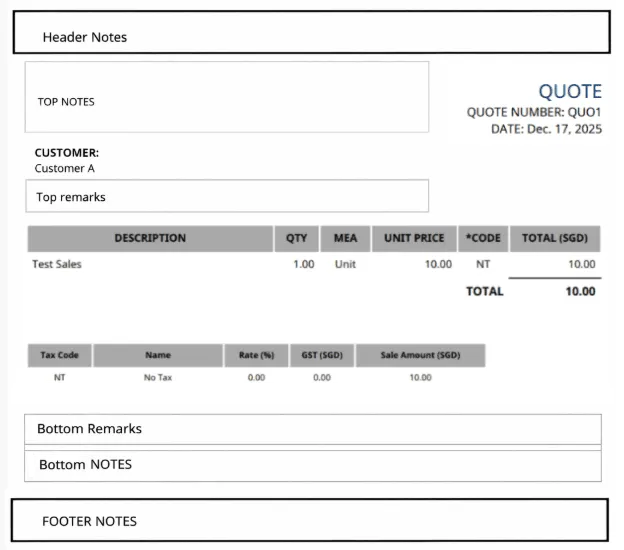

You can create Quotes (Quotations) for either normal sales or inventory sales, as shown in the extracted image below.

You can then convert a Quote into an actual sale by clicking the “Create Invoice” button within the respective Quote transaction.

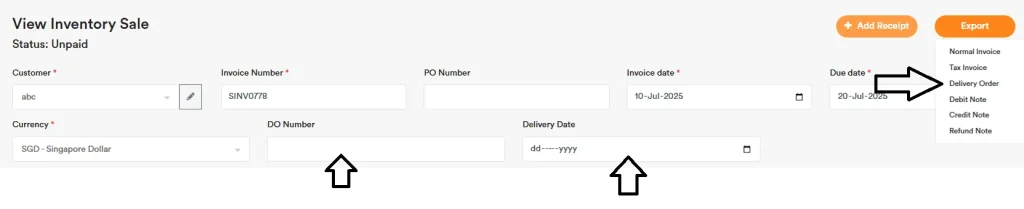

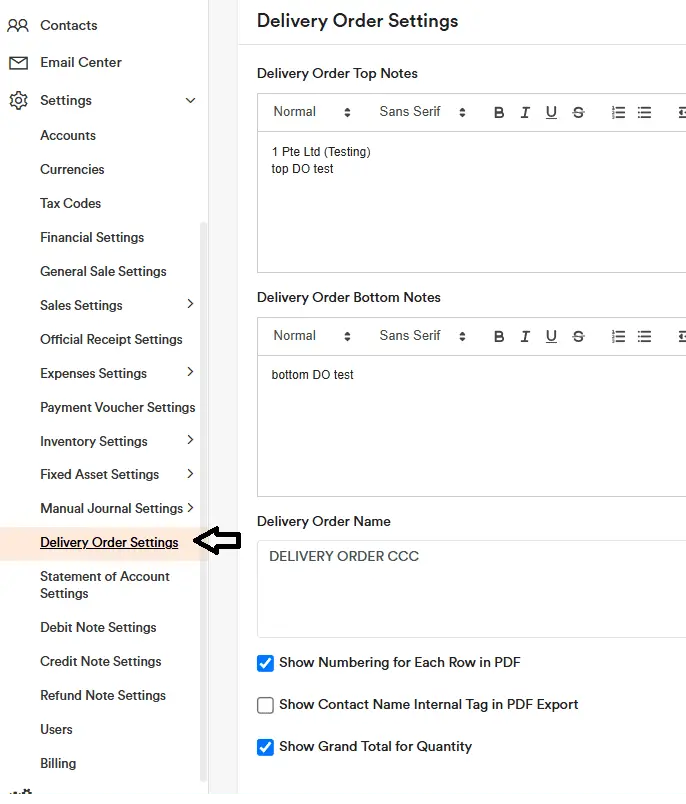

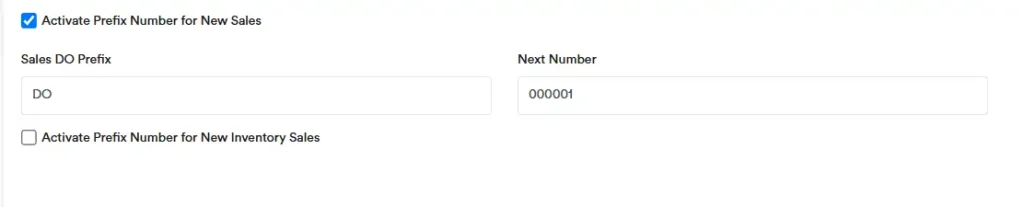

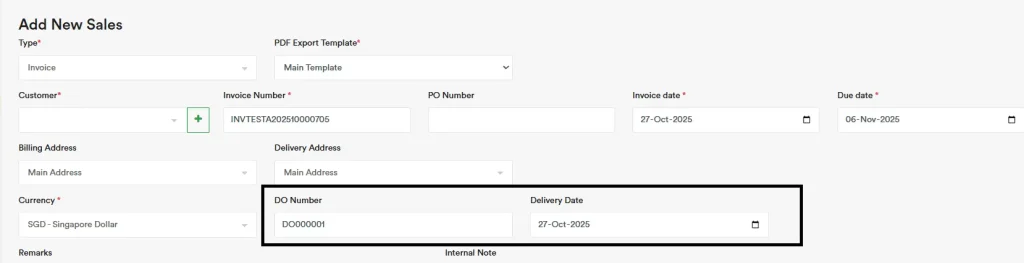

Delivery Order

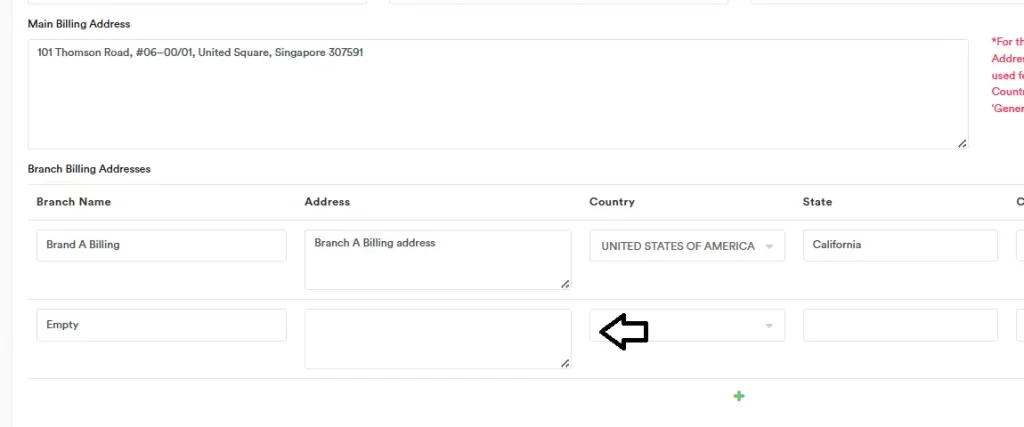

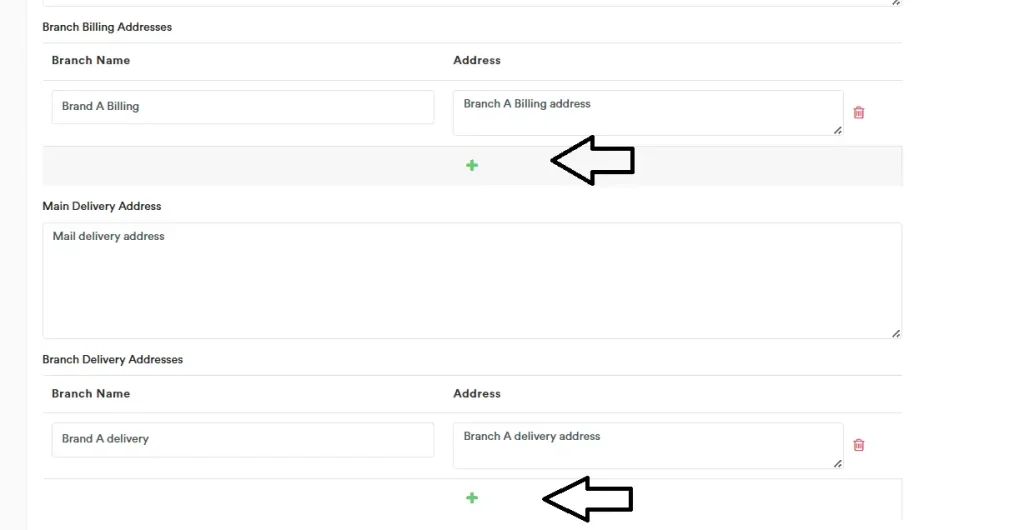

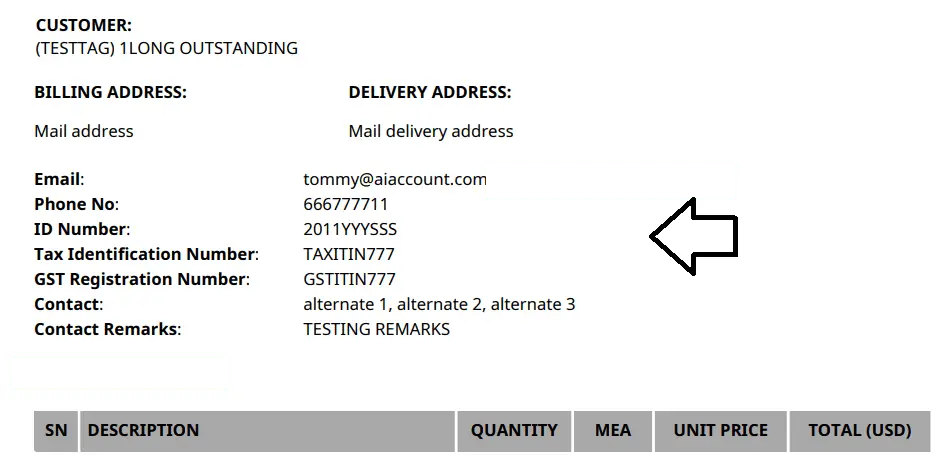

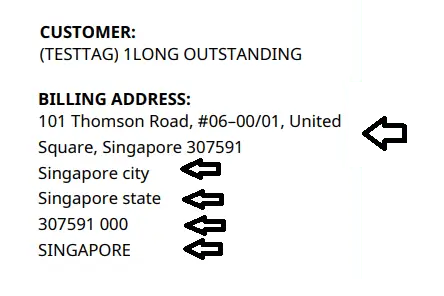

You need to fill in the delivery address under the contact details to display it on the Delivery Order when exporting the PDF. If your customer has multiple delivery addresses, you can create multiple branch addresses, as shown here.

You can generate a Delivery Order for the inventory sales you’ve made. Remember to fill in the DO Number and Delivery Date so that this information appears on the generated Delivery Order. You need to fill in the delivery address under the contact details to display it on the Delivery Order when exporting the PDF. If your customer has multiple delivery addresses, you can create multiple branch addresses, as shown here.

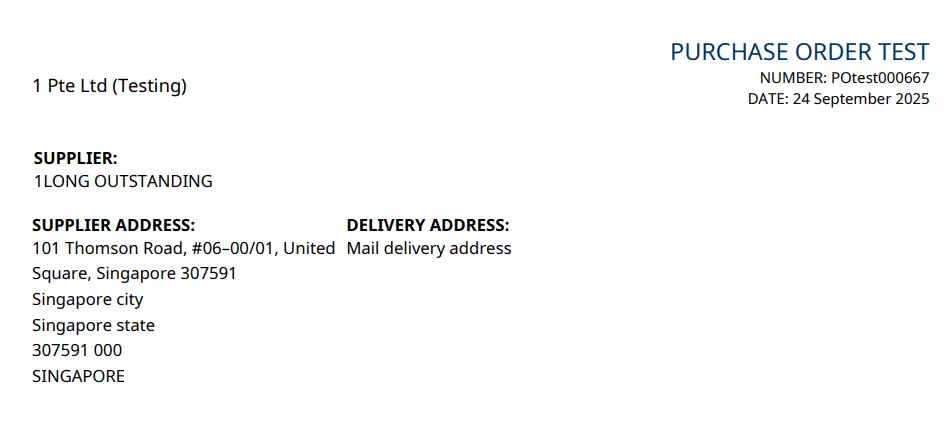

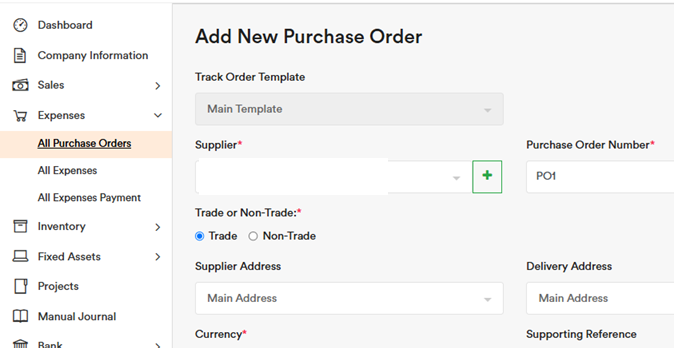

Purchase Order

You can create a Purchase Order for either normal expenses or inventory purchases, as shown in the extracted image below.

You can then convert a Purchase Order into an actual purchase by clicking the “Create Bill” button within the respective Purchase Order transaction.

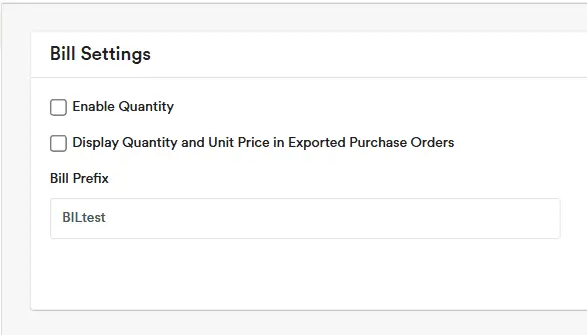

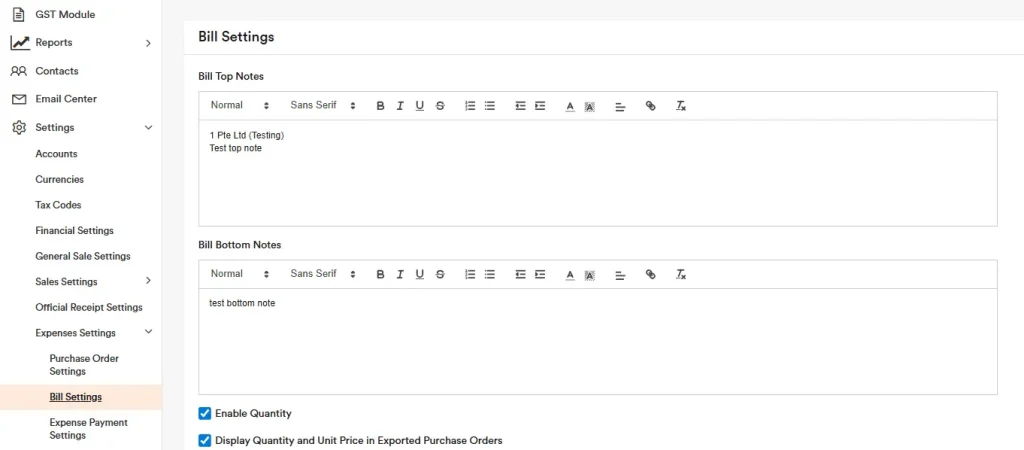

To include quantity in your exported purchase order, go to ‘Bill Settings’, tick “Display Quantity and Unit Price in Exported Purchase Orders” and click Save. The exported PDF reports for Purchase Order will then show the quantity and unit price.

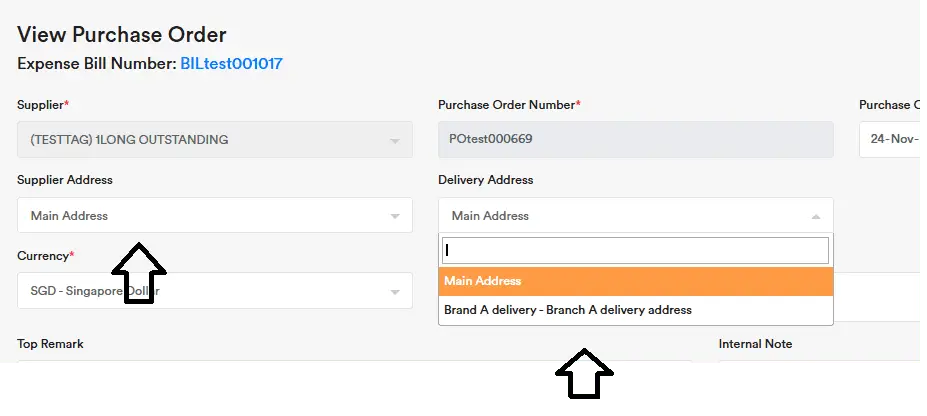

You can select the Address field in Contacts when creating your purchase order.

It will appear in the Purchase Order export as shown below.

If you don’t want to display the Supplier Address and only want to show the Delivery Address, go to the relevant contact and add an additional address entry and leave it blank like below. Then, select that address when creating the purchase order.

After that, the exported purchase order will show only the Delivery Address.

Sales Recording

You can go to All Quotes or All Sales to start creating your quotes and sales transactions with quantity.

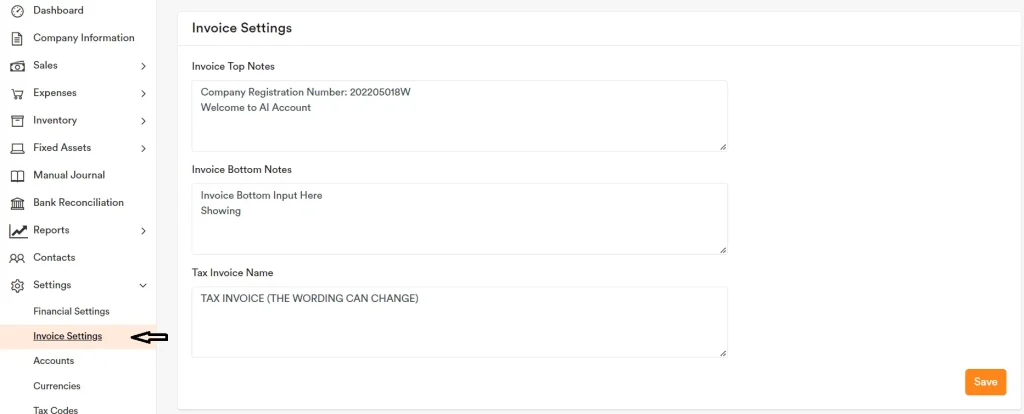

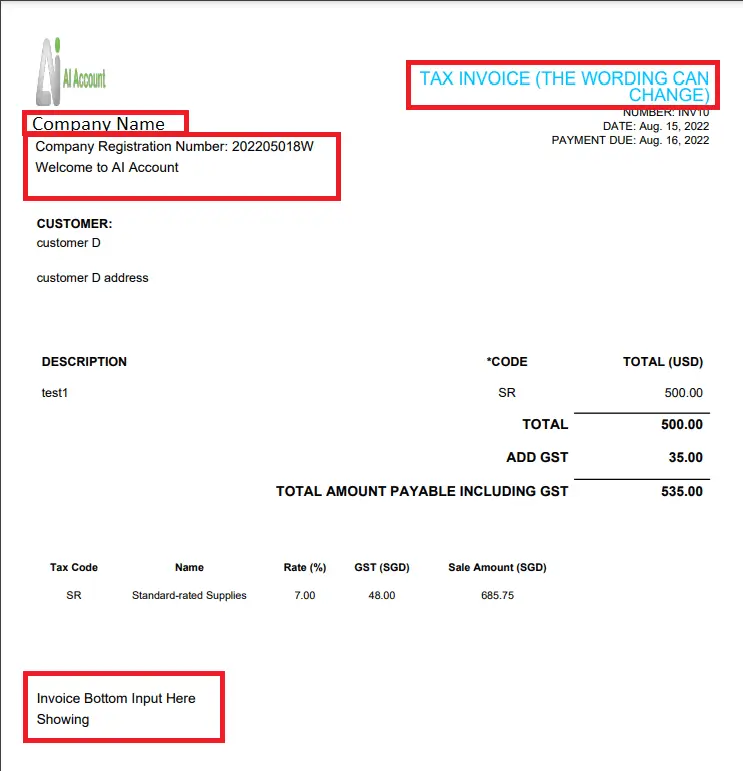

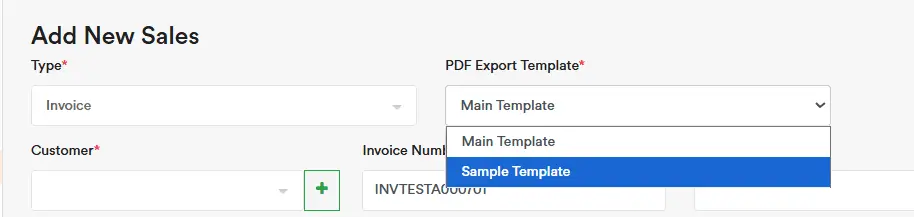

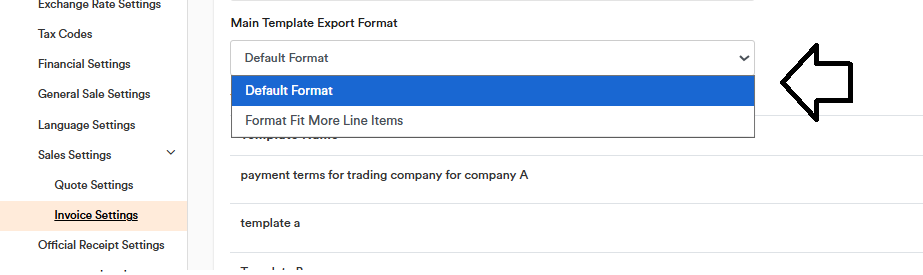

You can amend the tax invoice report output format in Invoice Settings.

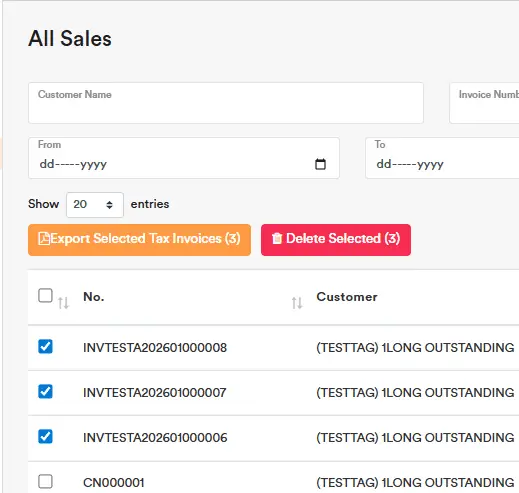

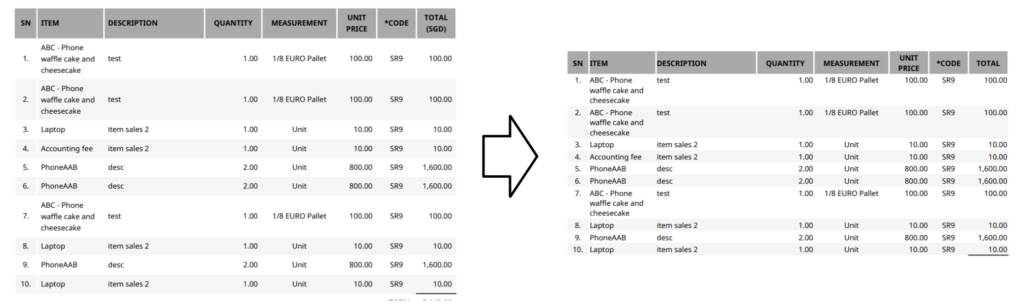

Download or Print Multiple Sales Invoices

You can select multiple invoices and click Export Selected Tax Invoices to export them all at once as a separate PDF file. You can then print the PDF.

You can amend the tax invoice report output format in Invoice Settings.

Sales Receipt Recording

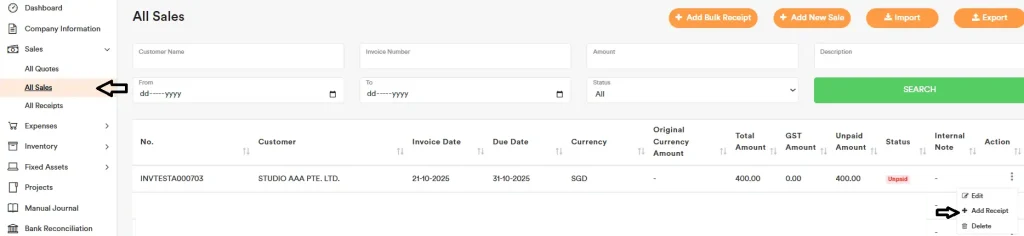

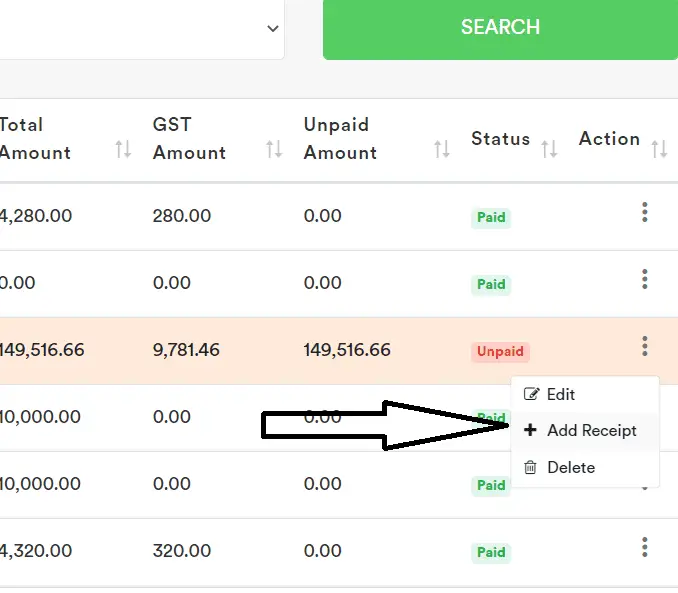

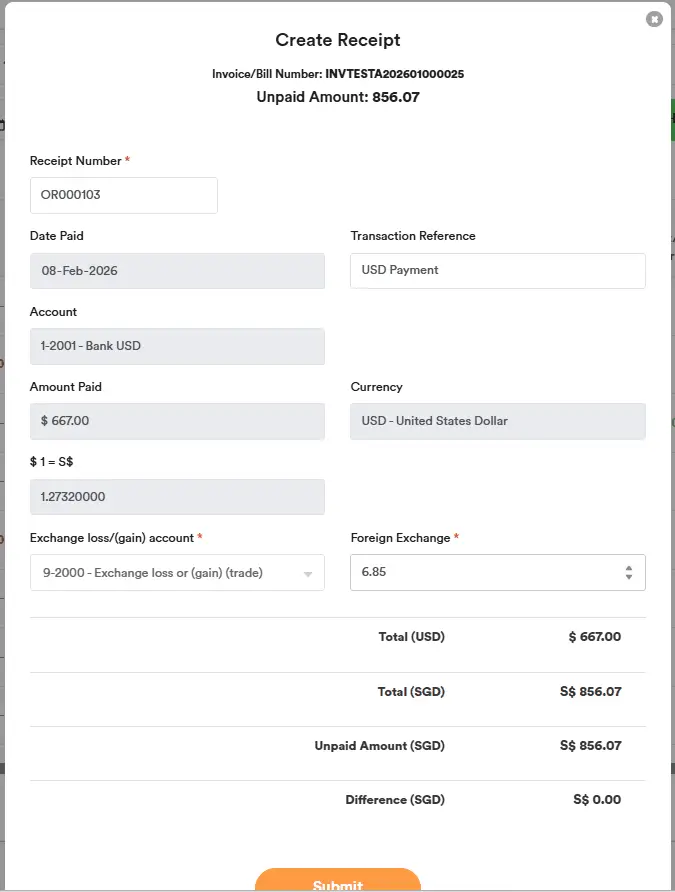

You can view the sales overview and, under Action, select ‘Add Receipt’ to record a receipt payment for a sales invoice.

To add payments for multiple invoices, click the Add Bulk Receipt button at the top.

Alternatively, open the sales transaction and click the Add Receipt button in the top-right.

You can also go to the All Receipts tab and click the Import button (top-right) to upload receipts in bulk via a CSV file.

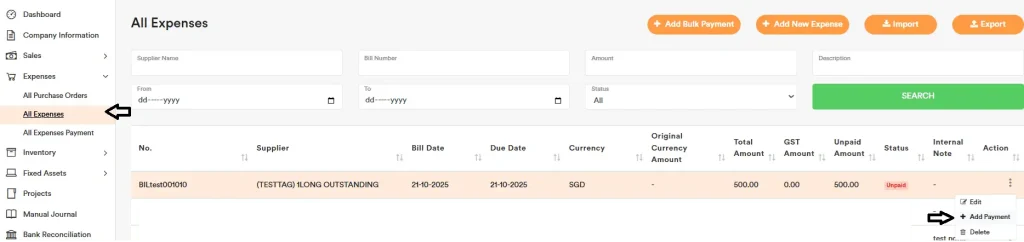

Expenses Recording

You can go to All Purchase Orders or All Expenses to start creating your purchase order and expenses transactions with quantity.

You can amend the expenses report output format in Bill Settings.

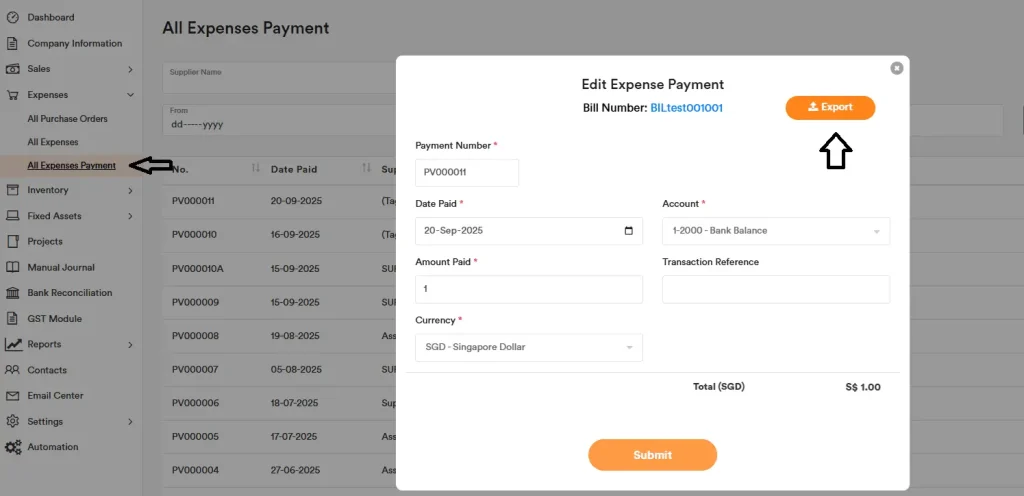

Expenses Payment Recording

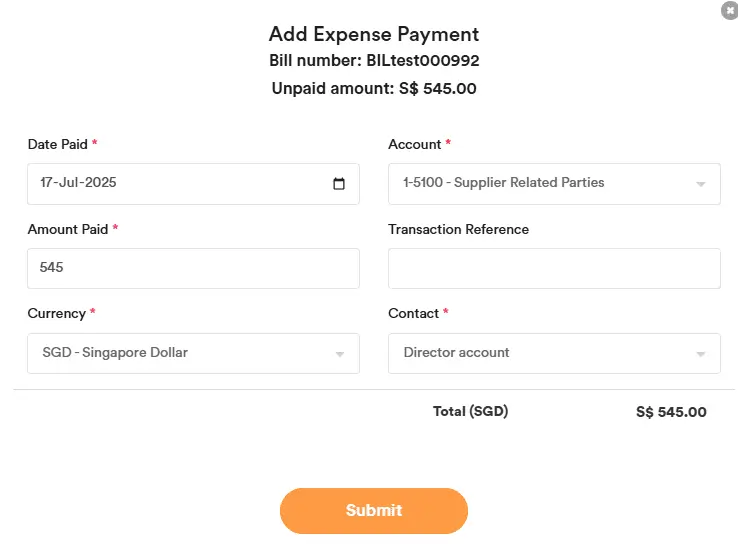

You can view the expenses overview and, under Action, select ‘Add Payment’ to record a payment for an expenses invoice.

To add payments for multiple invoices, click the Add Bulk Payment button at the top.

Alternatively, open the expenses transaction and click the Add Expense Payment button in the top-right.

You can also go to the All Expenses Payment tab and click the Import button (top-right) to upload payments in bulk via a CSV file.

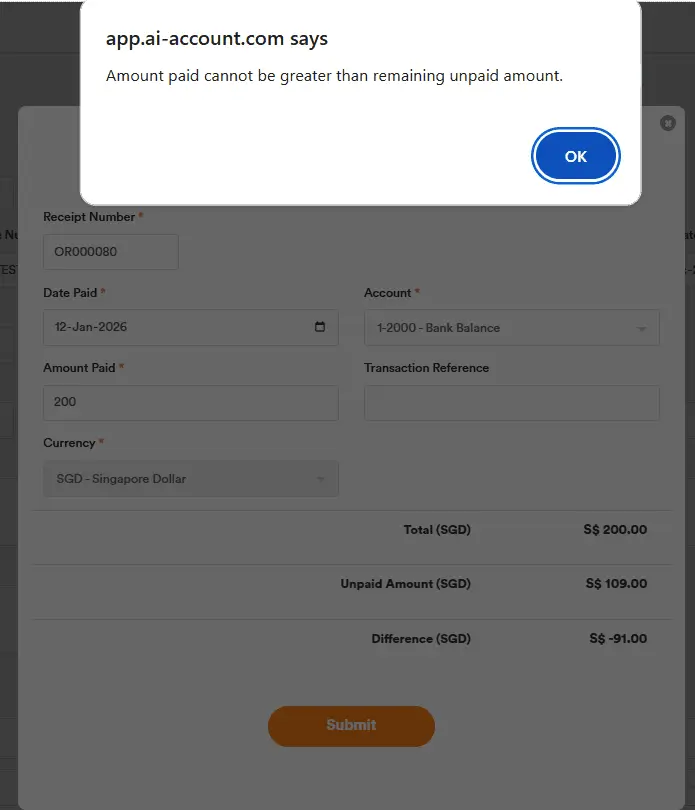

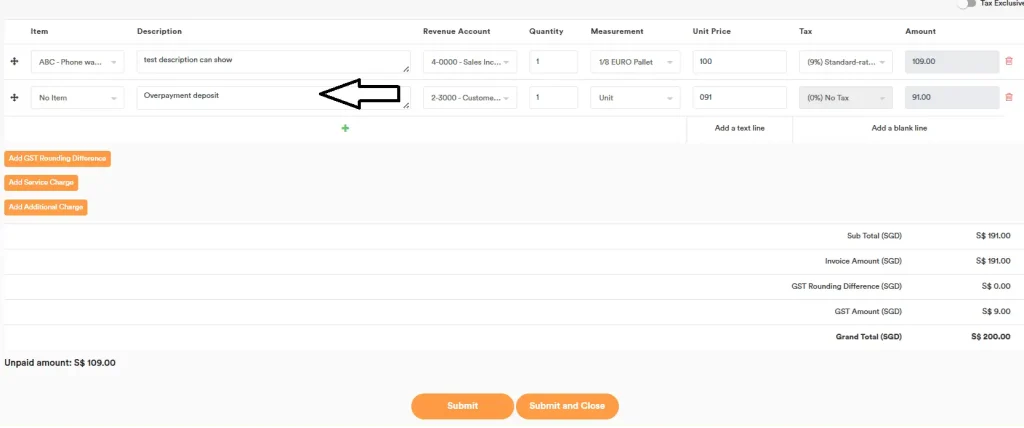

Overpayment Recording

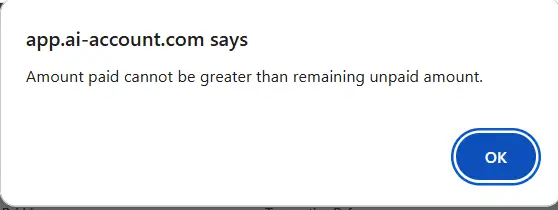

In the AI Account, we have controls to prevent overpaying an invoice.

For example, if an invoice has an outstanding balance of $109 and you try to pay $200, the system will display a warning (Amount paid cannot be greater than remaining unpaid amount.) and you won’t be able to proceed.

To record the overpayment, you need to add a line item on the invoice for the difference (e.g., Overpayment Deposit). You can post this to the Customer Deposit account. Then you can record the receipt for the full $200.

Alternatively, you may:

- Create a separate invoice (or document) to apply the excess payment, or

- Use a Bank Entry to record the difference as a separate payment.

We do not allow overpayments to be recorded directly against Trade Receivables, as this could cause the Trade Receivables balance to become negative, which is misleading. Instead, any excess payment should be recorded to a Customer Deposit (or similar liability) account and applied later.

You can use the Customer Deposit account to hold the overpayment and apply it to future unpaid invoices during payment. When making the payment, select Customer Deposit instead of the Bank account.

Credit Note or Debit Note

Sales Recording (CN & DN)

For a Debit Note, you can create it by selecting the Type = Debit Note, then choosing the customer contact. After that, you can select the related sales invoice associated with this debit note. Enter the Debit Note number in the Invoice Number field.

For a Credit Note / Refund Note, you can create the negative sales by selecting the Type = Credit Note / Refund Note, then choosing the customer contact. After that, you can select the related sales invoice associated with this credit note / refund note.

Tick Credit Apply to automatically apply the Credit Note amount to the invoice and offset it. Click Submit — the Credit Note will be applied automatically and the invoice balance will be reduced accordingly.

You will then see the invoice’s unpaid amount decrease by $5,000, and the Credit Note status will show as Paid.

Purchase Recording (CN & DN)

For a Debit Note, you can create it by selecting the Type = Debit Note, then choosing the supplier contact. After that, you can select the related purchase invoice associated with this debit note. Enter the Debit Note number in the Bill Number field.

For a Credit Note / Refund Note, you can create the negative expense and selecting the Type = Credit Note / Refund Note, then choosing the supplier contact. After that, you can select the related purchase invoice associated with this credit note / refund note.

Tick Credit Apply to automatically apply the Credit Note amount to the bill and offset it. Click Submit — the Credit Note will be applied automatically and the bill balance will be reduced accordingly.

You will then see the expense bill’s unpaid amount decrease by $54.50, and the Credit Note status will show as Paid.

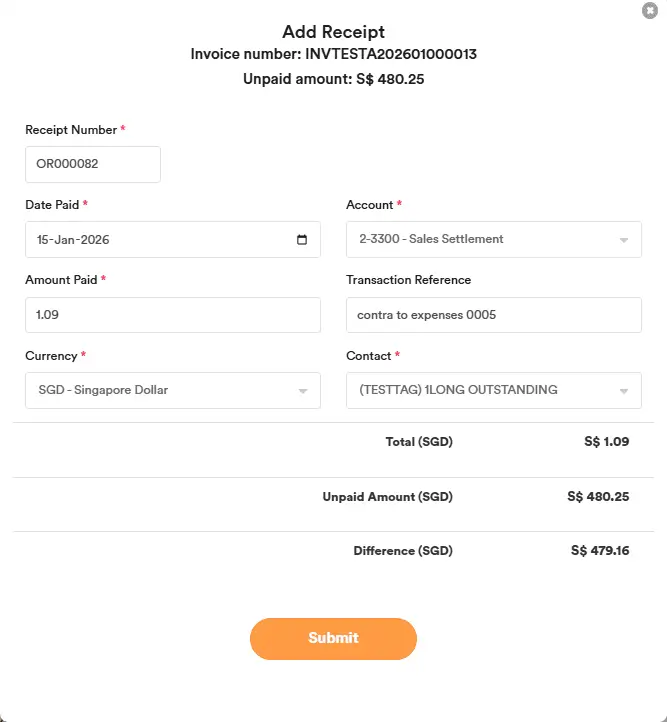

Sales Recording (CN & DN) – Manual Recording Process

For a Debit Note, you can create it by selecting the Type = Debit Note, then choosing the customer contact. After that, you can select the related sales invoice associated with this debit note. Enter the Debit Note number in the Invoice Number field.

For a Credit Note / Refund Note, you can create the negative sales by selecting the Type = Credit Note / Refund Note, then choosing the customer contact. After that, you can select the related sales invoice associated with this credit note / refund note.

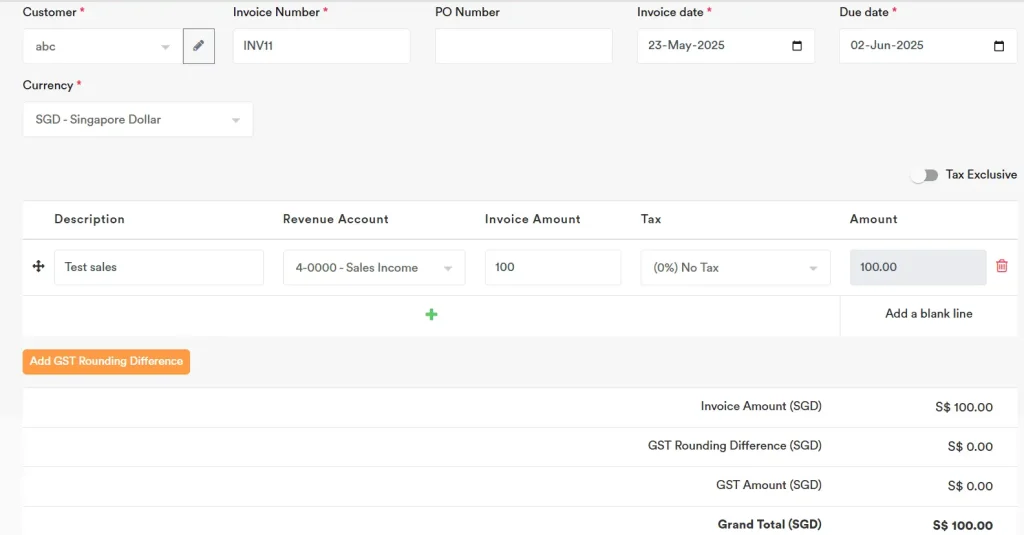

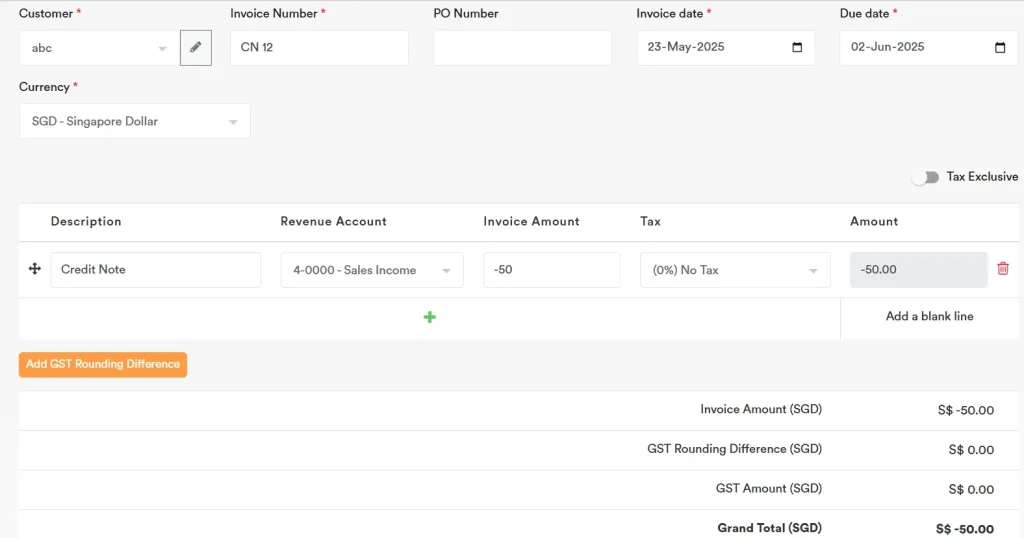

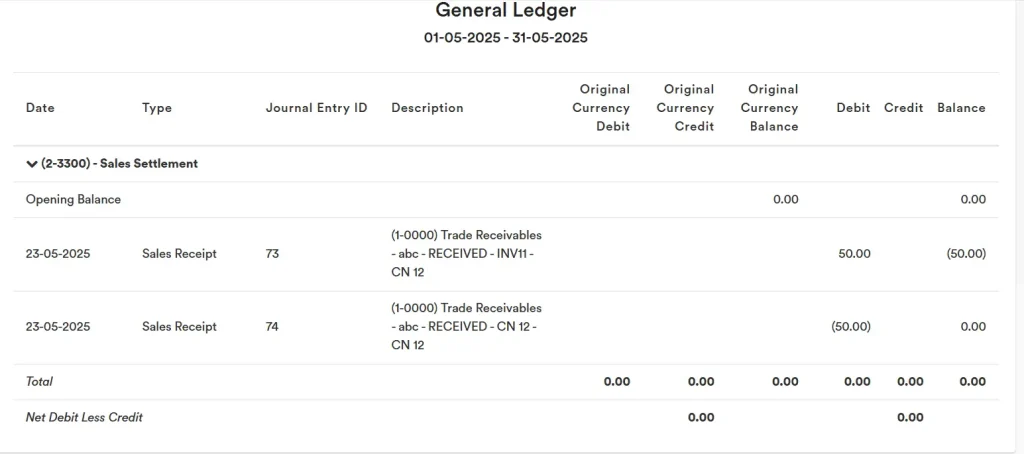

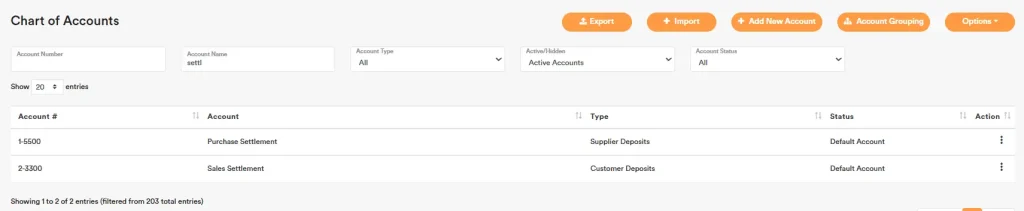

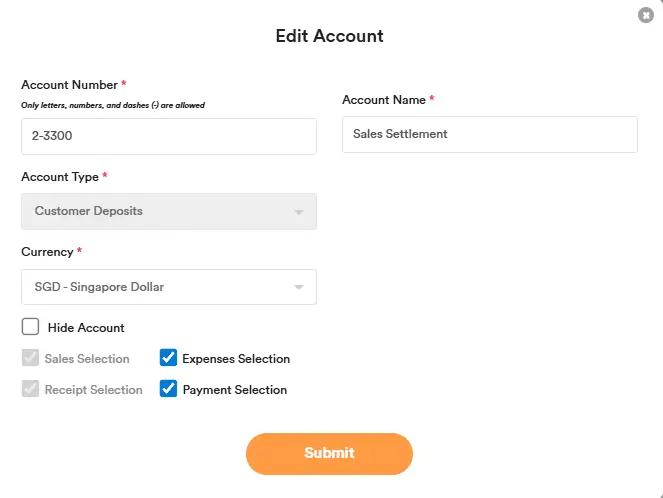

You can settle the credit note / refund note through the “2-3300 Sales Settlement” account. So both the invoices and credit note / refund note will offset their settlement in the “2-3300 Sales Settlement” account. Example:

1. Created the Sales Invoice.

2. Created the Credit Note (input like a normal Sales Invoice) below in the Sales section. The CN number can be entered in the “Invoice Number” field, and the amount should be negative since it is a credit note and will reduce the sales income previously invoiced to the client.

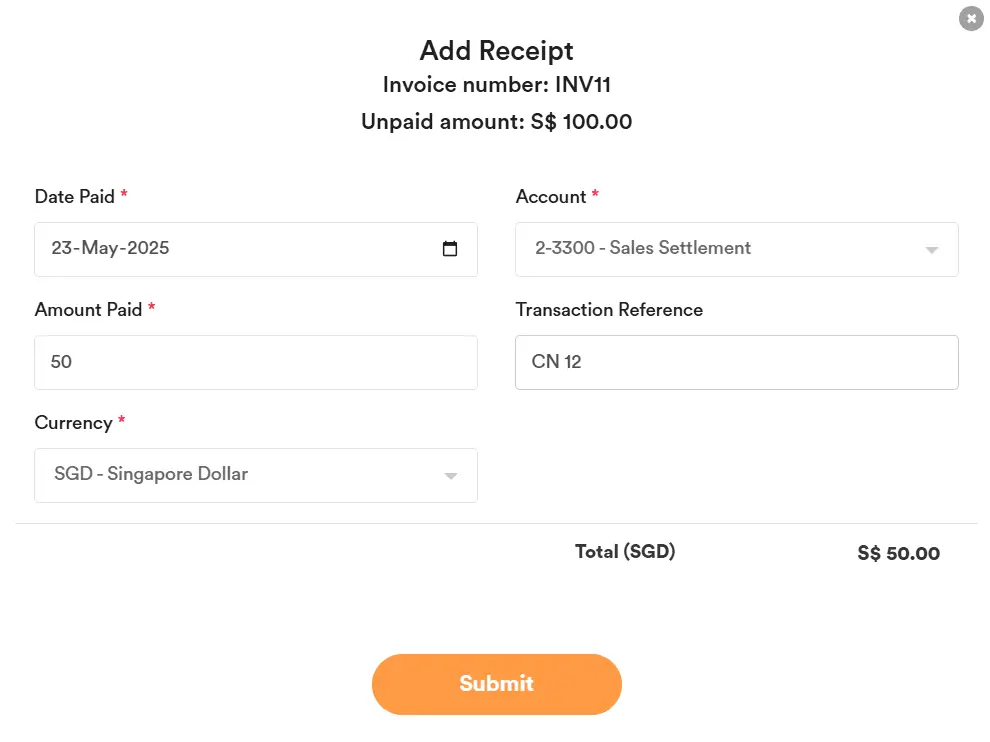

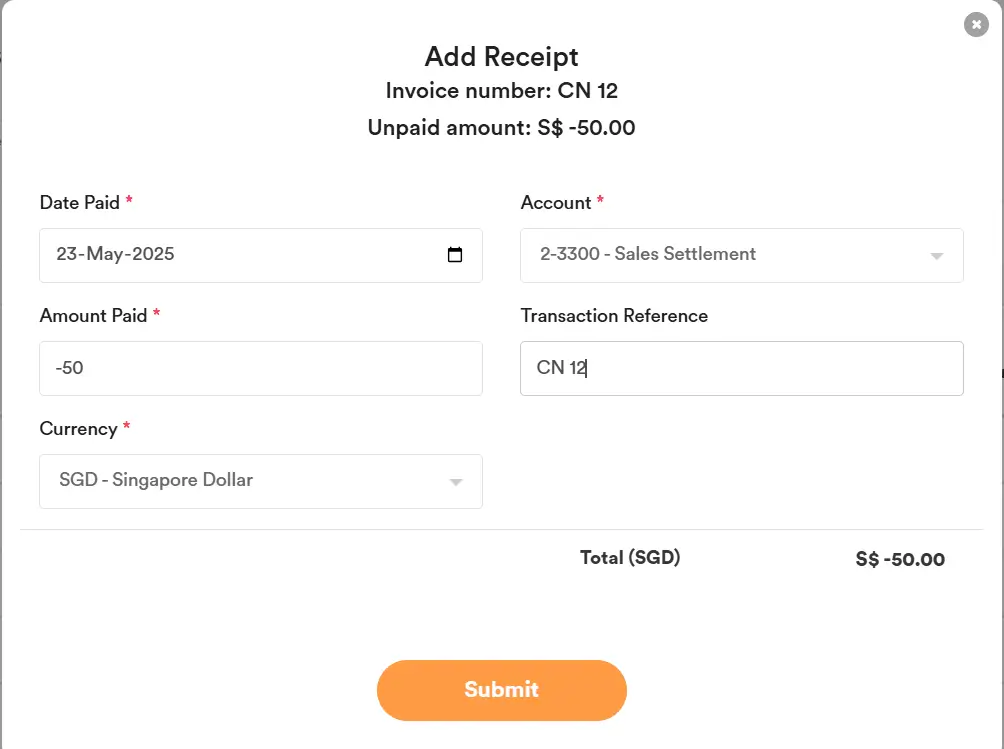

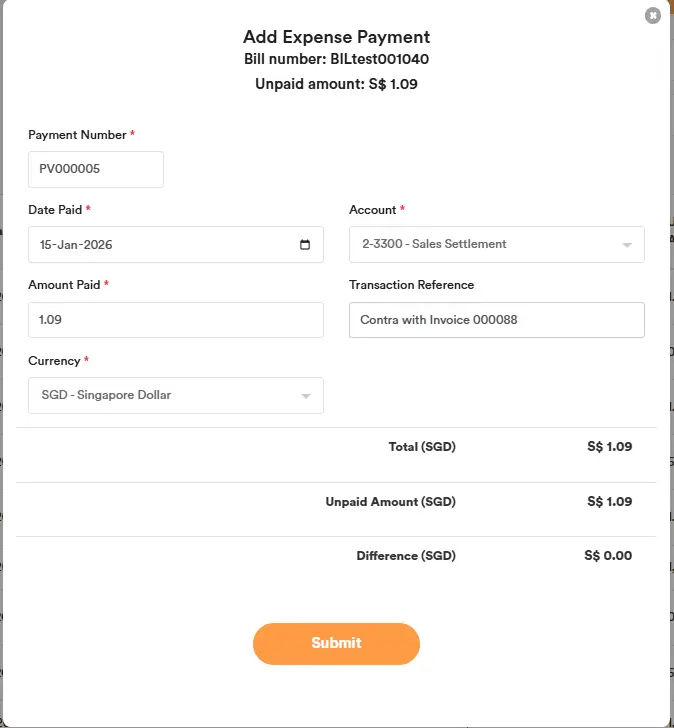

3. You can add the Receipt for the Sales Invoice and select the “2-3300 Sales Settlement” account. Select the amount to offset the Credit Note, and input the Credit Note number in the Transaction Reference field for easier tracking.

4. You can add the Receipt for the Credit Note and select the “2-3300 Sales Settlement” account. Select the amount to offset the Credit Note against the invoice, and input the Credit Note number in the Transaction Reference field for easier tracking.

5. Thereafter, you can see the Invoice unpaid amount becomes $50 after offsetting the issued Credit Note.

6. The Sales Settlement account will show as below and net off to zero.

Purchase Recording (CN & DN) – Manual Recording Process

For a Debit Note, you can create it by selecting the Type = Debit Note, then choosing the supplier contact. After that, you can select the related purchase invoice associated with this debit note. Enter the Debit Note number in the Bill Number field.

For a Credit Note / Refund Note, you can create the negative expense and selecting the Type = Credit Note / Refund Note, then choosing the supplier contact. After that, you can select the related purchase invoice associated with this credit note / refund note.

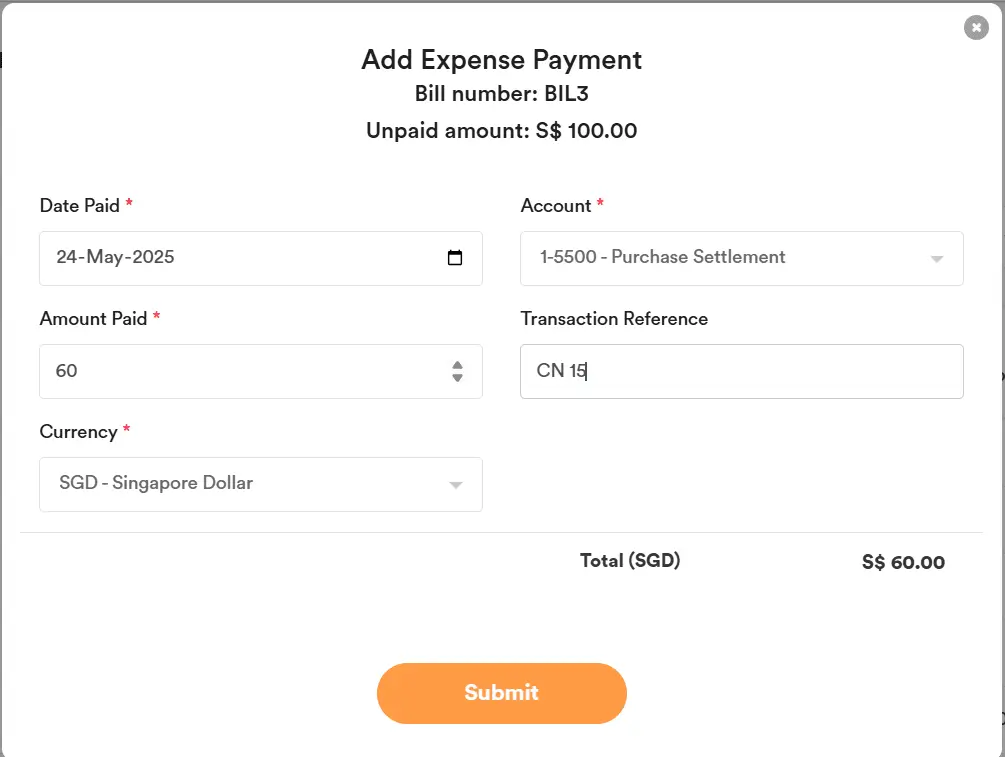

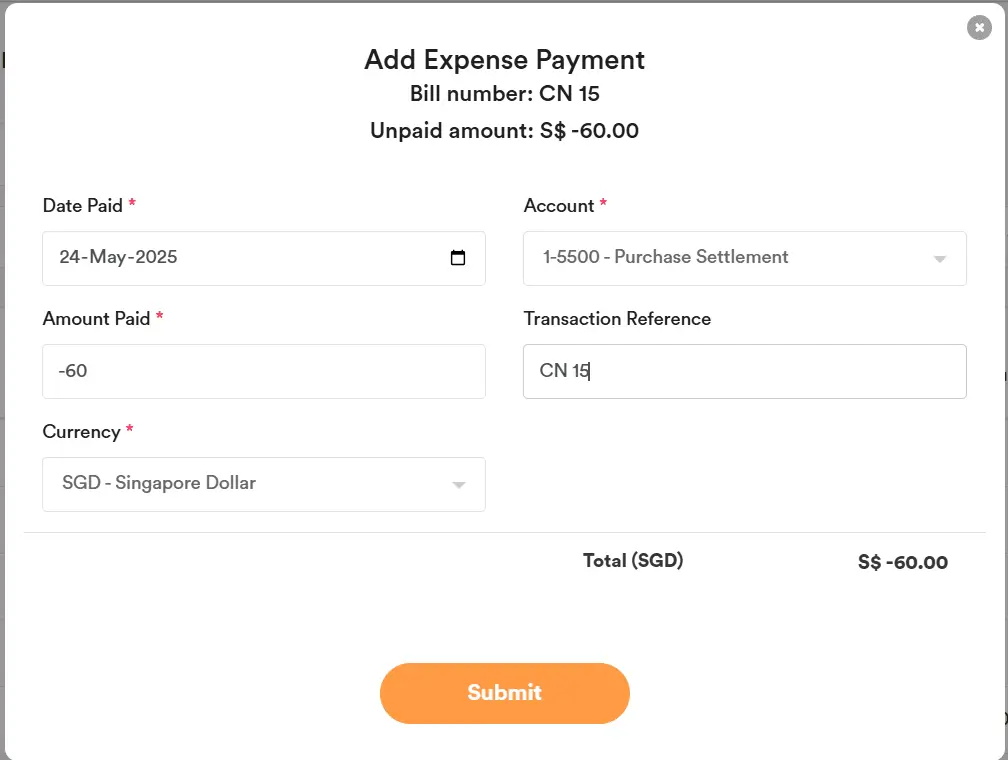

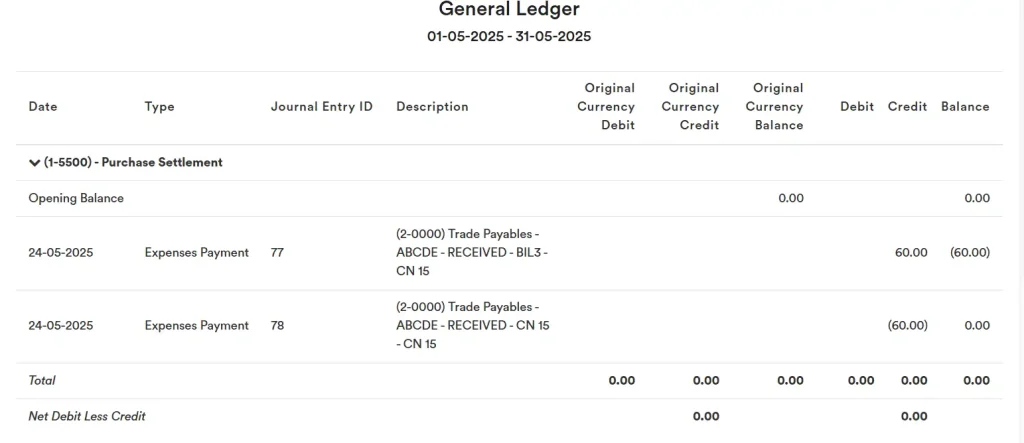

You can settle the credit note / refund note through the “1-5500 Purchase Settlement” account. So both the invoices and credit note / refund note will offset their settlement in the “1-5500 Purchase Settlement” account. Example:

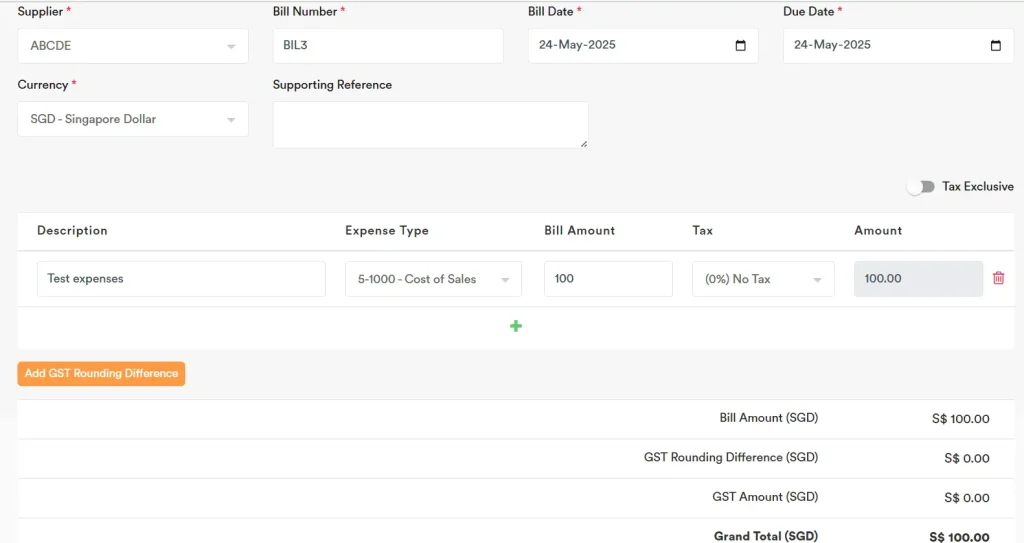

1. Created the Expense.

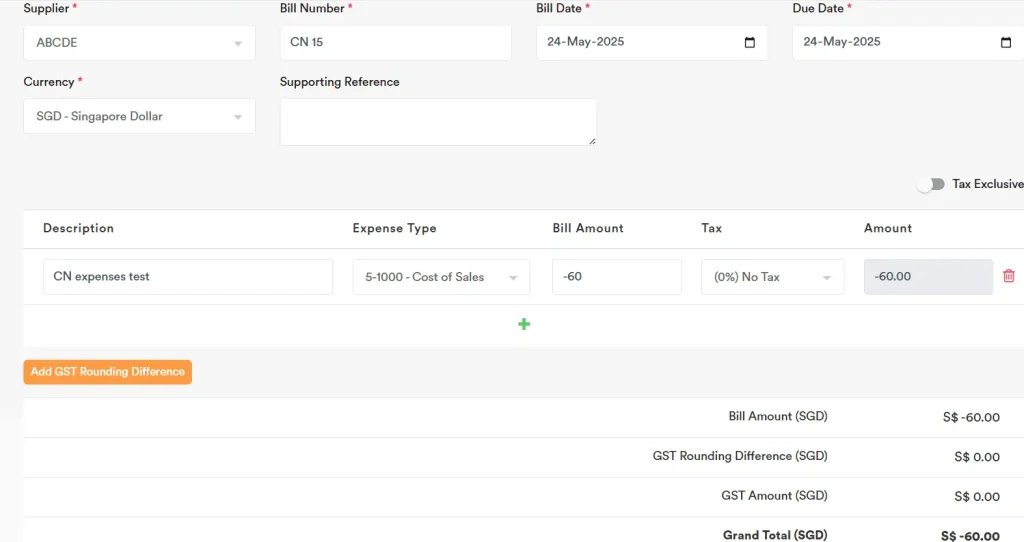

2. Created the Credit Note (input like a normal Expenses Invoice) below in the Expenses section. The CN number can be entered in the “Bill Number” field, and the amount should be negative since it is a credit note and will reduce the expenses previously billed from the vendor.

3. You can add the Payment for the Expenses Invoice and select the “1-5500 Purchase Settlement” account. Select the amount to offset the Credit Note, and input the Credit Note number in the Transaction Reference field for easier tracking.

4. You can add the Payment for the Credit Note and select the “1-5500 Purchase Settlement” account. Select the amount to offset the Credit Note against the invoice, and input the Credit Note number in the Transaction Reference field for easier tracking.

5. Thereafter, you can see the Invoice unpaid amount becomes $40 after offsetting the issued Credit Note.

6. The Purchase Settlement account will show as below and net off to zero.

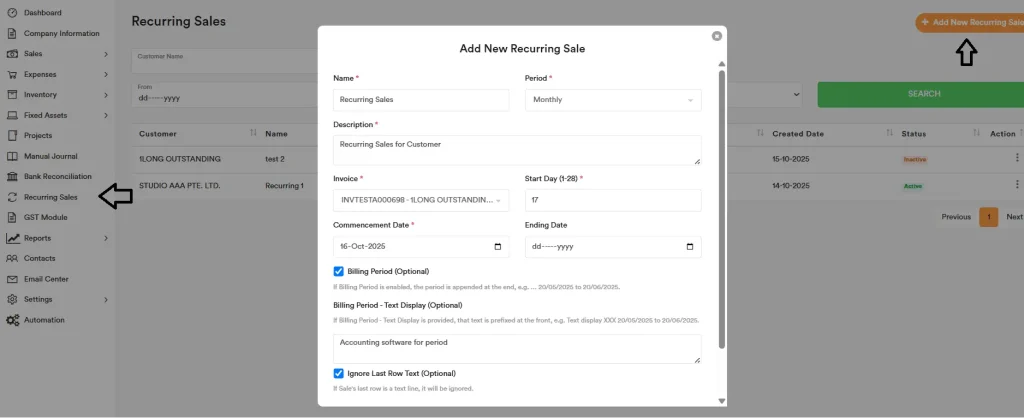

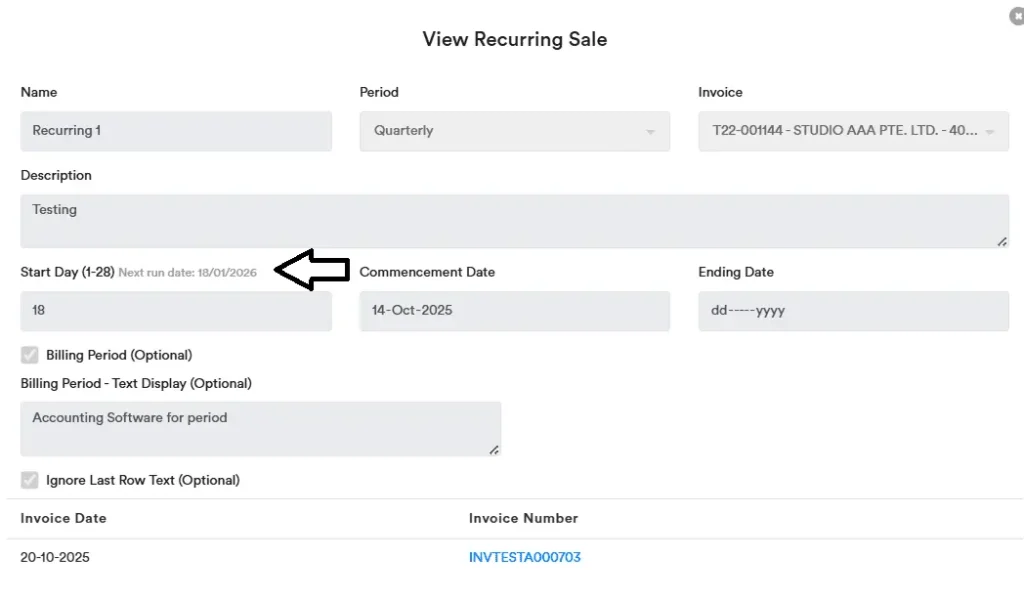

Recurring Sales

You can create invoices automatically on a schedule (monthly, quarterly, etc.) from a chosen invoice template.

Create a recurring sale

1. Open the Recurring Sales module

2. Click Add New Recurring Sale (top-right).

3. Fill in the form

Name: An internal name (e.g., “Studio AAA – Support Retainer”).

Period: Choose Monthly, Quarterly, Half Yearly, Yearly.

Description: Optional note for your internal reference.

Invoice: Pick the existing invoice (in ‘All Sales’ module) to use as the template (its customer, currency, lines and taxes carry over).

Start Day (1–28): Day of the month/quarter to generate the invoice (e.g., 17).

Commencement Date: The first cycle’s reference date (e.g., 16-Oct-2025).

Ending Date (optional): Leave blank for ongoing; fill to stop on a specific date.

Billing Period (Optional): Enable to append a billing window to the last line (e.g., “17/10/2025 to 17/11/2025.”).

Billing Period – Text Display (Optional): Optional prefix (e.g., “Accounting software for period”).

Ignore Last Row Text (Optional): If the template’s last line is text-only line, tick this to skip that line when generating the invoice and avoid duplicating the billing-period text.

4. Click ‘Submit’ to activate. The entry will appear in the Recurring Sales list with Active status.

5. On the day after the job runs, you can open the record to see the generated invoice. Select the invoice number to open and verify it.

You can also see the Next Run Date beside the Start Day indicated below, so you’ll know when the recurring sales invoice will be generated next.

How the schedule works (examples)

Monthly, Start Day = 17

First invoice generates on 17 Oct 2025, then every 17th of the month (e.g., 17 Nov 2025, 17 Dec 2025, …).

Quarterly, Start Day = 17

First invoice generated on 17 Oct 2025, next on 17 Jan 2026, then 17 Apr 2026, etc.

If the selected Ending Date is reached, generation stops after that cycle.

What gets copied each cycle

Customer, addresses, currency, tax settings.

Line items, quantities, and unit prices from the chosen Invoice.

Remarks/Internal Note from the template invoice (edit the template if you want different wording).

Where to find generated invoices

Each invoice is created on the run day and appears under ‘All Sales’ (and is linked from the Recurring Sales record). Review/send at Email Center as per your normal process.

Edit, pause, or stop

Go to Recurring Sales, open the record:

1. Update fields (e.g., change Period, Start Day, Ending Date).

2. To permanently stop, set an Ending Date in the past or mark Set to Inactive.

Good templates = smooth automation

Before you create the recurrence:

- Build a clean invoice template with the correct customer, tax code, revenue account, and line items.

- Put any repeating billing-window text on the last line (or enable Billing Period so the system appends it for you). Tick Ignore Last Row Text to avoid duplication if applicable.

FAQs

What if the month doesn’t have my Start Day (e.g., 29/30/31)?

Use a day 1–28 to avoid skipped months.Data security is crucial in account software to protect sensitive financial information, comply with data privacy regulations, and prevent data breaches.

Can I change prices mid-contract?

Yes—update the invoice template or edit the Recurring Sale and it will apply to future runs.

When are recurring invoices generated?

The system runs once daily at 1:00 AM Singapore Time (GMT+8). Any Active Recurring Sale that meets the schedule will generate an invoice at that time (e.g., today’s date matches the Start Day, the Commencement Date is on/before today, and it hasn’t passed the Ending Date).

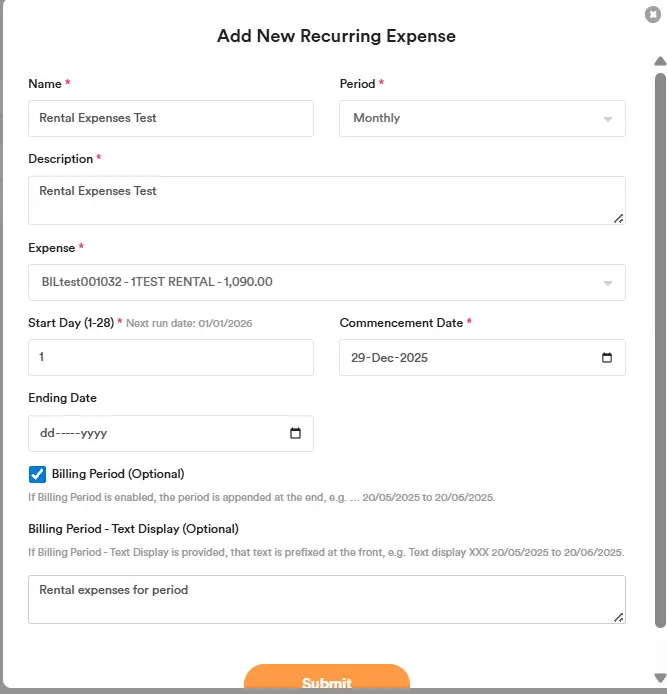

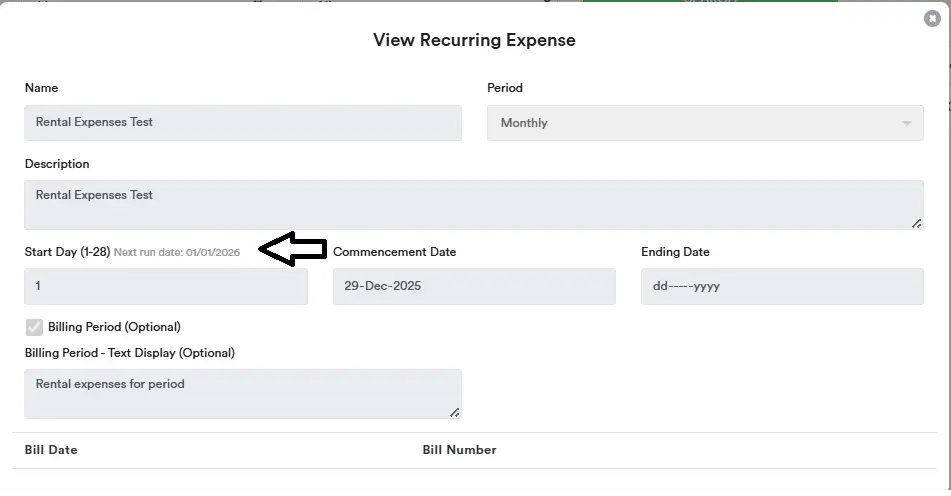

Recurring Expenses

Note: Recurring expenses work similarly to recurring sales. You can refer to the Recurring Sales section for details on how the logic works.

You can create expenses bills automatically on a schedule (monthly, quarterly, etc.) from a chosen expenses template.

Create a recurring expenses

- Open the Recurring Expenses module

- Click Add New Recurring Expenses (top-right).

- Fill in the form

Name: An internal name (e.g., “Rental Expenses Test”).

Period: Choose Monthly, Quarterly, Half Yearly, Yearly.

Description: Optional note for your internal reference.

Invoice: Pick the existing expenses (in ‘All Expenses’ module) to use as the template (its supplier, currency, lines and taxes carry over).

Start Day (1–28): Day of the month/quarter to generate the invoice (e.g., 17).

Commencement Date: The first cycle’s reference date (e.g., 29-Dec-2025).

Ending Date (optional): Leave blank for ongoing; fill to stop on a specific date.

Billing Period (Optional): Enable to append a billing window to the last line (e.g., “1/1/2026 to 1/2/2026.”).

Billing Period – Text Display (Optional): Optional prefix (e.g., “Rental expenses for period”).

Ignore Last Row Text (Optional): If the template’s last line is text-only line, tick this to skip that line when generating the expenses and avoid duplicating the billing-period text. - Click ‘Submit’ to activate. The entry will appear in the Recurring Expenses list with Active status.

5. On the day after the job runs, you can open the record to see the generated expenses. Select the expenses number to open and verify it. You can also see the Next Run Date beside the Start Day indicated below, so you’ll know when the recurring expenses will be generated next.

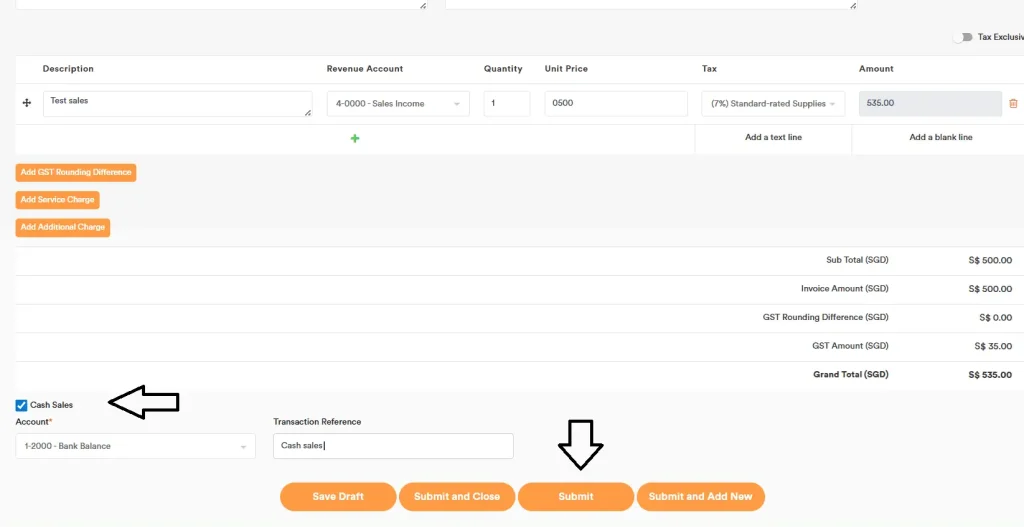

Cash Sales or Cash Expenses

To record cash sales or cash expenses, navigate to the “All Sales” or “All Expenses” section. When entering a new transaction, check the “Cash Sales” or “Cash Expenses” box at the bottom during the data entry, then select the appropriate bank or cash account.

Example: Go to ‘All Sales’ and click ‘Add New Sale’.

Enter the sales details.

At the bottom, tick ‘Cash Sales’.

Select the bank account that will receive the cash.

Enter a transaction reference if any.

Click Submit to save the cash sale.

Use the similar steps for recording Cash Expenses at ‘All Expenses’ section.

Alternatively, use the Bank Entry section to record the cash sales and cash expenses transaction directly to the bank, without recording trade or other receivables/payables.

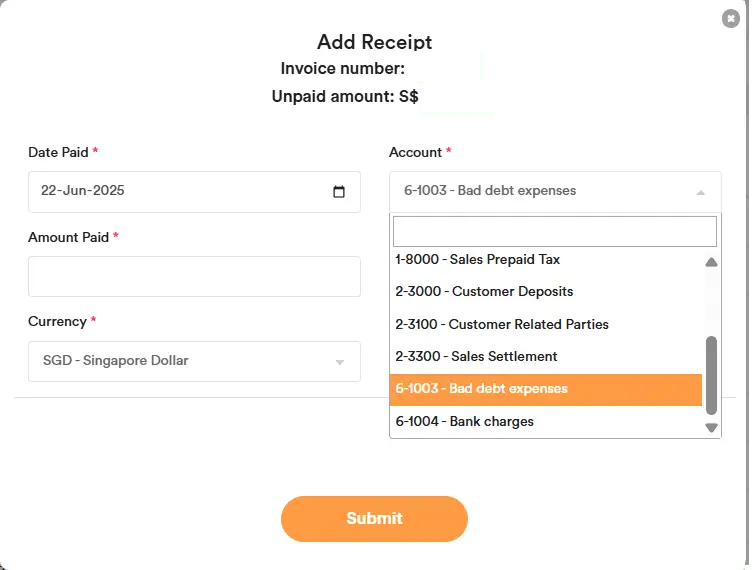

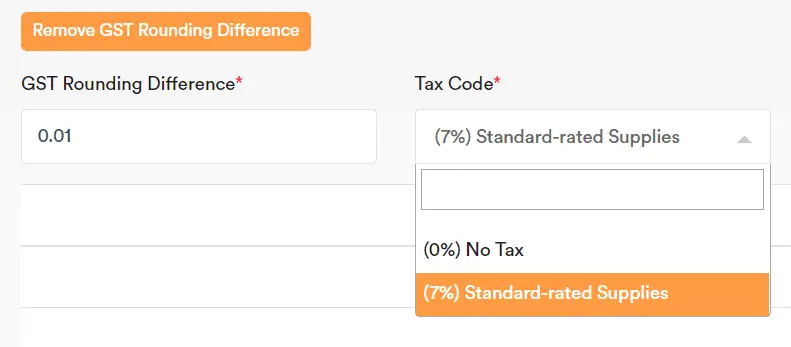

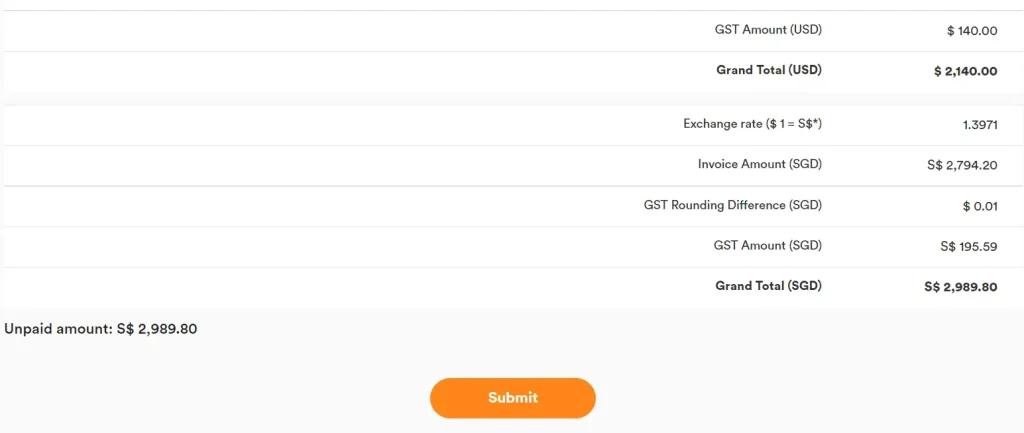

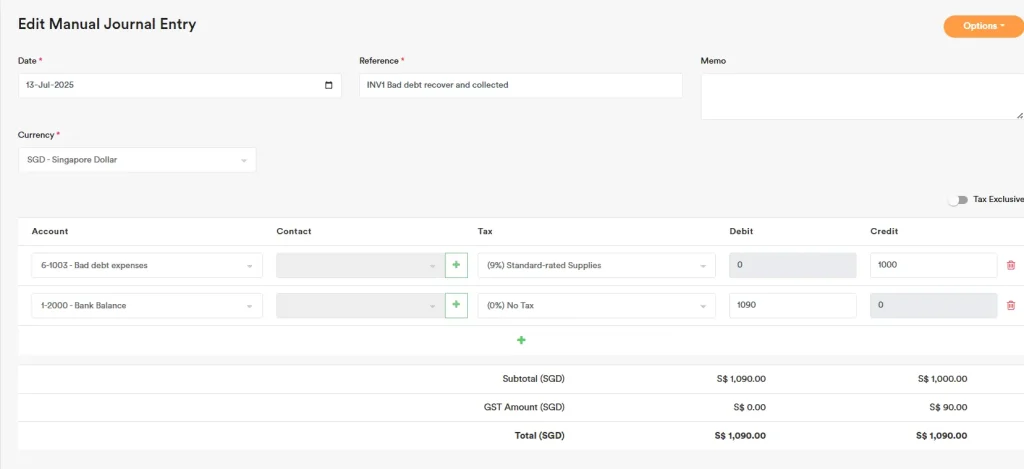

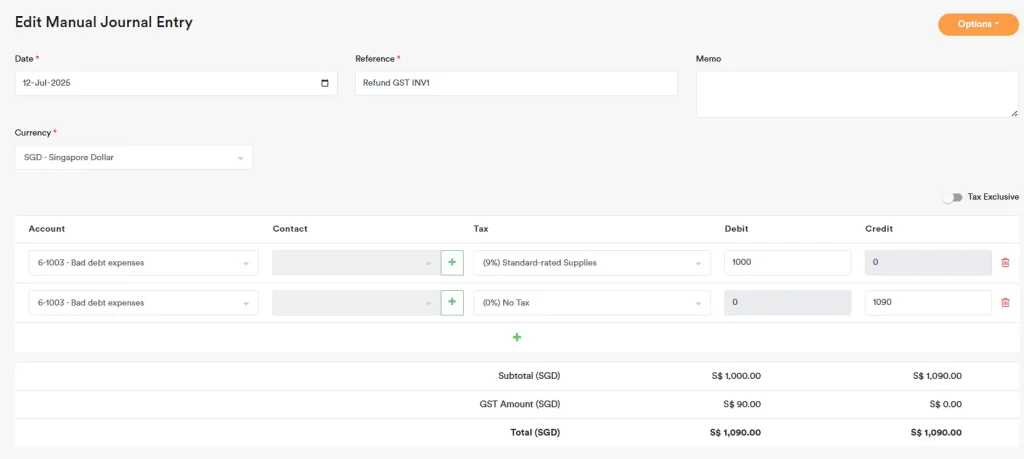

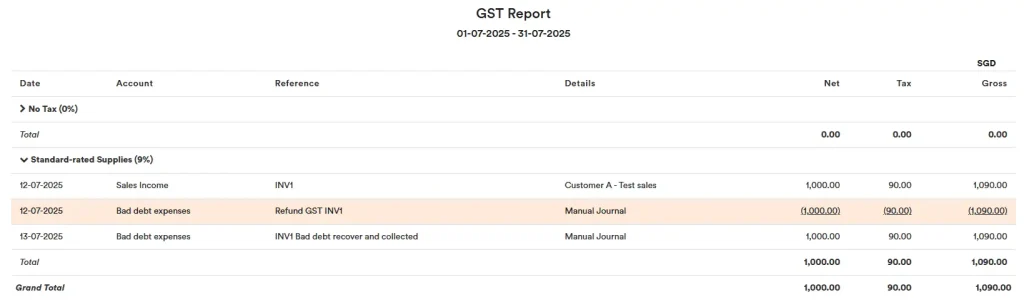

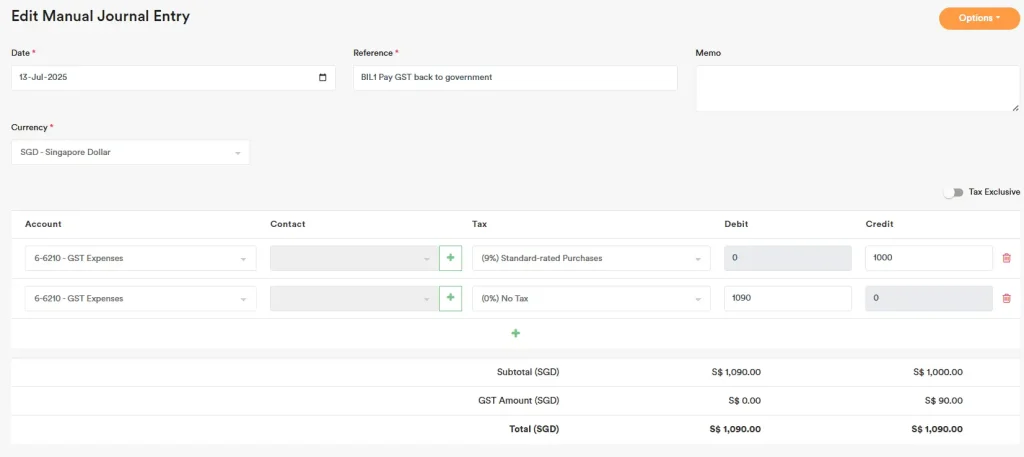

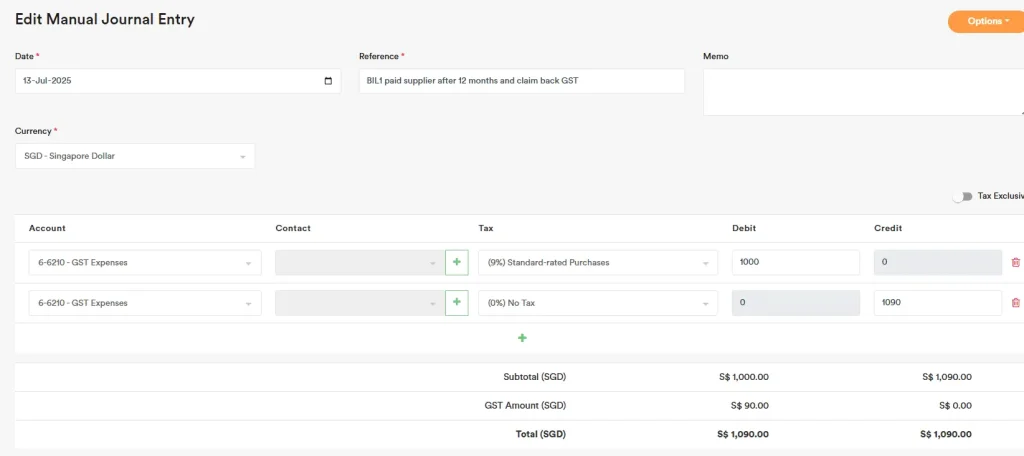

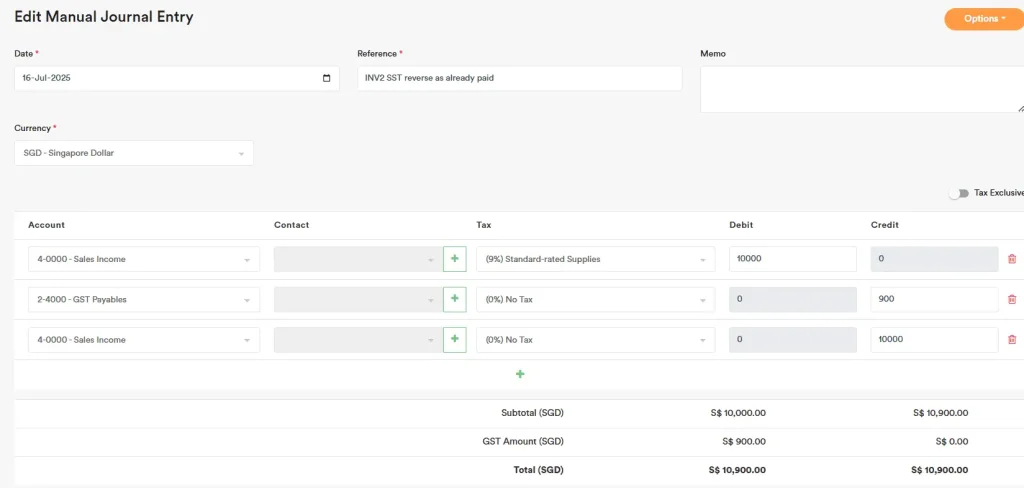

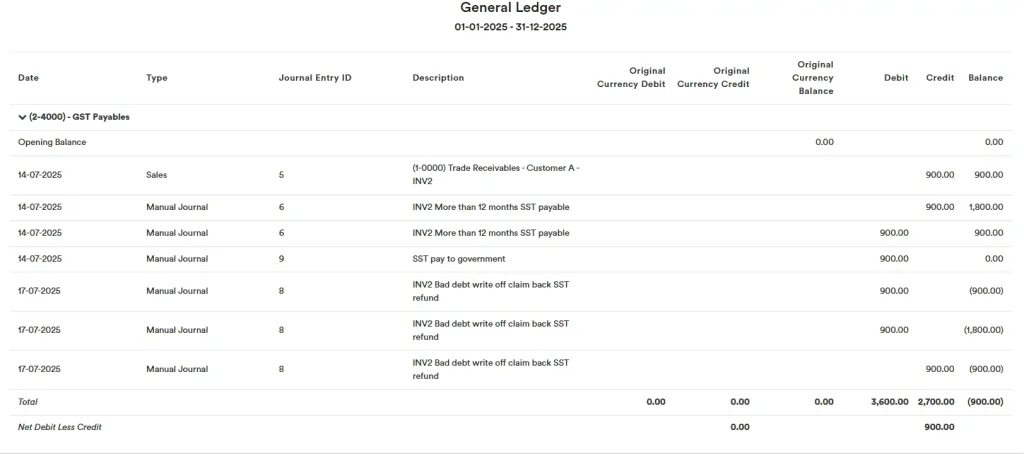

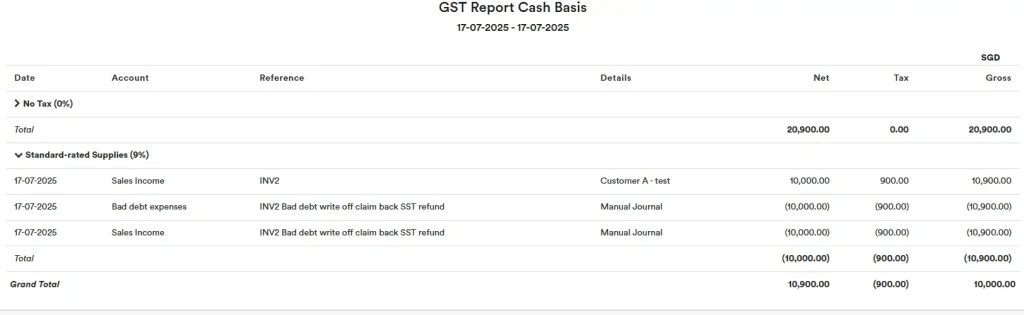

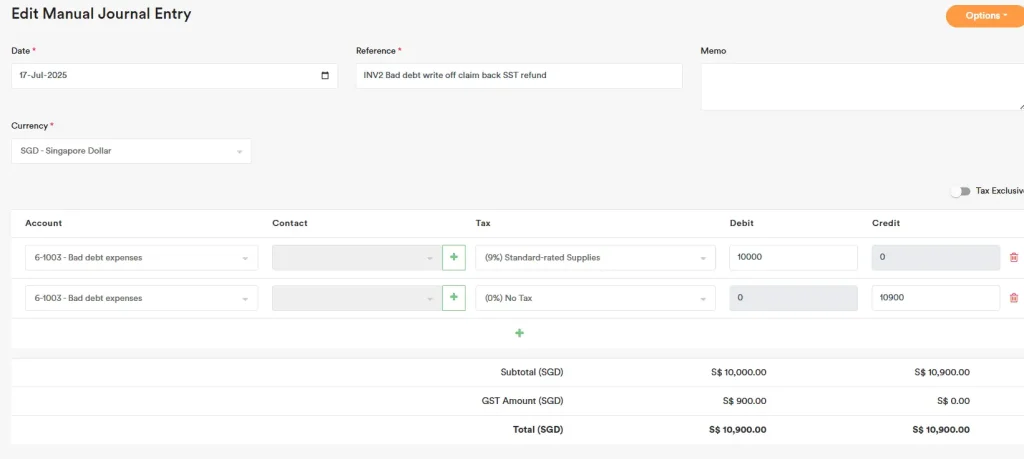

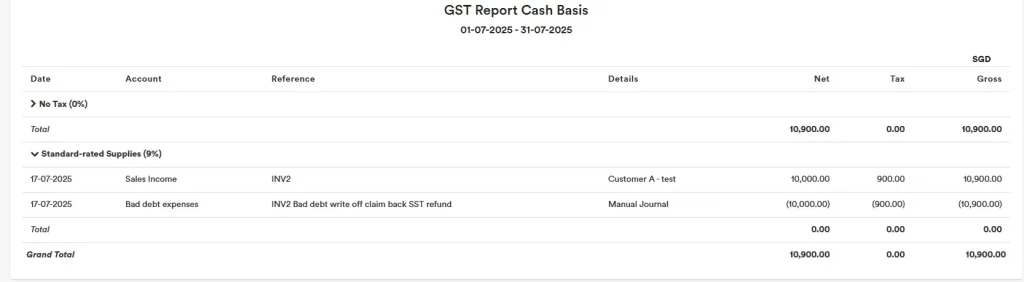

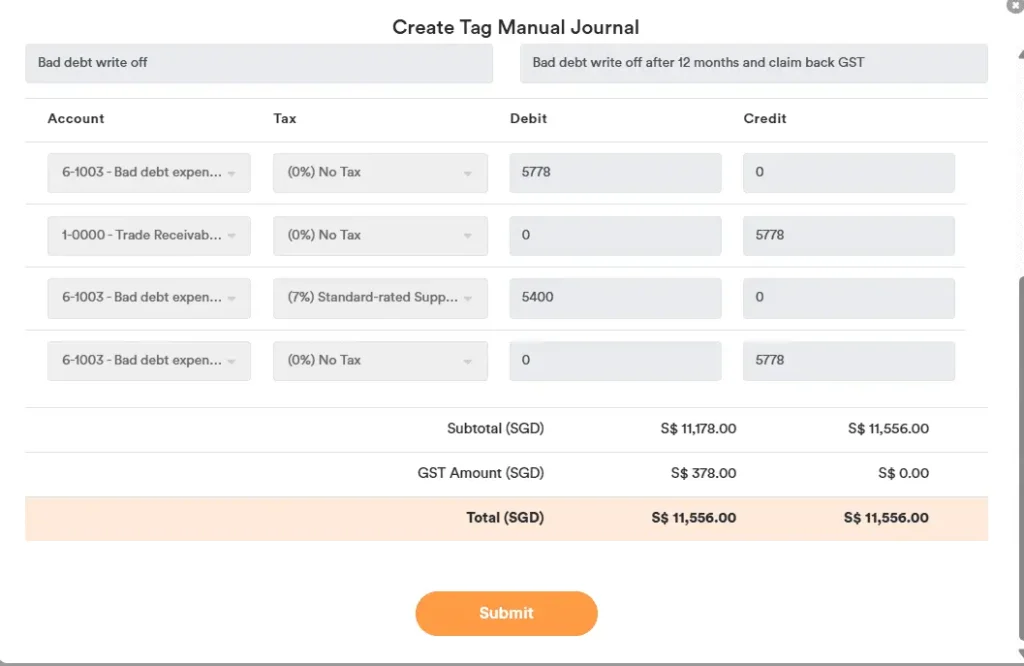

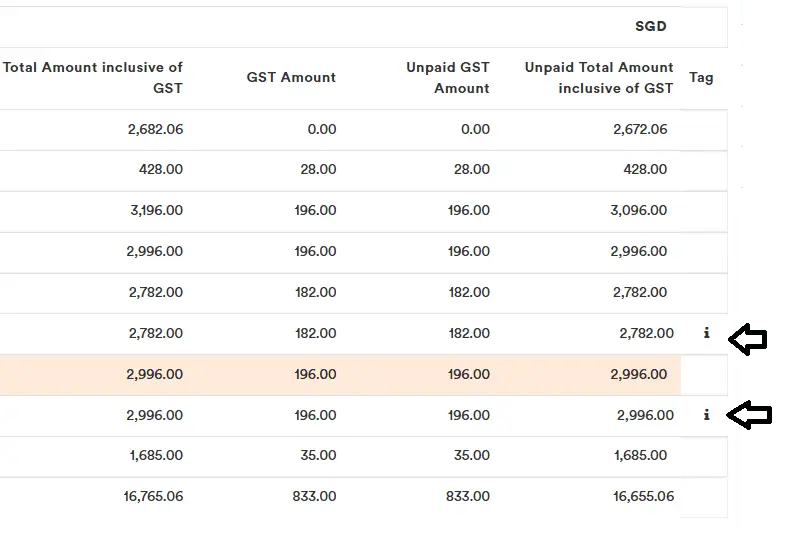

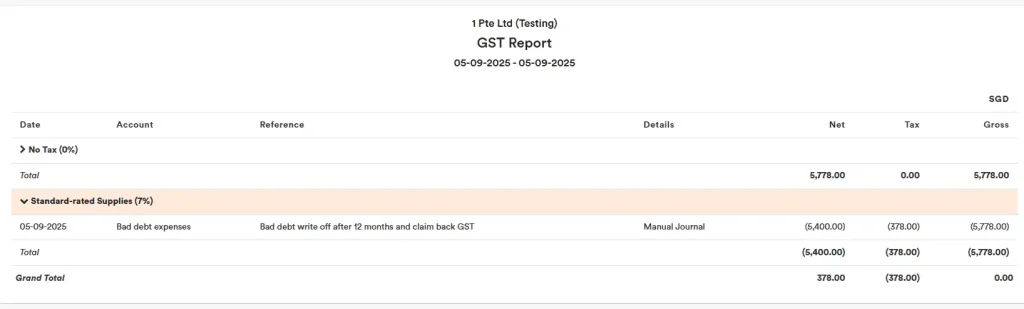

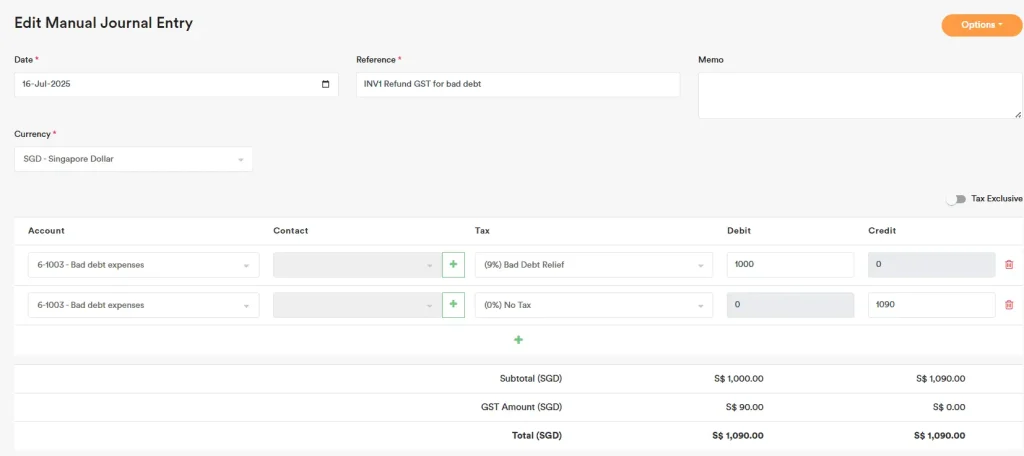

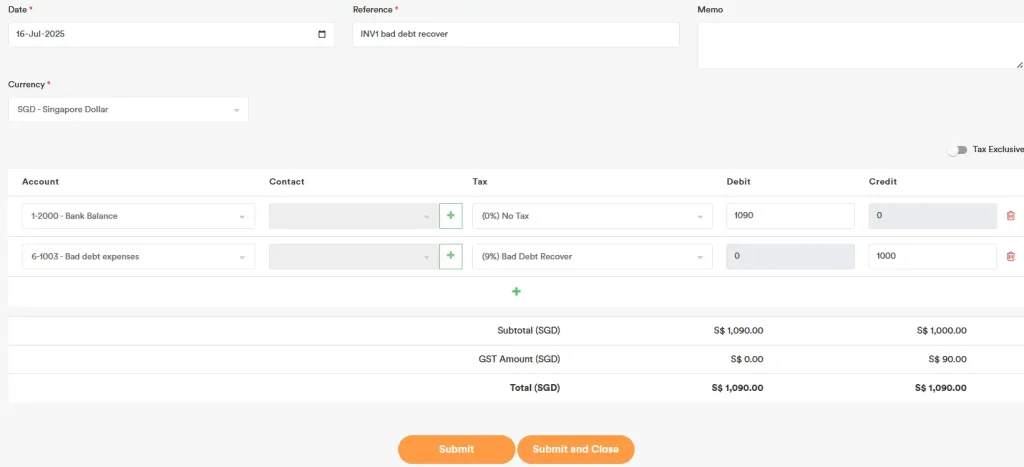

Bad Debt Recording

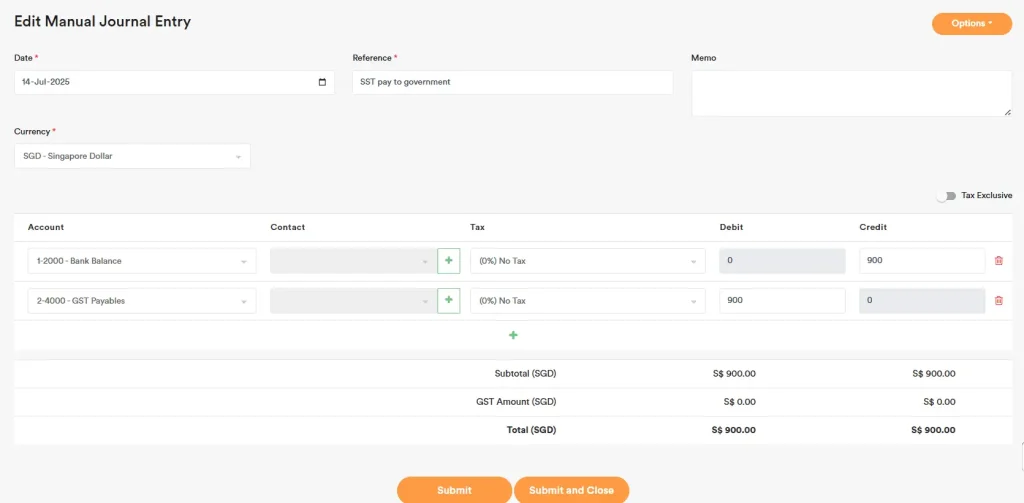

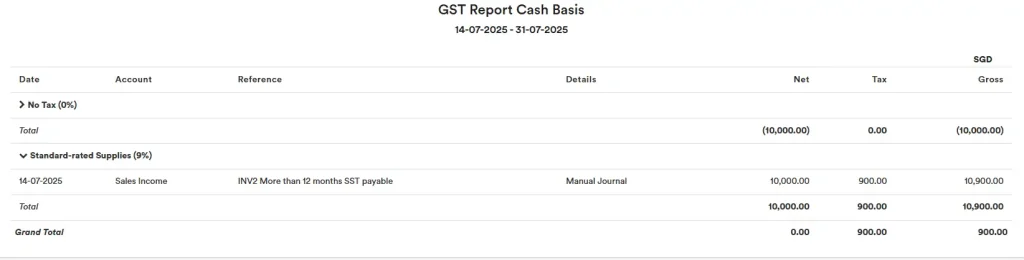

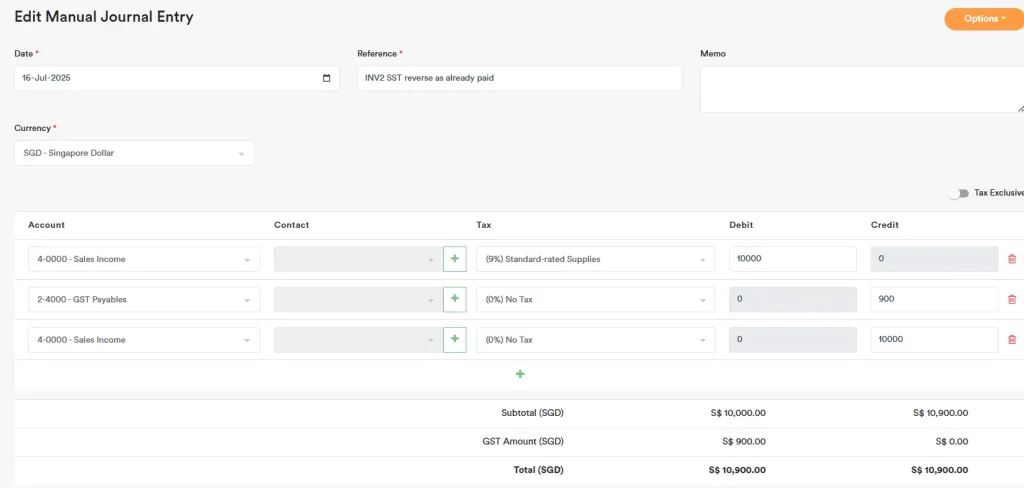

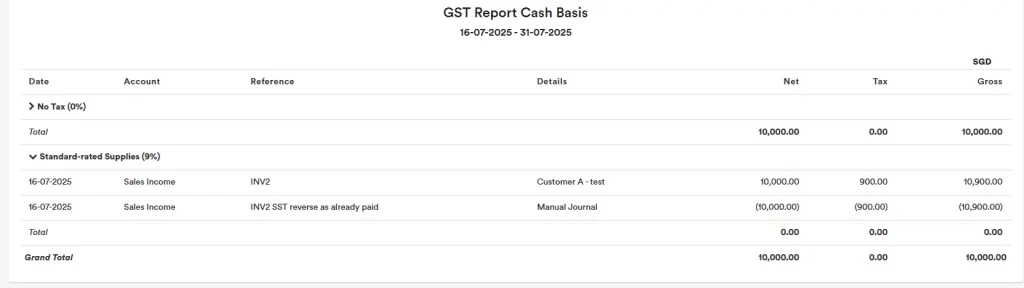

To write off trade and other receivables as bad debts, select the payment of the invoice and allocate it to the account “6-1003 – Bad Debt Expenses”. Thereafter, if GST was previously paid to the government, you can pass a manual journal entry to reverse the GST amount in order to claim it back from the government.

Example: Dr 2-4000 – GST Payables Cr 6-1003 – Bad debt expenses

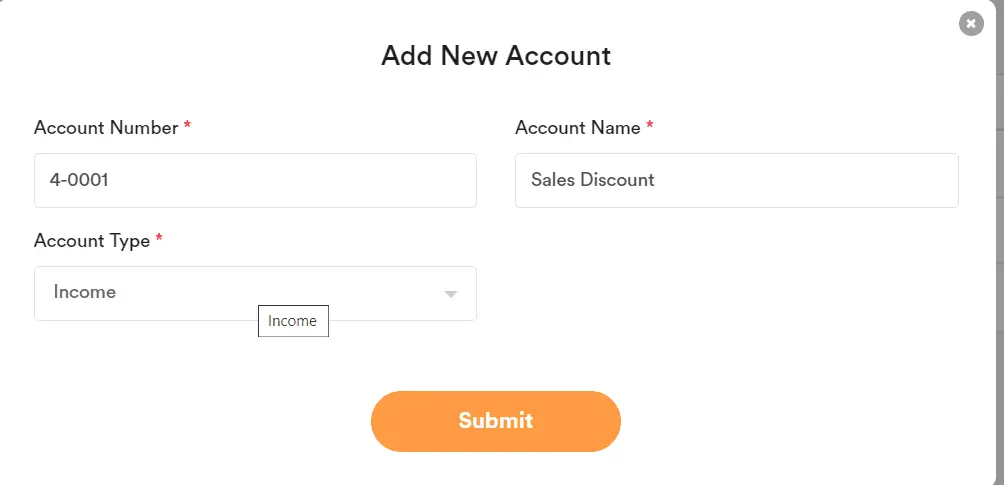

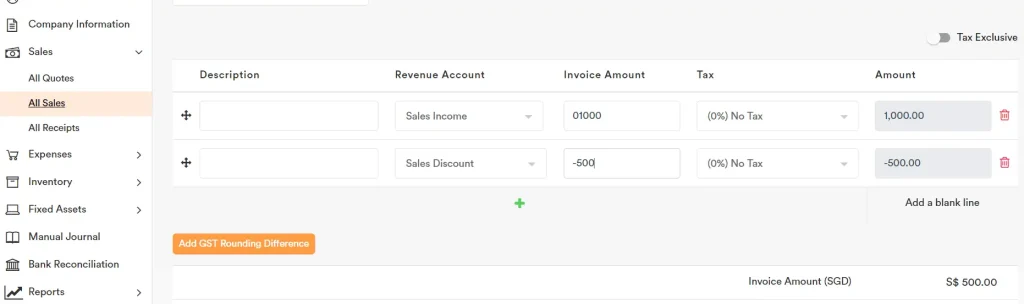

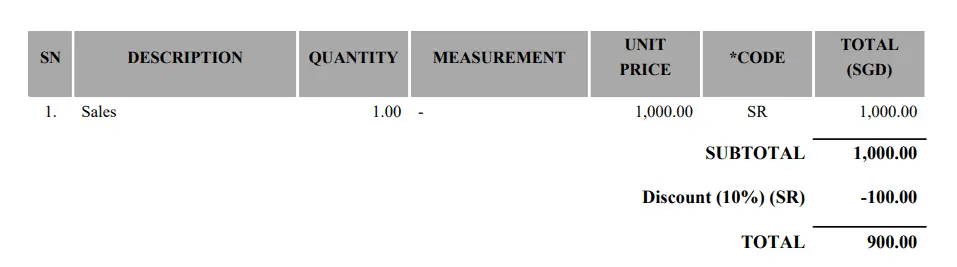

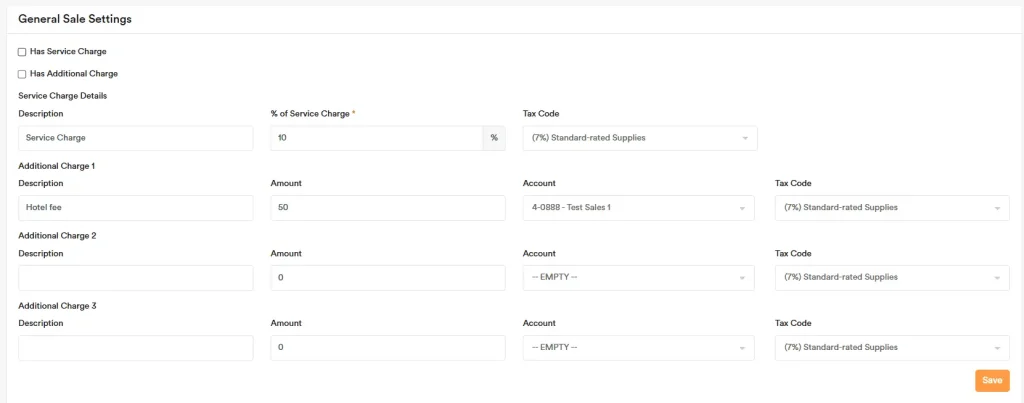

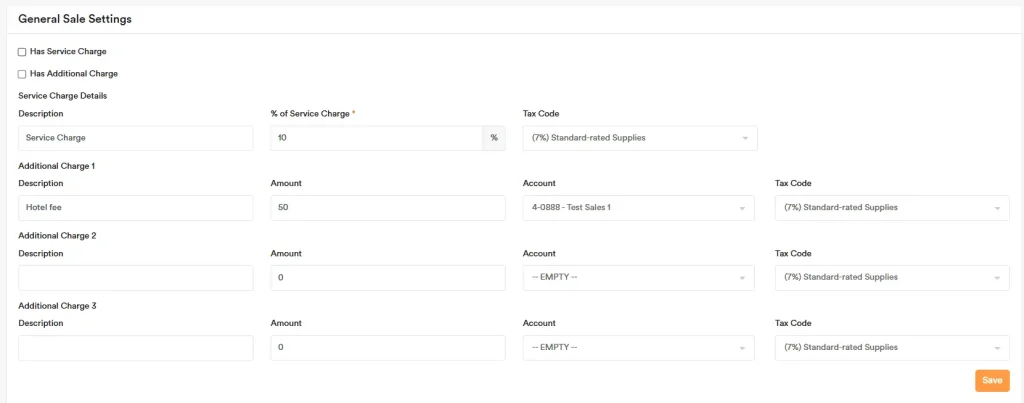

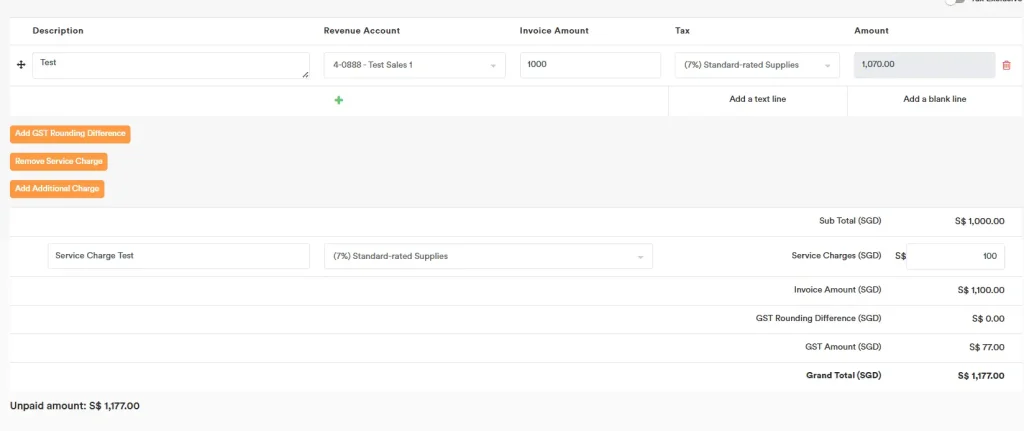

Discount Recording

You can record the sales discount by following these steps:

1. Add an account in the “Chart of Accounts” as shown below.

2. Select the Sales Discount option when issuing an invoice.

3. Input a negative amount for the Sales Discount.

For expense discounts, you can create a “Expense Discount” account with an “expense” Account Type for discount recording purposes.

There are a few options where you can record your sales discount.

First, record it as a separate line like below

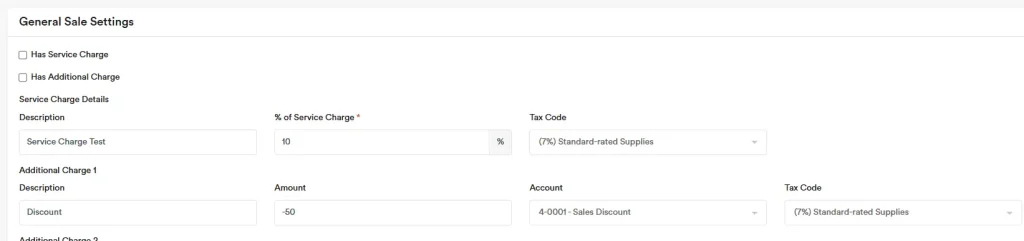

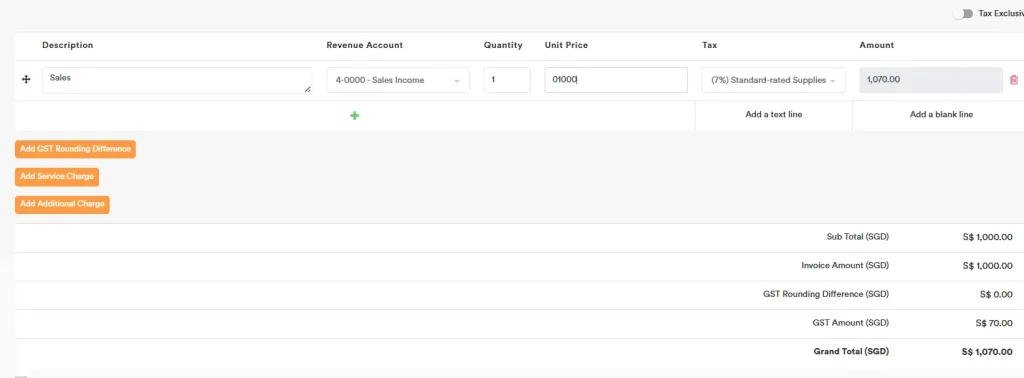

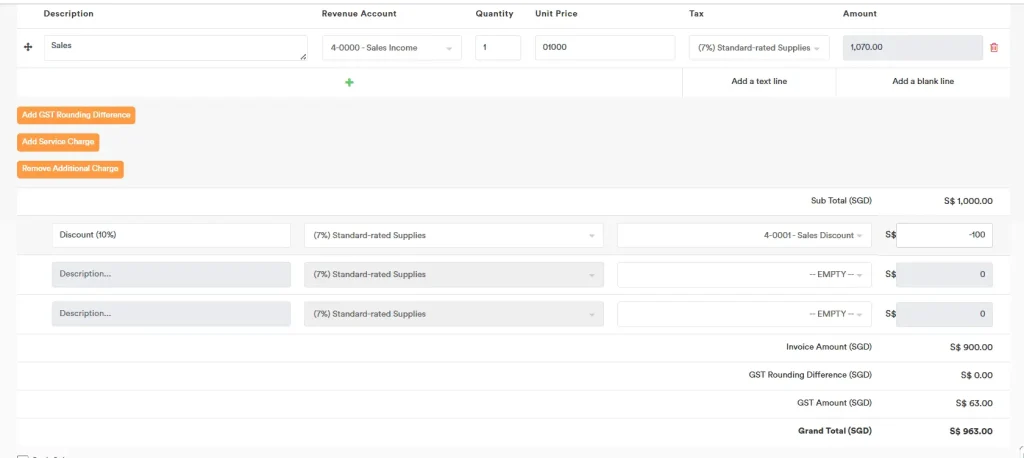

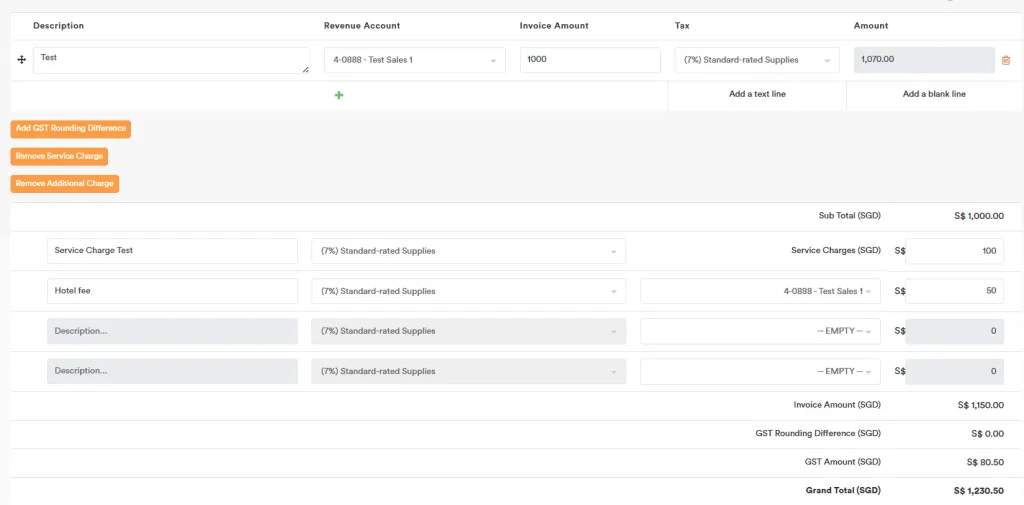

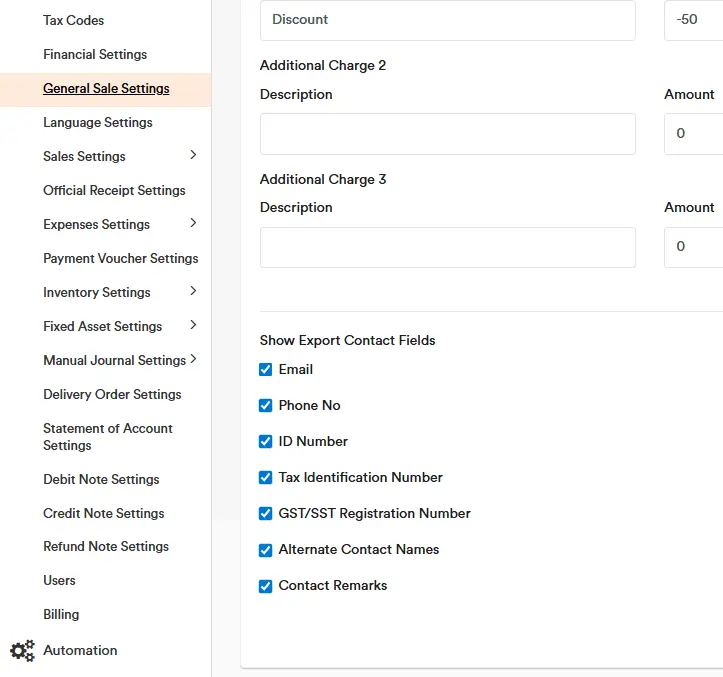

Second, you can record it as an Additional Charge so the discount shows after the subtotal. The steps are as follows:

1. Go to General Sale Settings,

2. Under Additional Charge 1, record it like below. For Description, enter “Discount” and a default amount (you can change this later when entering the sale, as each sale can have a different discount amount and %). For Account, select ‘Sales Discount’, and choose the tax code related to the discount.

3. When entering sales, click ‘Add Additional Charge’ to show the discount field.

4. Input the details: description with %, and the amount as a negative. Then click Submit.

5. Then you can generate the PDF tax invoice and see the discount listed like below.

Dividend Recording

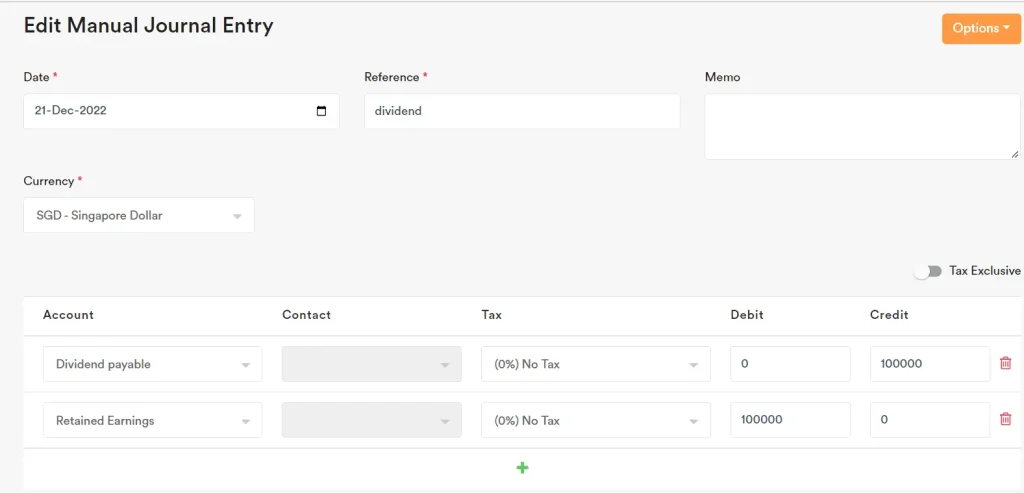

For record of dividend paid adjustment, you can use manual journal, example as follows.

When you click the Retained Earnings at Balance Sheet

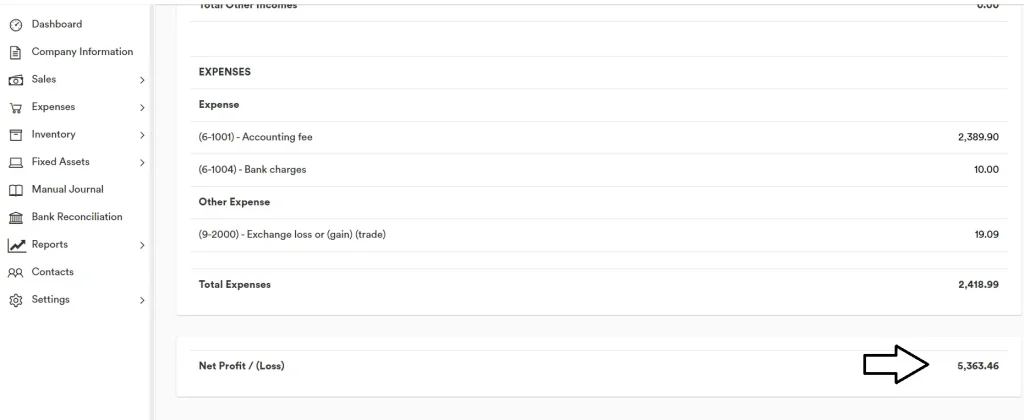

The system will bring you to the period of profit and loss which contribute to the retained earnings amount. For this situation, the Net Profit / (Loss) is not tally is due to the dividend adjustment of $100,000

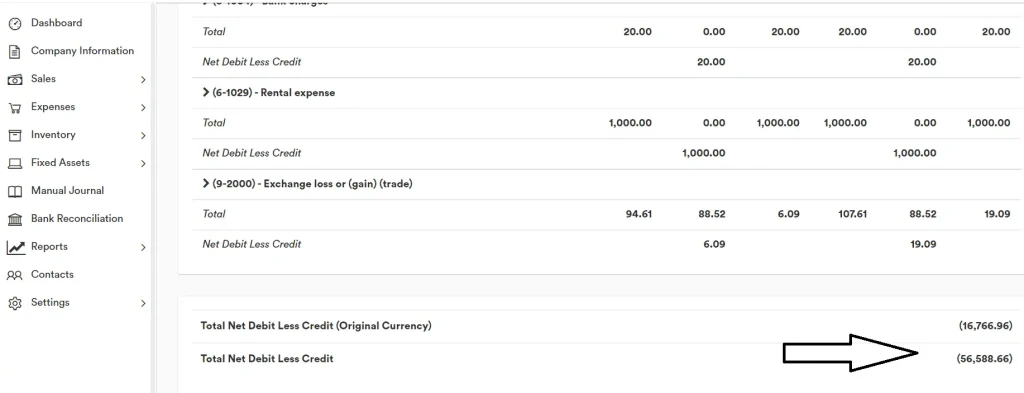

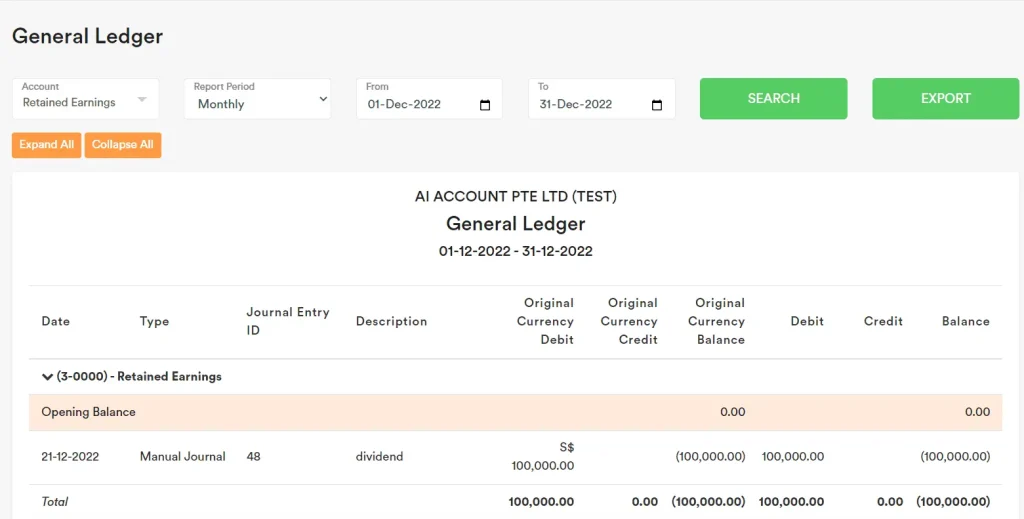

You can go to General Ledger to find the retained earnings adjustment to reconcile the different

Withholding Tax Recording

For sales payment and supplier payment, it is required to withhold tax in Indonesia usually. You can post the withholding tax entry when you make payment

1. Select “Add Receipt” on the unpaid invoice

2. For Sales, you can select “Sales Prepaid Tax” to record the Prepaid Tax to government (withholding tax by customer, remind to get supporting documents from your customer)

3. For Expenses, you can select “Expenses Withholding Tax” to record the Withholding tax that pay to government (withholding tax pay to government for the expenses vendor invoice, remind to send the supporting documents to your supplier)

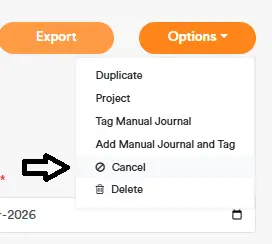

Cancel Records

You may choose to retain a record and cancel it instead of deleting it. This helps keep the numbering continuous and makes it clear that a particular invoice was cancelled. When you cancel a record, the transaction will not be posted as a double-entry.

After cancelling, you can convert the record back to Normal status if needed.

Only transactions with Saved or Unpaid status can be cancelled. Transactions that are partially paid or fully paid cannot be cancelled.

You can cancel records from the following sections:

- All Quotes

- All Sales

- All Purchase Orders

- All Expenses

- Inventory Sales Quote

- All Inventory Sales

- All Inventory Purchase Order

- All Inventory Purchases

- All Manual Journal Entries

- All Bank Entries

After you cancel, the record will show a Cancelled status (as shown below).

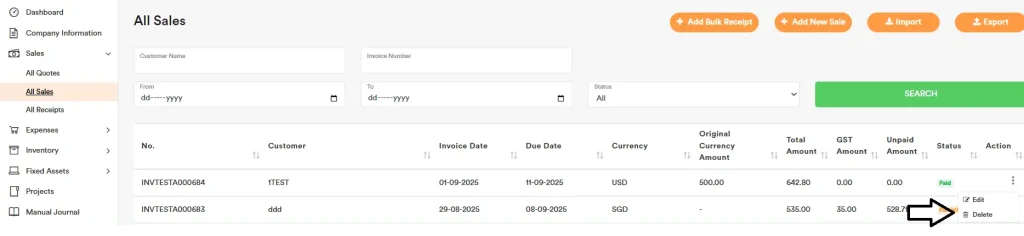

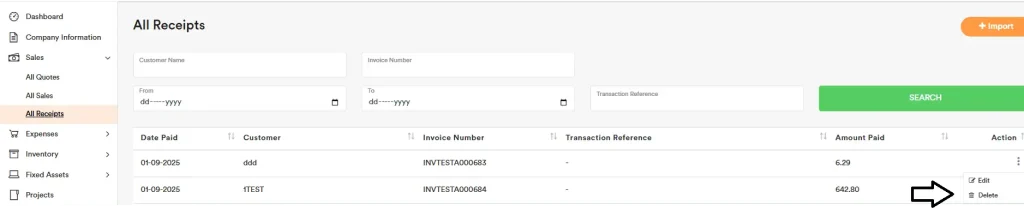

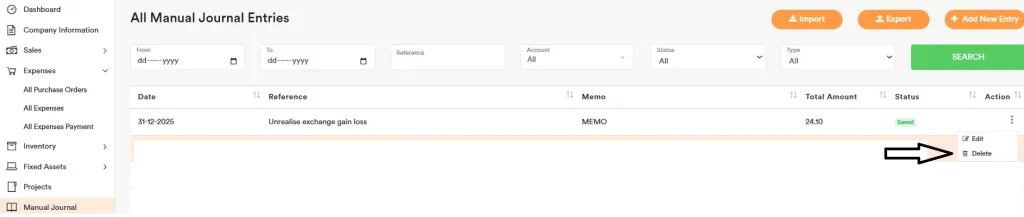

Delete Records

Sales Transactions

- Go to All Sales.

- In the Action column, click ‘Delete’.

- If a payment/receipt is linked to the transaction, it will be deleted together with the sales transaction.

Receipts

- Go to the All Receipts tab.

- In the Action column, click ‘Delete’.

- After the receipt is deleted, you can edit the related sales invoice.

Other Sections

Deletion works the same way in other modules. For example, in Manual Journal, use Action → Delete.

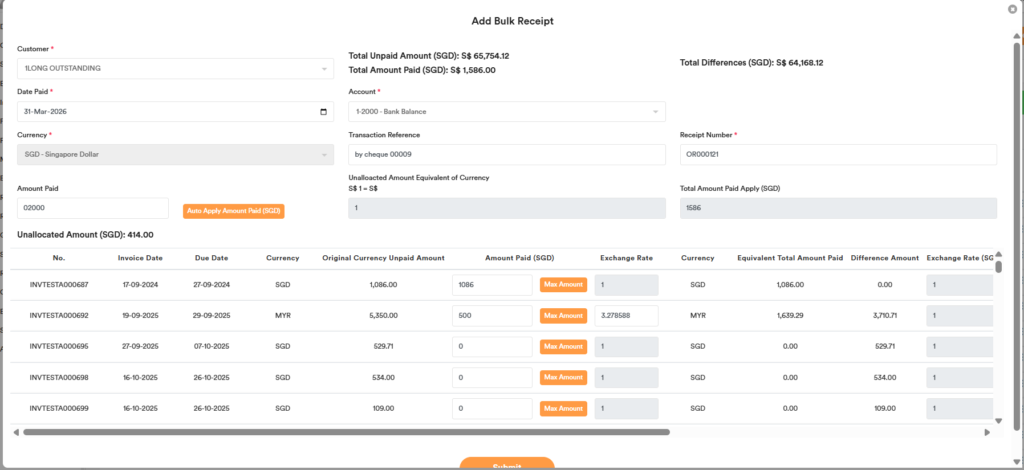

Payments for Multiple Invoices Recording

Your customer made a payment to you for multiple invoices. There are few ways to record this.

First method: You can record payments for multiple invoices at once using the “+ Add Bulk Receipt” or “+ Add Bulk Payment” button.

First, select the customer or supplier contact name. All outstanding invoices for that customer or supplier will then appear below. Next, enter the date, select the account where you received or made the payment, and enter a transaction reference to help track it during bank reconciliation.

Enter the total amount paid. You can choose to click the button ‘Auto Apply Amount Paid’ to automatically apply the payment amount to each invoice, or you can enter the amount for each invoice manually.

If there is an overpayment and the full amount not be applied to the invoices, the remaining balance will be recorded as a negative unallocated amount under receivables or payables.

The bulk receipt or payment function is available under the Sales, Expenses, Inventory Sales, and Inventory Purchases sections.

You can use bulk receipt or bulk payment for any currency you have.

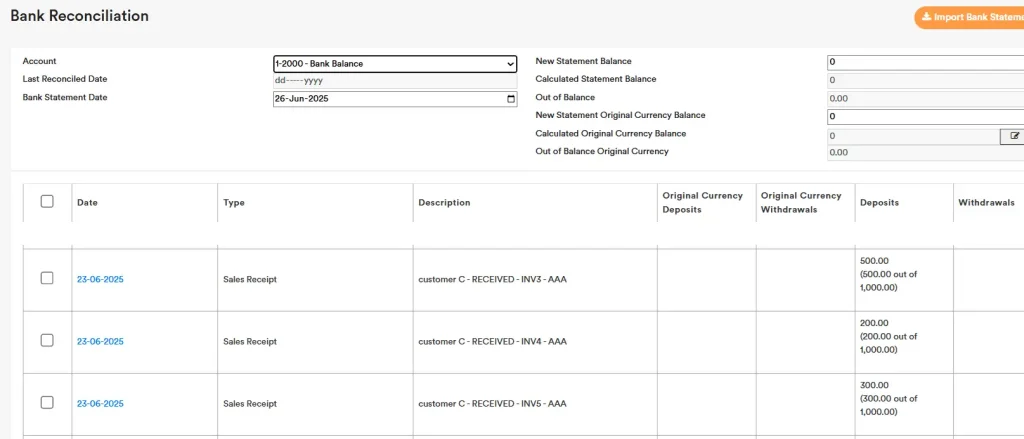

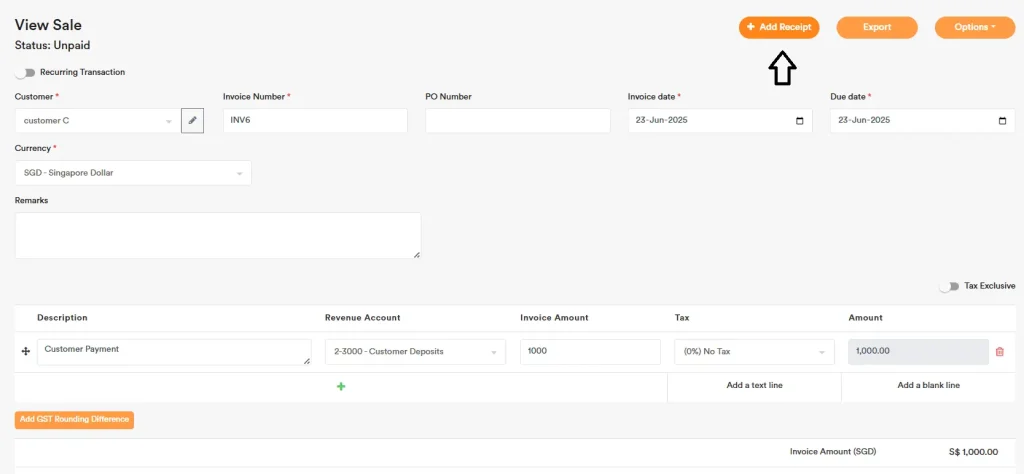

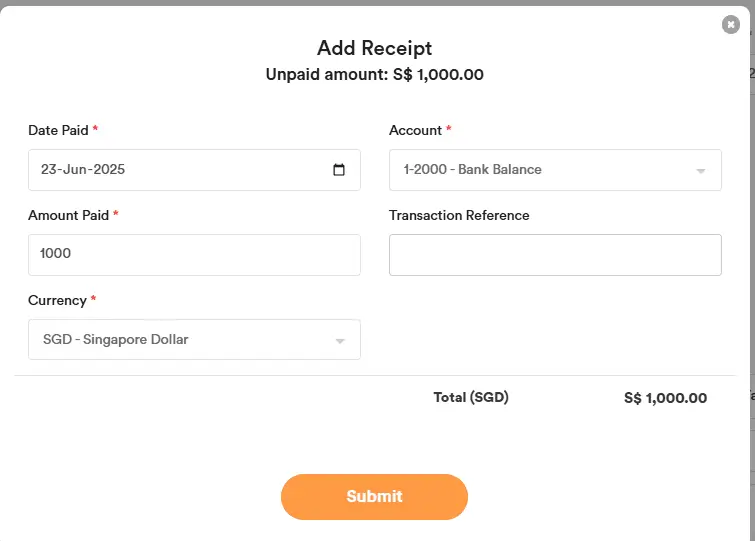

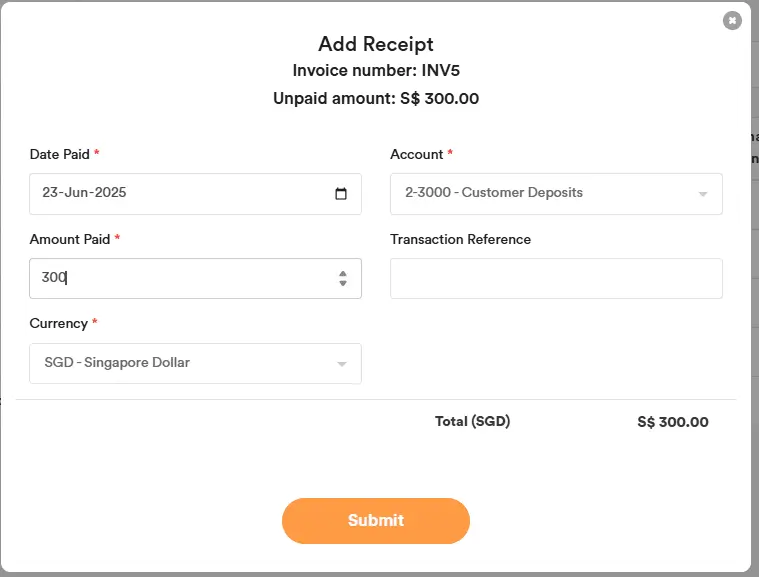

Alternatively, you can add the payment separately for each invoice. For example, if the client paid you $1,000 for the three invoices, you can click “Add Receipt” on each invoice individually. This will show as three separate payments in the bank reconciliation, with a total of $1,000.

In the bank reconciliation, you can see the combined total of receipts with the same date and reference.

Second method: You can record the full payment as a customer deposit and later apply it to the individual invoices. Here’s how:

- Create a new invoice and select the account “2-3000 Customer Deposits.”

- Enter a separate invoice number (for payment tracking purposes) and the amount received from the client (e.g., $1,000), then click “Submit.

- Then, click “+ Add Receipt” to record the payment received for this deposit invoice.

Enter the details and click Submit. The customer will now have a $1,000 deposit that can be used to offset the three invoices.

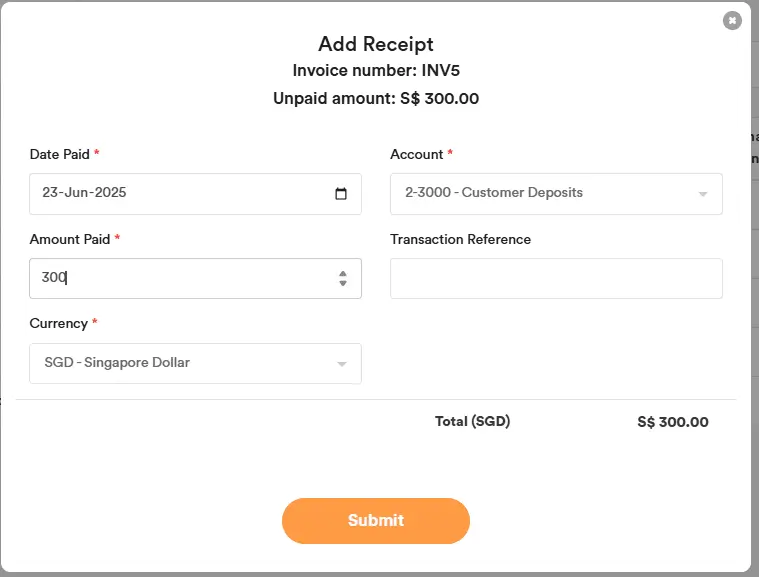

Next, go to each invoice, click “Add Receipt,” and select “2-3000 Customer Deposits” to apply the deposit towards the invoice and click Submit.

Once all invoices are settled, they will show as fully paid.

In the bank reconciliation, you will see only one payment entry. You can also check the aging report to confirm that the customer has no outstanding balance.

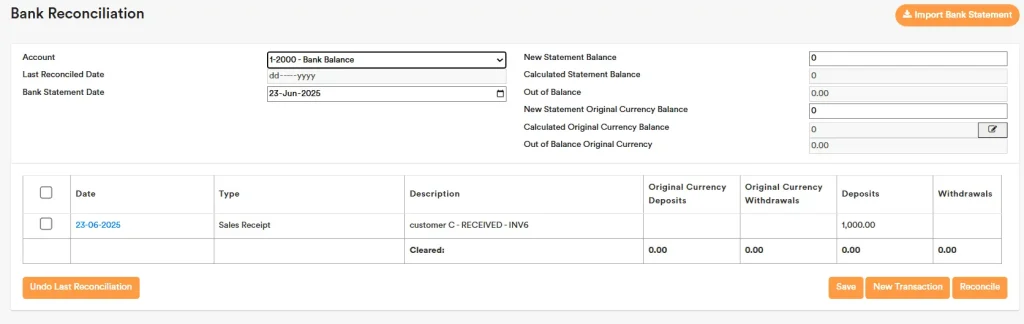

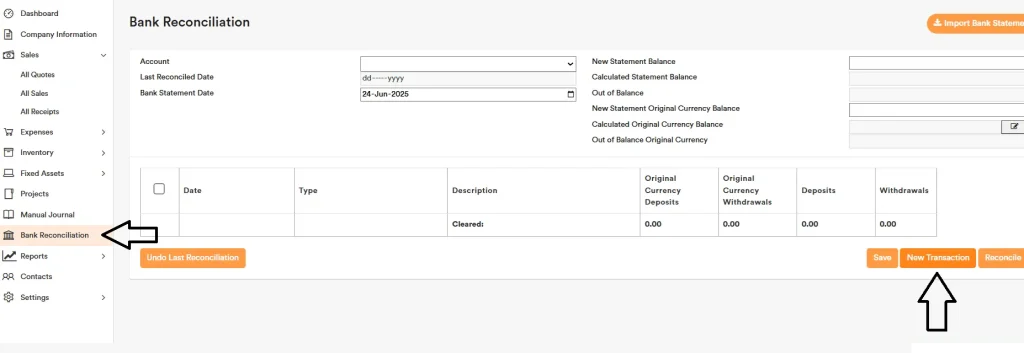

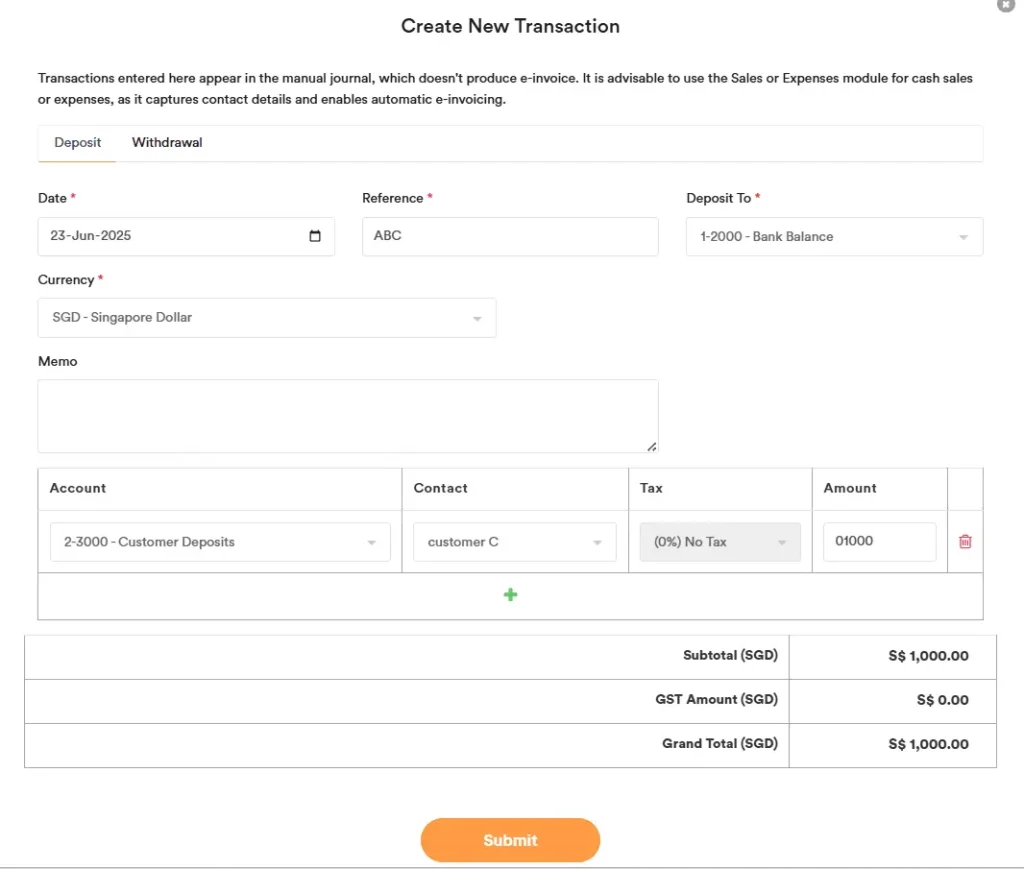

Third Method: You can record the full payment as a customer deposit via direct bank transaction and later apply it to the individual invoices. Here’s how:

- Go to “Bank Reconciliation” and click “New Transaction”.

- Select the bank account where the payment was received.

- For the Account, choose “2-3000 Customer Deposits”.

- Select the customer’s name under Contact.

- Enter the customer’s name and deposit details in the Reference field. (The reference will appear later in the bank reconciliation.)

- Click Submit.

The customer will now have a deposit of $1,000, which can be used to offset the outstanding invoices.

Next, go to each invoice, click “Add Receipt,” and select “2-3000 Customer Deposits” to apply the deposit towards the invoice and click Submit.

Once all invoices are settled, they will show as fully paid.

In the bank reconciliation, you will see only one payment entry. You can also check the aging report to confirm that the customer has no outstanding balance.

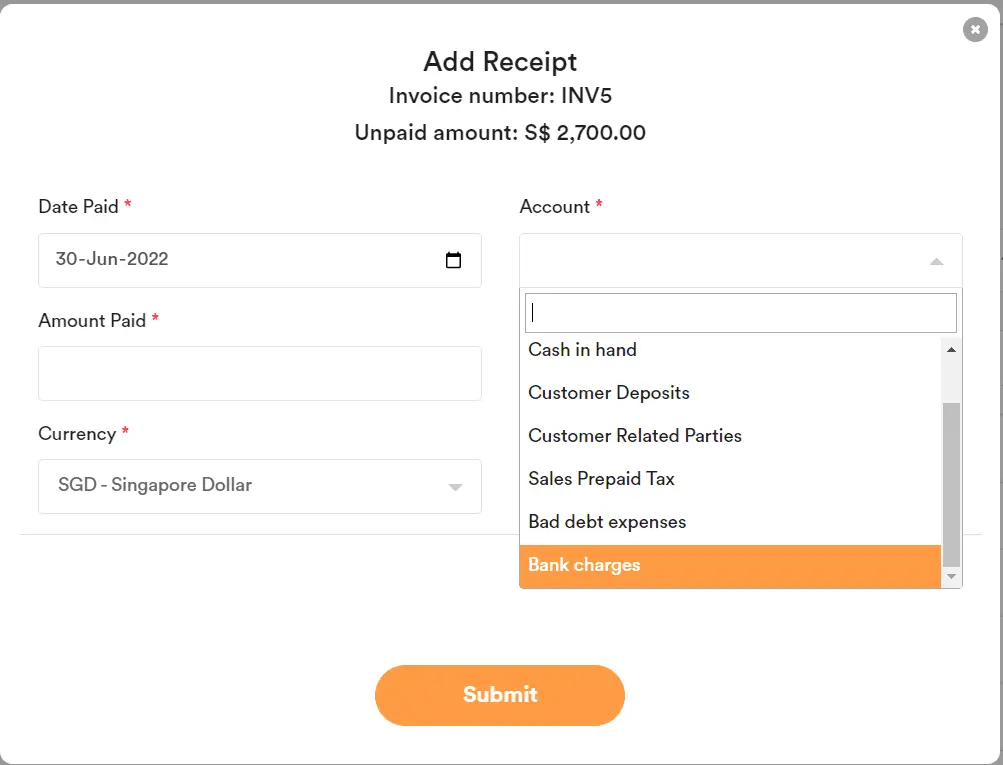

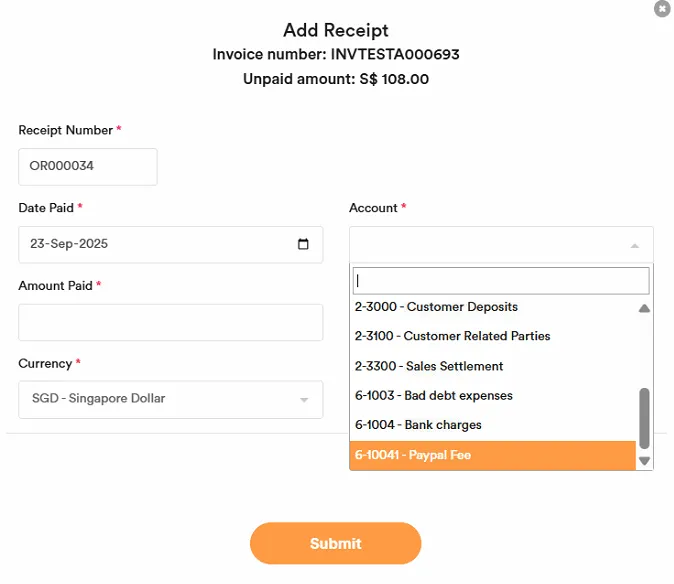

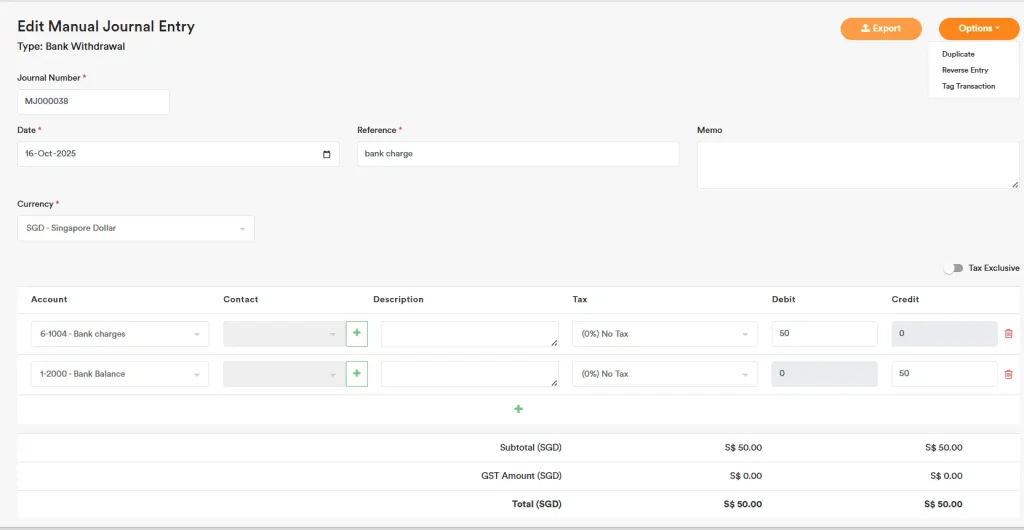

Bank charges imposed by bank when receipt of payments from customers

When a client makes payment for an outstanding invoice and there is a shortfall of balances due to bank charges imposed by the bank, you can select Account “Bank charges” during the Add Receipt recording.

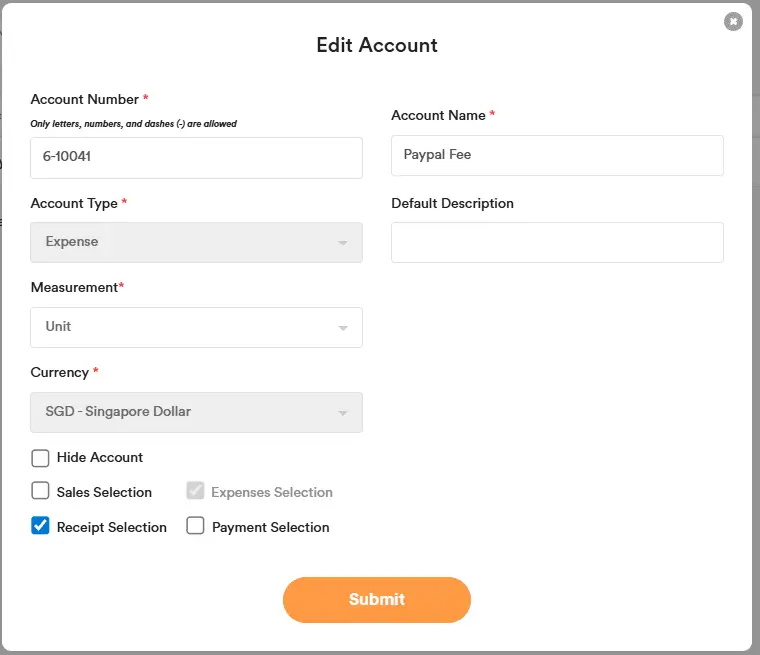

If a client pays you via PayPal and you want to record the PayPal fee, you can create a bank charge account by following these steps:

- Go to Accounts.

- Click Add New Account.

- Enter the details as follows:

- Account Number: Based on your preferences

- Account Name: PayPal Fee

- Account Type: Expense

- Tick “Receipt Selection”

- Click Submit.

You can then select the PayPal Fee account when entering a receipt for a customer, as shown below.

Other transactions (e.g. interest income)

For received interest income or incurred interest expenses etc, you can input the details via a manual journal entry.

Contra Sales and Expenses